Polestar Automotive Holding UK (PSNY) Valuation After Extended Loan Facility Support From Geely

Polestar Automotive Holding UK PLC Sponsored ADR Class A PSNY | 0.00 |

Polestar Automotive Holding UK (PSNY) has amended its term facility with affiliate Geely Sweden Automotive Investment AB, extending the loan maturity to June 30, 2027, and lifting the margin from 3.0% to 3.2%.

The extended facility comes as Polestar’s share price has been volatile, with a 7 day share price return down 18.11%, a 90 day share price return up 14.13%, and a 1 year total shareholder return down 38.24%. This suggests that momentum has recently faded following a short term rebound.

If this kind of funding update has you rethinking your watchlist, it could be a good moment to see which other electric and future mobility plays stand out via 21 top founder-led companies

With PSNY trading at US$18.90, compared with an average analyst price target of US$17.50 and carrying a low value score of 2, investors have to ask whether this weakness is a genuine opportunity or whether the market is already pricing in whatever growth lies ahead.

Most Popular Narrative: 8% Overvalued

At $18.90, the most followed narrative pegs Polestar’s fair value at $17.50, so the valuation sits slightly above that central estimate.

The analysts have a consensus price target of $17.5 for Polestar Automotive Holding UK based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $15.0.

Want to see what is built into that $17.50 figure? Revenue growth assumptions, margin repair and a future earnings multiple all pull in different directions.

Result: Fair Value of $17.50 (OVERVALUED)

However, there are clear risks to that overvaluation call, including going concern doubts and ongoing cash burn. This keeps Polestar reliant on fresh external funding.

Another Angle On Valuation

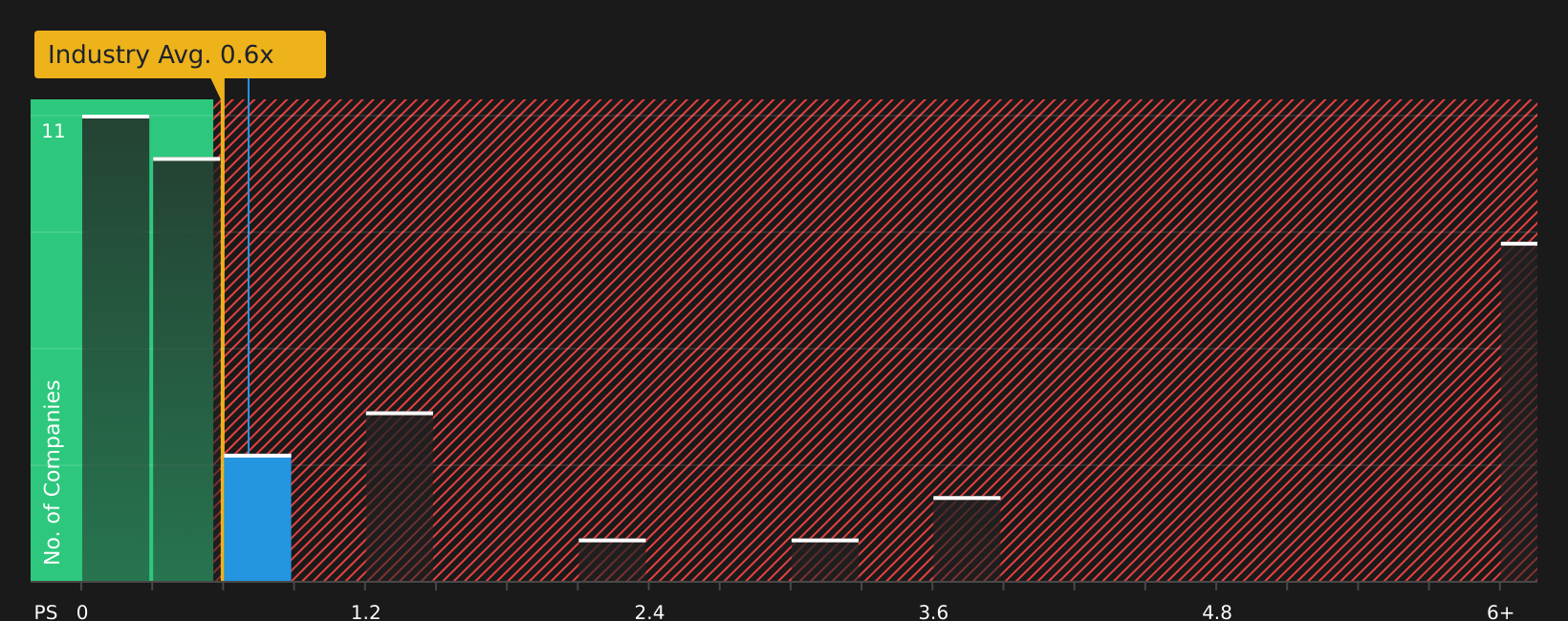

The earlier narrative leans on long term earnings assumptions and a target price of $17.50, yet today PSNY trades at a P/S ratio of 0.7x. That sits below a fair ratio estimate of 1.6x and below the 0.9x peer average, even though it is slightly above the 0.6x US Auto industry average. For investors, that mix of discount versus fair ratio and peers, but premium versus the sector, raises a simple question: is the market underestimating revenue potential or correctly marking the risks?

To see how this price signal lines up with the rest of the numbers, it is worth looking at a fuller breakdown of the valuation drivers, from growth and margins through to balance sheet pressure, in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of concern and optimism feels finely balanced, now is the time to review the numbers yourself and consider both perspectives. Start by checking the 1 key reward and 3 important warning signs

Looking for more investment ideas?

If Polestar has you reassessing your next move, do not stop here. Use focused screeners to spot other stocks that suit your goals and risk comfort.

- Target potential value opportunities by scanning 49 high quality undervalued stocks built on both quality and pricing signals.

- Prioritise resilience and capital preservation with 64 resilient stocks with low risk scores that keeps the focus on lower risk scores.

- Stay ahead of the crowd by checking the screener containing 22 high quality undiscovered gems that combines strong fundamentals with under followed stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.