Power Integrations (POWI) Stock Still Looks Expensive On Fresh Analyst Target Hikes

Power Integrations, Inc. POWI | 0.00 |

Power Integrations stock has surged 78.2% year to date, yet based on current checks it still screens as expensive rather than a clear bargain. That creates a tension for investors between strong recent momentum and valuation metrics that point to a premium.

- The 78.2% gain year to date indicates that expectations for Power Integrations have reset sharply higher and may leave less room for disappointment.

- Recent analyst interest in Power Integrations' high power GaN portfolio and product pipeline can support elevated expectations, but any slowdown in capturing those high growth opportunities may weigh heavily on what investors are willing to pay.

- Power Integrations passes 0 of 6 valuation checks on Simply Wall St, which means the broader assessment leans expensive rather than suggesting a clear value opportunity, according to the valuation summary.

The stock's next move may depend on whether Power Integrations' future execution is viewed as sufficient to justify this kind of premium after such a strong run year to date.

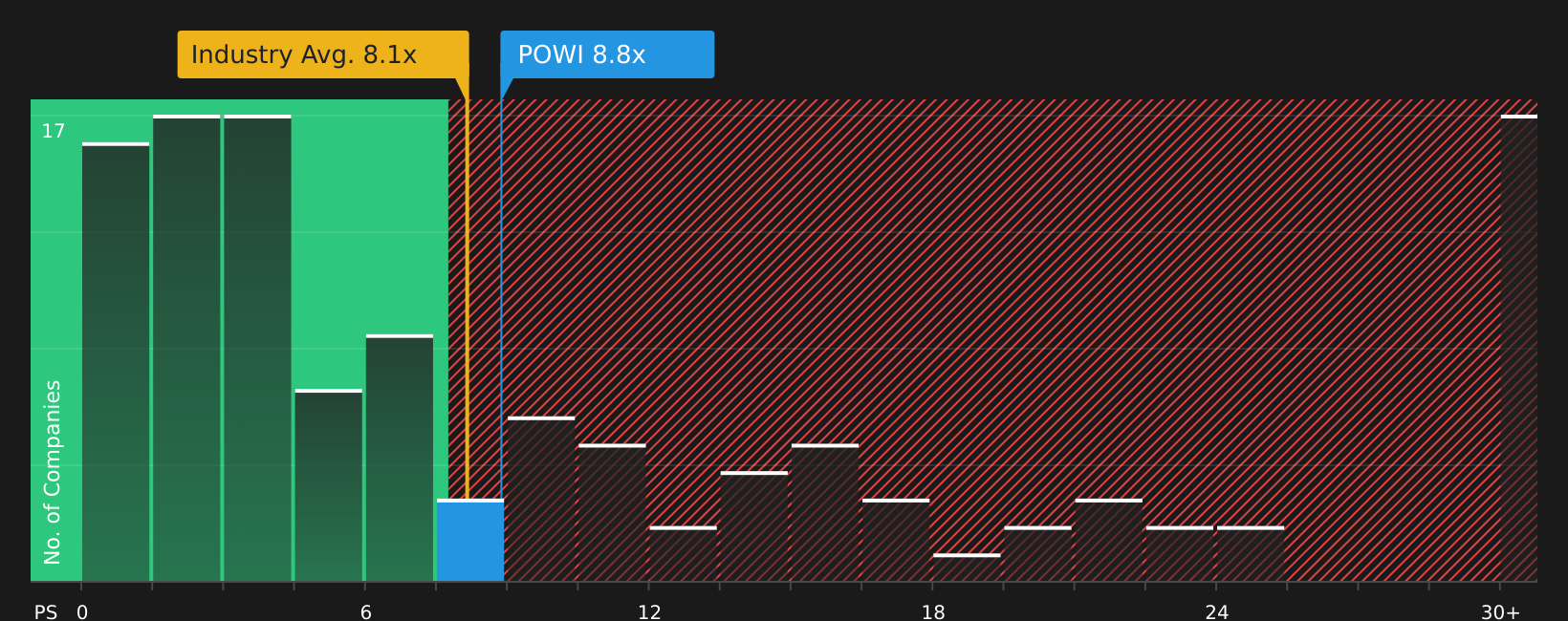

Has Power Integrations Run Too Far on Sales?

P/S is a useful lens for Power Integrations because revenue is a central reference point for many semiconductor investors. Power Integrations currently trades at a P/S ratio of 8.3x, compared with a semiconductor industry average of 7.5x and a peer average of 6.2x. The stock therefore already sits on a visible premium to both the broader sector and closer comparables.

The tailored fair P/S ratio for Power Integrations is 6.5x, which reflects what investors might typically pay given the company’s profile and risk factors. Against this benchmark, the current 8.3x suggests the stock is pricing in more optimistic assumptions than the model would indicate. Recent analyst upgrades highlight Power Integrations' growth potential and product portfolio, but the gap to the fair P/S ratio indicates the market is already assigning a relatively rich revenue multiple.

Overall, Power Integrations appears fully valued to overvalued on the P/S multiple, with the current price implying a premium to both sector norms and the modelled fair ratio.

The Power Integrations Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Power Integrations aim to spell out which combinations of revenue growth, margins and earnings would need to hold for Power Integrations' current valuation premium to look too high or too low. They use those assumptions to bridge the gap between today’s P/S ratio and potential future outcomes on the Community page. Each narrative treats fair value as a thesis about how the business might progress that you can revisit over time rather than a one off snapshot.

The community is split on Power Integrations, with one camp seeing room for upside and another arguing the stock already bakes in too much optimism.

Bull case: 30% undervalued

"Structural global trends in electrification and rapidly tightening energy efficiency standards create a powerful multi-year demand tailwind for Power Integrations' proprietary high-voltage, high-efficiency platforms..."

Bear case: 48% overvalued

"Some research points to a risk that the current P/E multiple may already reflect optimistic expectations, leaving less room for execution missteps or slower than expected growth in core markets..."

Do you think there's more to the story for Power Integrations? Head over to our Community to see what others are saying!

The Bottom Line

For now, Power Integrations looks overvalued on the market-multiple view, with the stock trading at a clear premium to both sector norms and its tailored fair P/S ratio. That does not rule out further gains, but it does mean the margin for error is thinner if expectations around high power GaN adoption or broader revenue momentum soften. The crux for investors is whether Power Integrations can deliver enough consistent growth and execution to keep justifying this premium, or whether sentiment cools and the P/S multiple settles closer to peers over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.