Powell Industries (POWL) Joins Key Russell Indexes, Is The Upside Already Priced In?

Powell Industries, Inc. POWL | 0.00 |

Powell Industries (POWL) has just shifted into a different index tier, moving from several Russell 2000 indices into the Russell 1000 and related growth and defensive benchmarks. This change can influence how certain funds treat the stock.

Over the past year, Powell Industries has combined a strong 1 year total shareholder return of 240.44% with a 109.63% year to date share price return. However, recent trading has cooled, with the share price down 13.53% over 30 days and 11.95% over 7 days after the index moves and upbeat backlog commentary.

If you are looking beyond Powell Industries for other power grid and infrastructure plays, now could be a good time to scan the market with the 35 power grid technology and infrastructure stocks.

After such a sharp multi year run and a recent pullback, Powell Industries now sits in larger cap growth and defensive indices with analyst targets above the last close. Is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 31.6% Undervalued

Based on the most widely followed narrative, Powell Industries' fair value of $360 sits above the last close of $246.33, framing a bullish long term setup that hinges on several growth and margin assumptions.

The multi year build out of U.S. LNG export facilities and related natural gas infrastructure is contributing to a pipeline of large, complex projects, supporting backlog stability, higher plant utilization and stronger gross margins.

Strategic capacity expansions in Houston and ongoing productivity investments are increasing throughput and manufacturing leverage. This may enable Powell to convert its record backlog more efficiently and support higher operating margins over time.

Curious what earnings power this backlog could support? The narrative leans on faster top line growth, higher profitability, and a premium future earnings multiple. The full picture connects these moving parts into one valuation story.

Result: Fair Value of $360 (UNDERVALUED)

However, this Powell Industries bullish setup still depends on the timing of LNG projects as well as continued grid and data center spending, both of which could disappoint and pressure margins.

Another View on Powell Industries Valuation

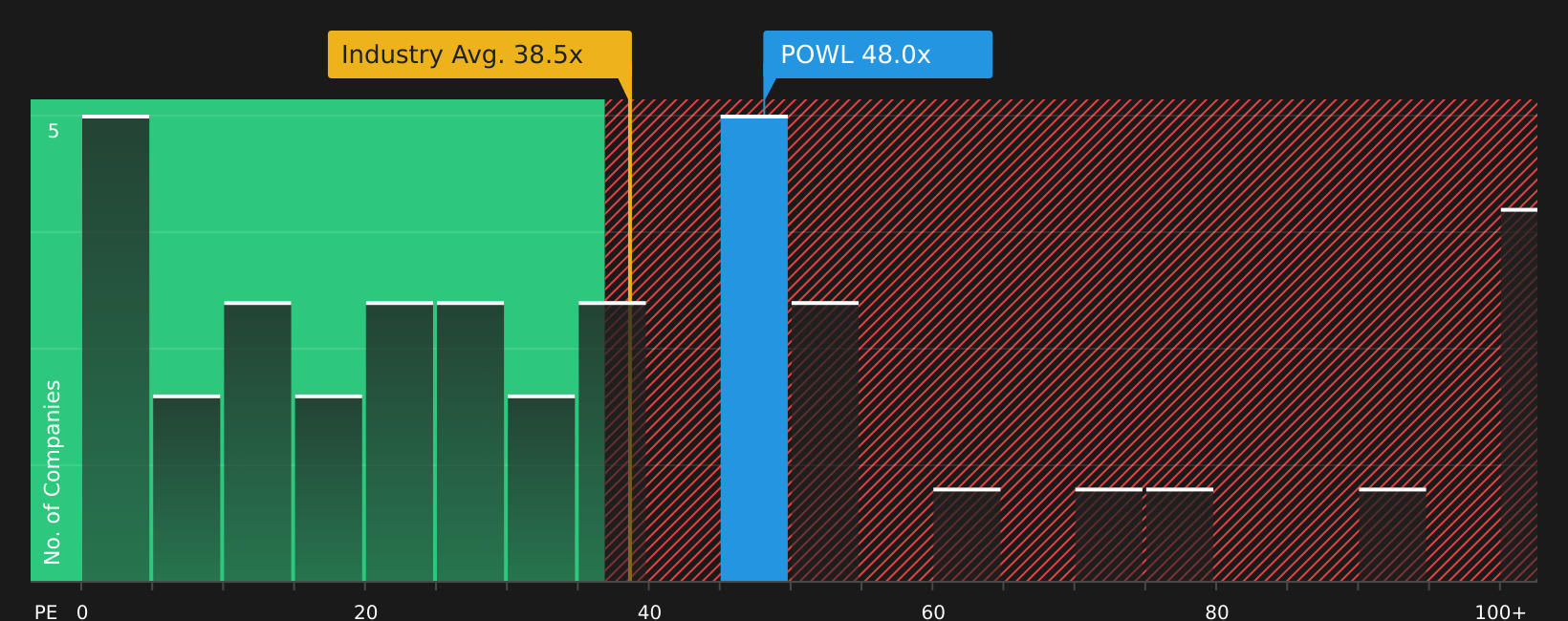

The popular Powell Industries narrative leans on a higher future P/E to argue for upside, but the current P/E of 48x already sits well above the fair ratio of 36.9x, the US Electrical industry at 38.5x and peers at 42.9x. That richer multiple can point to valuation risk if expectations ease.

To see what the numbers say about this price, find out in our valuation breakdown, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

The mix of optimism and caution around Powell Industries is clear. Take a moment to review the data, weigh both sides, and shape your own stance with the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Powell Industries?

If Powell Industries has your attention, do not stop here. Put a few minutes into finding other stocks that fit your style using the Simply Wall Street Screener.

- Target potential bargains backed by solid fundamentals with the 44 high quality undervalued stocks before other investors focus on them.

- Prioritise resilience and sleep better at night by scanning the 74 resilient stocks with low risk scores that keeps downside firmly in view.

- Spot companies with strong finances that can fund growth or dividends using the solid balance sheet and fundamentals stocks screener (47 results) while opportunities are still on the table.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.