Polaris (PII) Stock Looks 4.9% Overvalued as Rally Tests Fair Value

Polaris Inc. PII | 0.00 |

Recent trading in Polaris (PII) has put fresh attention on the stock, with investors weighing its recent share performance against fundamentals such as profitability, revenue mix, and the company’s current market valuation.

The recent 3.98% 1 day share price return, alongside a 36.26% 90 day share price return and an 86.01% 1 year total shareholder return, points to strengthening momentum in Polaris as investors reassess both risk and potential reward around the current valuation.

If Polaris’s move has you thinking about other opportunities tied to physical products and infrastructure, this could be a useful moment to scan 34 power grid technology and infrastructure stocks

With Polaris now trading above its analyst price target and carrying an intrinsic value estimate that sits well below the current share price, the key question is whether there is still a buying opportunity or whether the market is already pricing in future growth.

Most Popular Polaris Narrative: 4.9% Overvalued

The most followed valuation narrative for Polaris puts fair value at $68.00, slightly below the recent close at $71.36, which frames the stock as modestly ahead of that model.

In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 11.9x on those 2029 earnings, up from -9.0x today. This future PE is lower than the current PE for the US Leisure industry at 22.9x.

Want to see what is baked into that fair value for Polaris? The narrative leans on a steady revenue build, a clear margin reset, and a re rating in line with long term earnings power.

Result: Fair Value of $68.00 (OVERVALUED)

However, Polaris still carries key risks, including tariff costs that could squeeze margins and a weaker demand backdrop that may keep pressure on volumes and pricing.

Another View on Polaris Using Sales Based Valuation

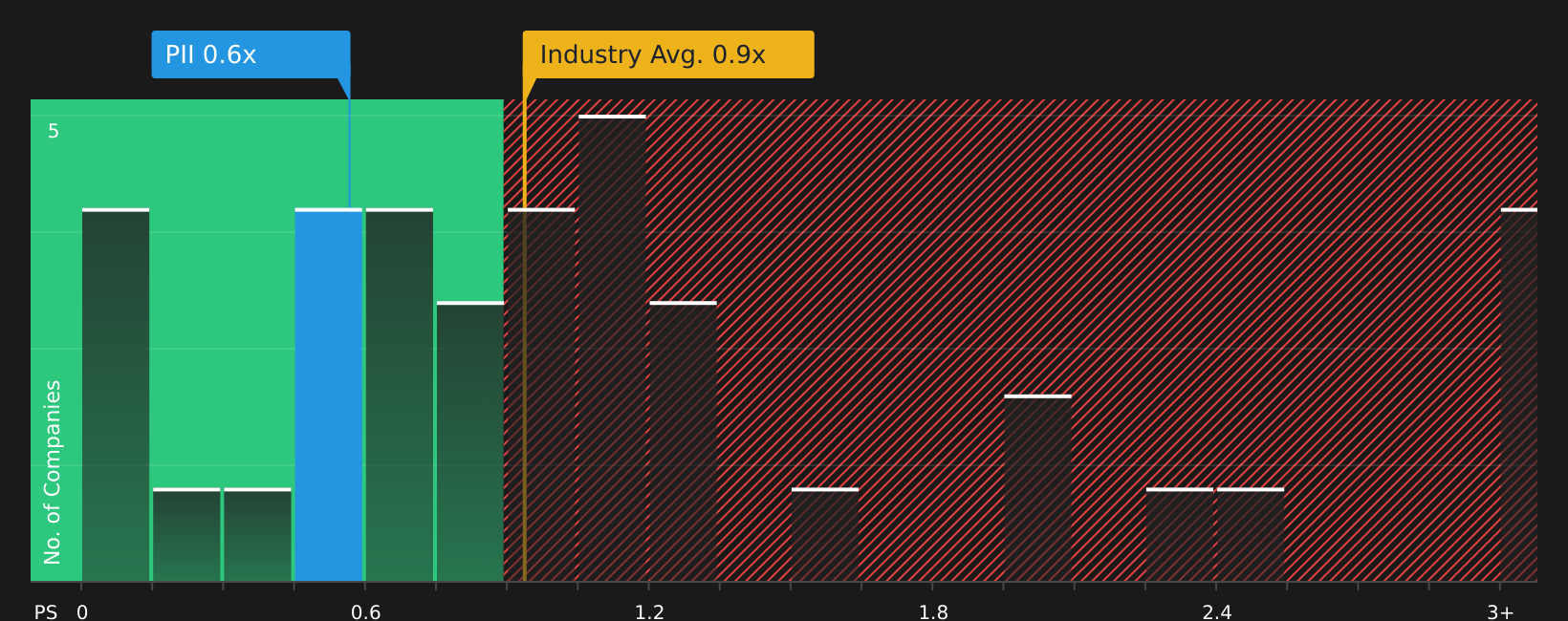

The popular narrative frames Polaris as about 4.9% above its $68.00 fair value, but the current P/S ratio paints a different picture. At about 0.6x sales versus a 1.0x industry average and a 1.2x peer average, Polaris trades at a clear discount to similar companies.

The fair ratio is also 0.6x, which is in line with where Polaris already trades, so the gap to peers looks more like a potential valuation risk or opportunity than a simple mispricing. The key question is whether that discount reflects genuine concerns around losses, tariffs, and interest coverage, or if the market is being overly cautious.

Next Steps

With mixed signals around Polaris’s upside and downside, it makes sense to move quickly, review the underlying data and form an independent view. To weigh those trade offs in more detail, start with the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Polaris?

If Polaris has sharpened your appetite for opportunities, do not stop here. Line up a few more ideas so you are not relying on a single stock.

- Target dependable cash generators by reviewing companies in the 45 high quality undervalued stocks that combine quality fundamentals with prices that sit below their estimated worth.

- Prioritize resilience by checking stocks in the 66 resilient stocks with low risk scores where risk scores aim to keep unexpected shocks from dominating your portfolio.

- Spot under followed opportunities early by scanning the screener containing 20 high quality undiscovered gems and seeing which solid businesses are not yet on most investors' radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.