Pool (POOL) Faces A Valuation Test Following Russell Growth Index Removals

Pool Corporation POOL | 0.00 |

Index removals put Pool stock in focus

Pool (POOL) has been dropped from several Russell growth indices, including the Russell 1000 Growth and Russell 3000 Growth, a change that can influence trading as index tracking funds rebalance holdings.

For you as an investor, this kind of index removal often affects short term supply and demand for the stock, separate from how the underlying pool supplies distribution business is performing or what its fundamentals look like.

Pool’s recent index removals come after a strong 30 day share price return of 22.2% and a 90 day share price return of 8.15%. However, the 1 year total shareholder return has declined 25.71% and the 5 year total shareholder return is down 49.88%, suggesting that recent momentum contrasts with a weaker longer term record.

If you are reassessing Pool in light of this index change, it can help to widen the lens beyond pools and outdoor products by reviewing 20 top founder-led companies.

So with Pool trading at US$219.47, sitting at a discount to analysts’ published price targets and some intrinsic value estimates, is the recent weakness setting up a mispriced opportunity, or is the market already factoring in all the future growth?

Most Popular Narrative: 14.2% Undervalued

Pool’s most followed narrative points to a fair value of about $255.91 per share, compared with the recent $219.47 close. This frames the current discount in the context of long term cash generation and capital returns.

Expansion of private label offerings (especially chemicals), alongside supply chain and digital platform investments (e.g., POOL360), are driving margin-enhancing product mix and operational efficiencies. This is supporting gross and net margin improvement over time. Increased adoption of e-commerce channels (POOL360 up to 17% of sales) and new location openings in dense pool markets are enabling customer retention, service differentiation, and efficient market penetration. This is strengthening competitive positioning and enhancing future earnings potential.

Curious what earnings profile, revenue runway, and profit margin mix could justify that higher fair value using a 7.2% discount rate and richer future P/E multiple assumptions? The full narrative spells out the growth, buyback, and profitability path that would need to line up for Pool to close that gap.

Result: Fair Value of $255.91 (UNDERVALUED)

However, Pool’s reliance on mature North American housing, along with its exposure to inflation in labor, transport, and materials, could challenge the earnings and multiple assumptions behind that fair value story.

Another View on Pool’s Valuation

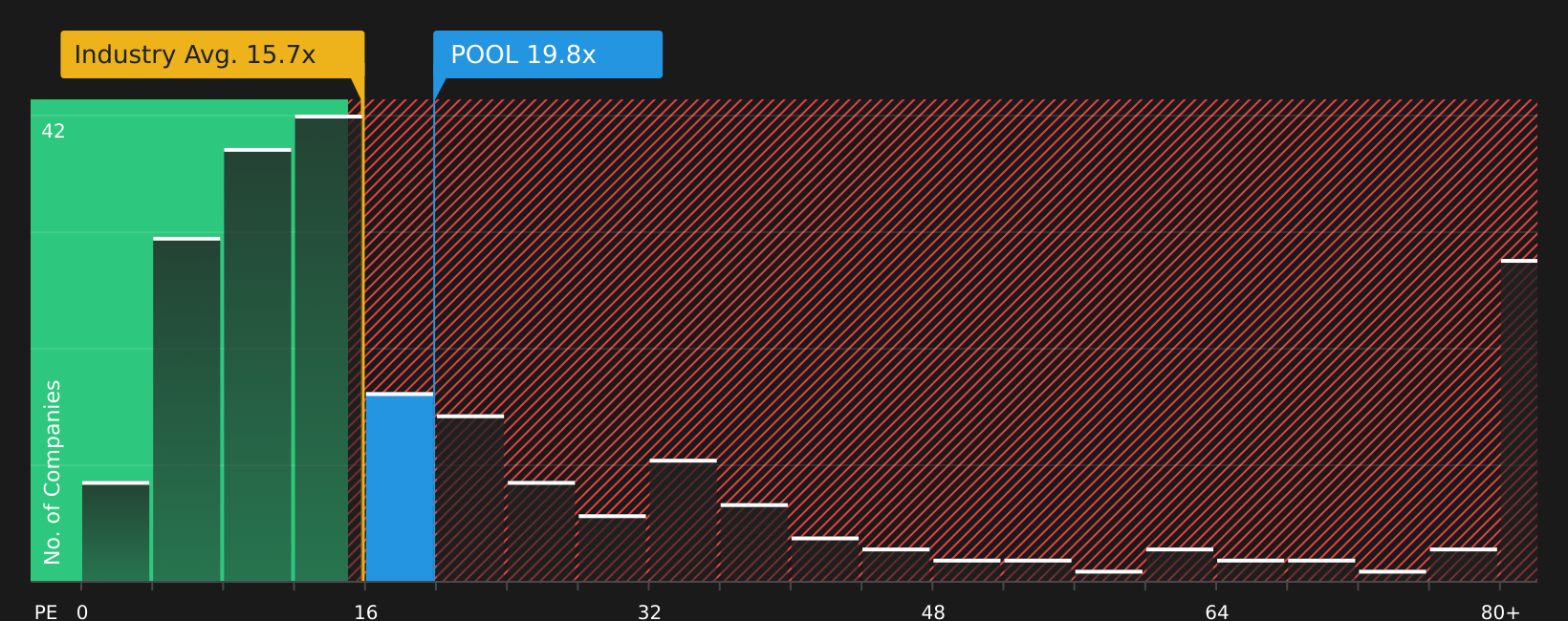

The earlier narrative framed Pool as trading below an estimated fair value of $255.91 per share based on future earnings and cash generation. Yet on a simple earnings multiple, the picture looks less comfortable, with the stock at a P/E of 19.8x versus a peer average of 13.2x and a fair ratio of 13.8x. This suggests investors today are paying a premium that could limit upside if expectations cool.

For a closer look at how that premium lines up with earnings quality, growth, and peer comparisons, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of concerns and optimism around Pool feels finely balanced, act while the information is fresh and weigh the trade offs yourself with 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Pool?

If Pool has sharpened your thinking, do not stop there. Fresh ideas across sectors can help you stress test your views and spot opportunities others overlook.

- Target income resilience by scanning companies with 7 dividend fortresses that may align with your yield and payout preferences.

- Hunt for quality at a discount using the screener containing 18 high quality undiscovered gems that filters for companies with solid fundamentals and less crowd attention.

- Dial up defense in your portfolio by focusing on 75 resilient stocks with low risk scores that screens for businesses with more stable risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.