Pool (POOL) Stock Could Be 33% Below Fair Value

Pool Corporation POOL | 0.00 |

Pool Corp has had a tough run, with the share price down about 50.9% over five years, yet its Discounted Cash Flow (DCF) estimate points to shares trading at a sizeable discount while traditional market multiples make the stock look expensive. That split between an intrinsic value signal suggesting upside and a multiples view pointing to a premium sets up a clear valuation debate for Pool today.

- The roughly 50.9% share price decline over five years means long term holders have seen substantial value erode, which naturally sharpens attention on whether the current price now builds in too much pessimism.

- For a distributor tied to pool and outdoor spending, expectations for steady cash generation can support the DCF view. At the same time, any sustained pressure on volumes or margins may challenge how much of that cash ultimately reaches shareholders.

- Pool screens as attractive on only 2 out of 6 valuation checks, which leans more towards the stock not being a straightforward bargain on the broader tests despite what the intrinsic value estimate suggests.

The stock's next move may depend on whether Pool's cash flow delivery ends up justifying the DCF implied upside or whether the richer market multiples prove to be a better guide to where the valuation should sit.

Is Pool Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) method values Pool by projecting its future cash generation and discounting it back to today. Pool has reported latest twelve month free cash flow of about $308.1 million, and the model assumes cash flows grow from this base rather than shrink, consistent with the 2 Stage Free Cash Flow to Equity setup.

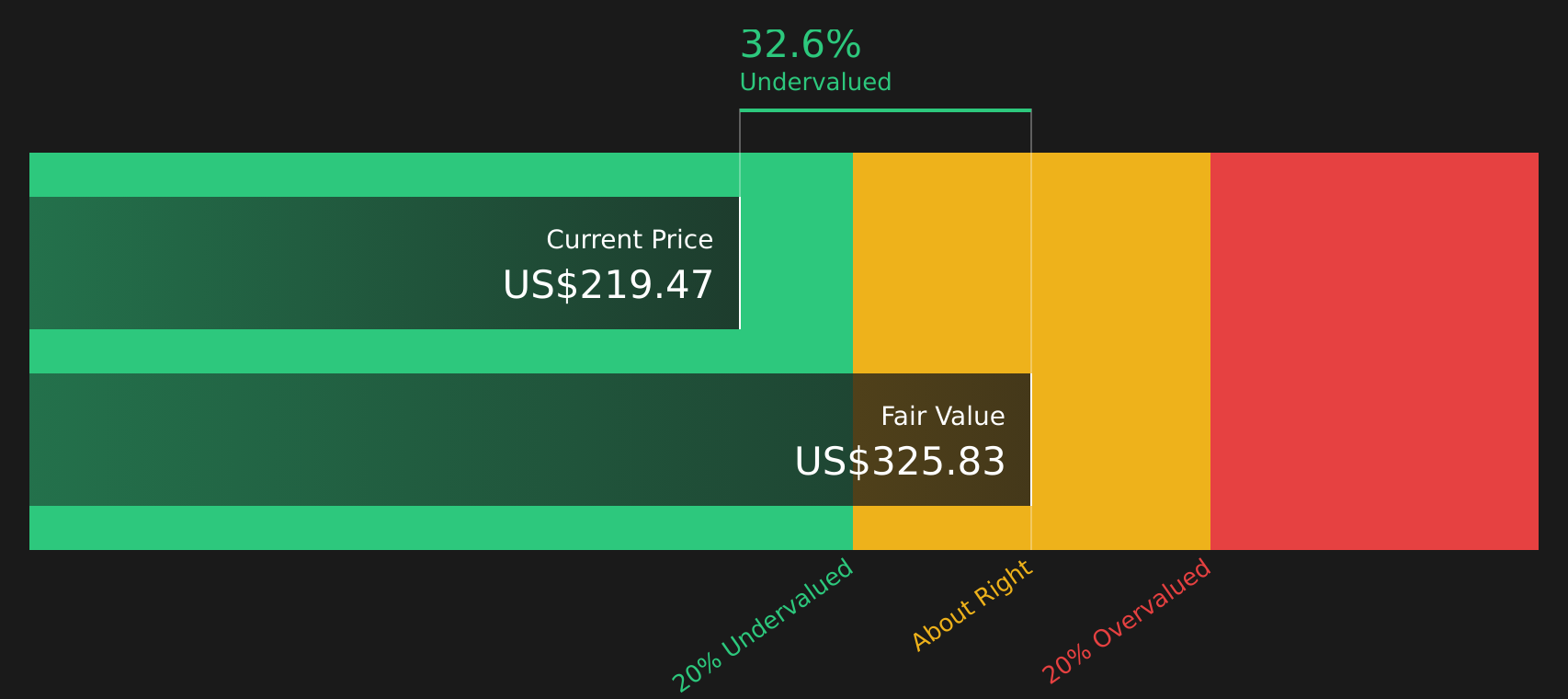

On these assumptions, the DCF model points to an intrinsic value around $322 per share, which compares to a current price that sits roughly 33.1% below that estimate. For readers, that gap suggests the market price does not fully reflect the cash flows implied in the model, even after a difficult share price stretch for Pool stock.

Taking the Discounted Cash Flow output at face value, Pool stock appears undervalued relative to its modeled cash generation.

Our Discounted Cash Flow (DCF) analysis suggests Pool is undervalued by 33.1%. Track this in your watchlist or portfolio, or discover 41 more high quality undervalued stocks.

Is Pool Getting Expensive on Earnings?

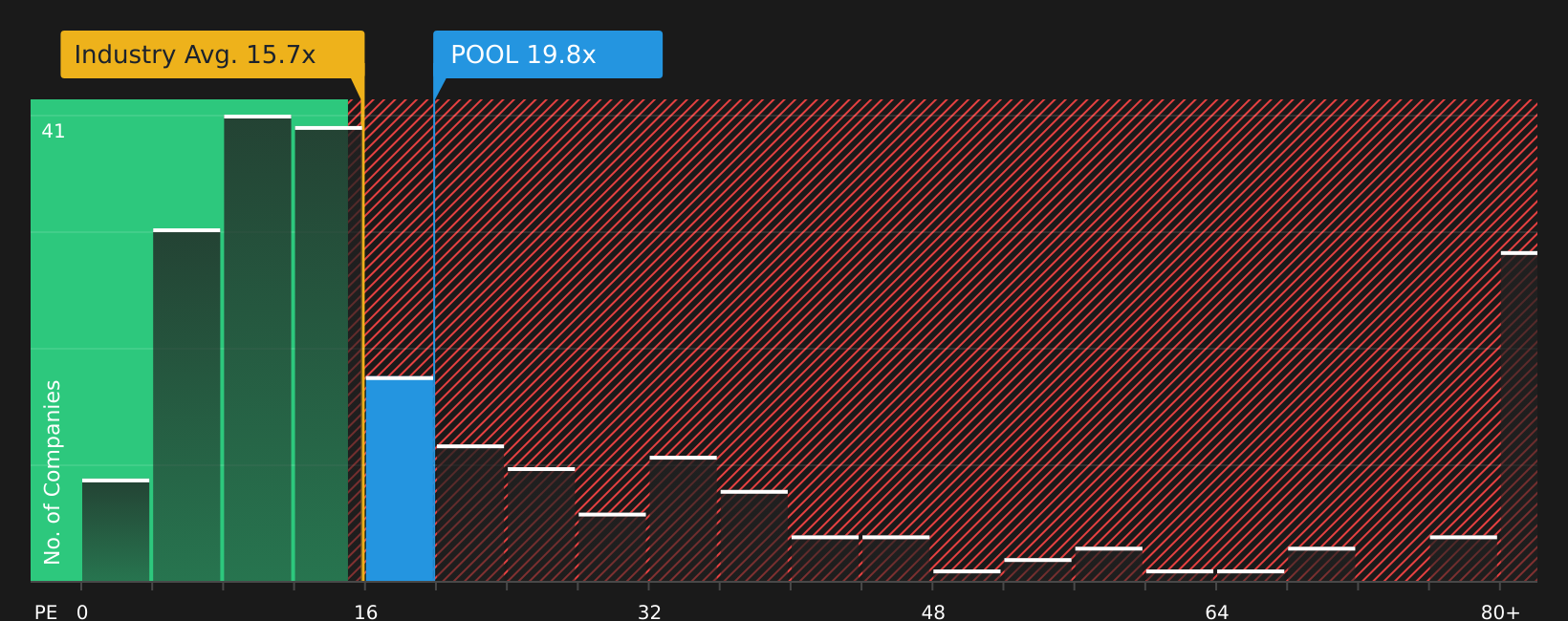

For a mature business like Pool, the P/E ratio is a straightforward way to see what you are paying for each dollar of earnings. Pool currently trades on a P/E of about 19.5x, compared with an industry average for Retail Distributors of roughly 15.7x and a peer average near 13.1x, so the stock carries a clear earnings premium.

The fair P/E ratio estimated for Pool is about 13.8x, which is well below the current multiple. That gap indicates investors are paying more for Pool's earnings than the model suggests would be typical once factors such as its industry, scale and risk profile are taken into account. For readers comparing the DCF signal to this earnings view, the P/E suggests the market is still assigning a higher price to Pool than the tailored benchmark would imply.

On the P/E yardstick, Pool stock currently screens as overvalued relative to the earnings multiple that the model flags as fair.

The Pool Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Pool's valuation split leaves off by spelling out which assumptions about Pool's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than it is today on the market. Each narrative links a fair value to a particular combination of potential catalysts and risks, so you can track over time which version of Pool's story is actually unfolding on Simply Wall St's Community page.

One of the top community narratives on Pool: 16% undervalued

"Expansion of private label offerings, alongside supply chain and digital platform investments, are driving margin enhancing product mix and operational efficiencies..."

Do you think there's more to the story for Pool? Head over to our Community to see what others are saying!

The Bottom Line

For Pool Corp, the Discounted Cash Flow (DCF) intrinsic value estimate points to meaningful upside at current levels, while the P/E comparison flags the stock as overvalued relative to peers and a tailored fair multiple. That split reflects how cash flow based models lean on the timing and durability of free cash generation. In contrast, market multiples lean on how much growth and sentiment investors are currently willing to pay for. Broader valuation checks are weak, so the DCF signal sits against a cautious backdrop. The key question from here is whether Pool's cash flows and margins hold up well enough to justify both the intrinsic value estimate and the premium earnings multiple.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.