Procter & Gamble (PG) Stock After Mixed Recent Returns Is The Current Valuation Attractive

Procter & Gamble Company PG | 0.00 |

- If you are wondering whether Procter & Gamble stock is offering fair value or a potential discount right now, the starting point is understanding how its current price lines up against several valuation checks.

- The share price recently closed at US$148.50, with returns that include a decline of 1.3% over the past week but gains of 3.9% over the past month and 4.7% year to date, alongside a decline of 3.7% over the last year.

- Recent coverage has focused on how Procter & Gamble fits into evergreen portfolios as a large household products company that many investors monitor regularly. This has kept attention on whether its current price properly reflects its long history as a core holding in many long term portfolios, especially when returns have been mixed across different time frames.

- On Simply Wall St's valuation checks, Procter & Gamble currently records a valuation score of 4 out of 6. This means it screens as undervalued on four checks and not on two. That sets up a closer look at traditional valuation methods and hints at a broader way to think about value that will be covered at the end of this article.

Approach 1: Procter & Gamble Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows, then discounts them back to today using a required return, to estimate what a stock like Procter & Gamble might be worth right now in $.

For Procter & Gamble, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is reported at about $15.6b. Analysts provide free cash flow estimates for the next few years, and Simply Wall St then extrapolates those figures further. In this case, projected free cash flow for 2028 is $16.8b, with additional estimates extending out to 2035 based on those earlier inputs.

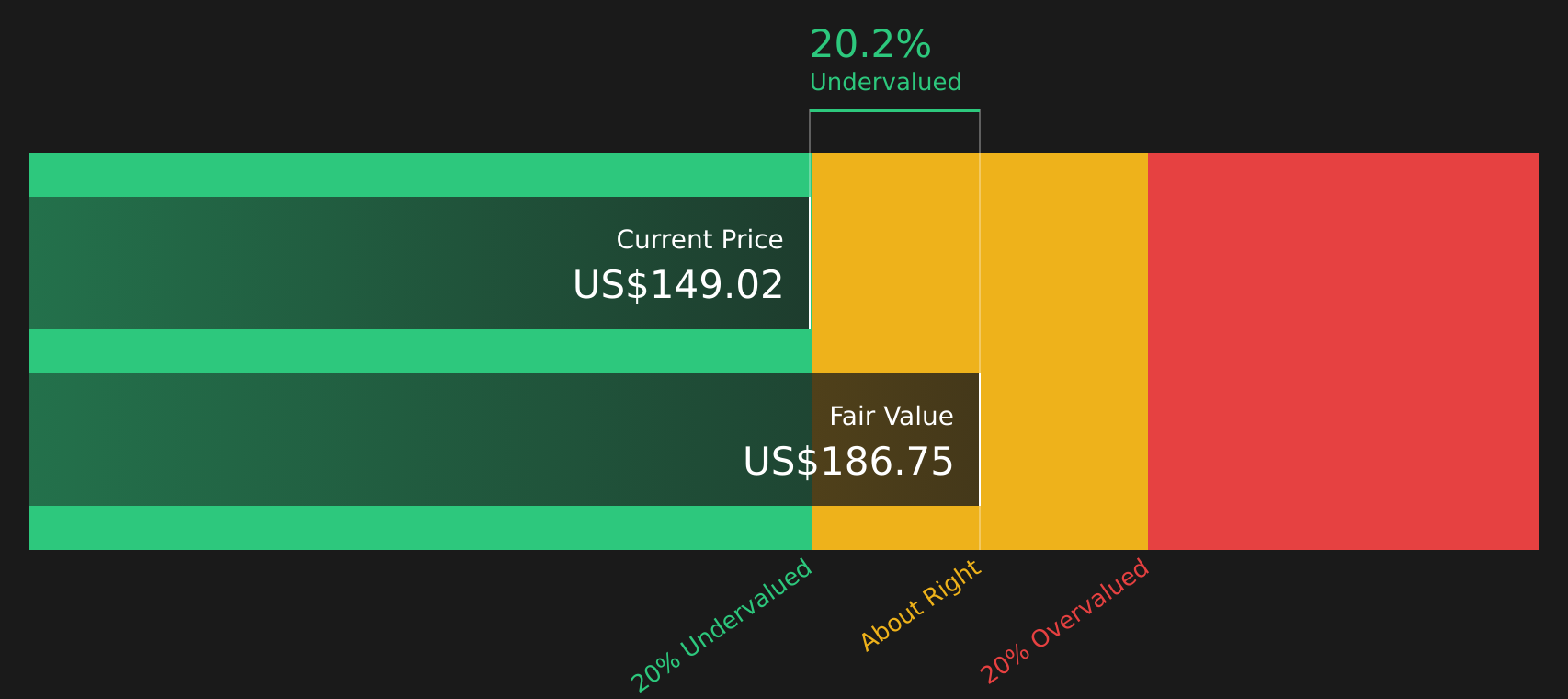

Pulling all of these cash flows together and discounting them produces an estimated intrinsic value of $186.75 per share. Compared with the recent share price of $148.50, the model points to an implied discount of about 20.5%, which indicates that Procter & Gamble stock currently screens as undervalued on this DCF measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Procter & Gamble is undervalued by 20.5%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Approach 2: Procter & Gamble Price vs Earnings

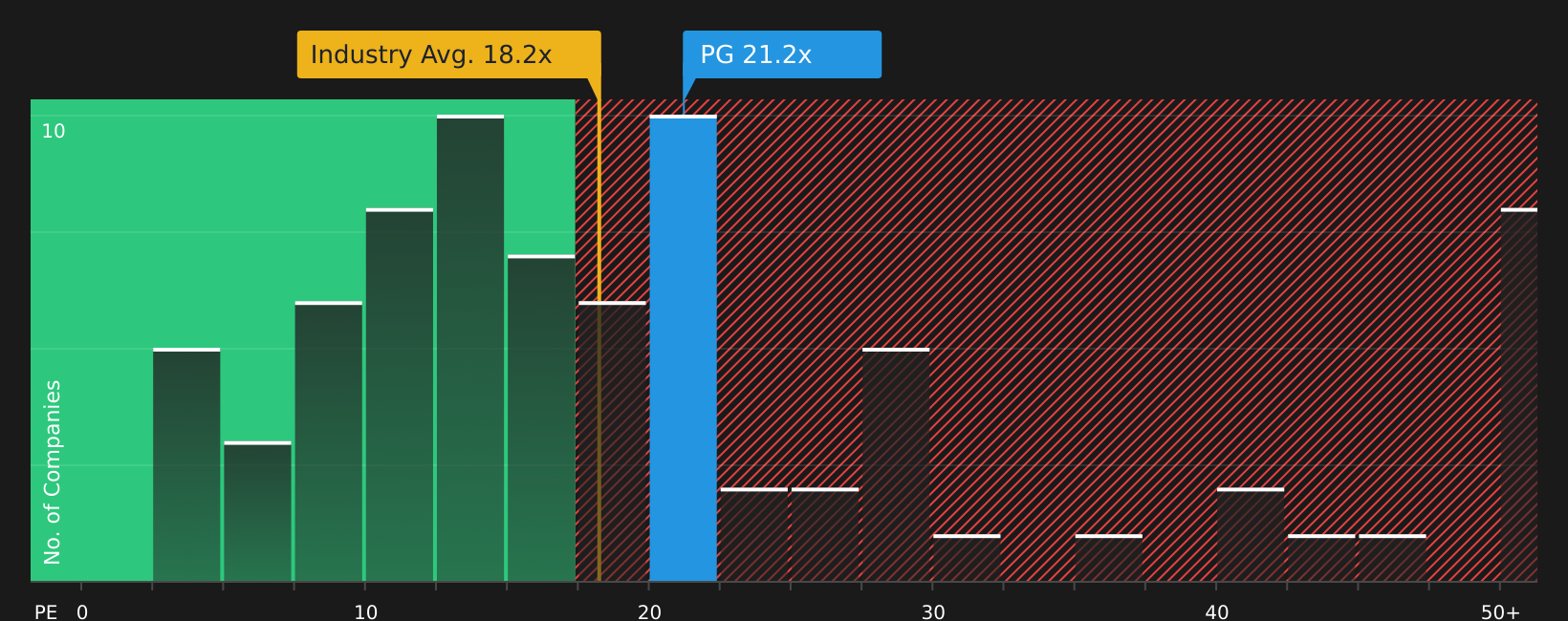

For a profitable company like Procter & Gamble, the P/E ratio is a useful way to relate what you pay per share to the earnings the company is currently generating. Investors usually accept a higher or lower P/E depending on what they expect for future earnings growth and how much risk they see in those earnings, so there is a range of what might be considered a normal or fair P/E for each stock.

Procter & Gamble currently trades on a P/E of 21.18x. This sits above the Household Products industry average P/E of 17.85x, but below the peer group average of 25.68x. Simply Wall St also applies a proprietary Fair Ratio, which for Procter & Gamble is 22.41x. This Fair Ratio reflects factors such as the company’s earnings growth profile, industry, profit margins, market capitalization and specific risks.

Because the Fair Ratio incorporates these company specific drivers, it gives a more tailored yardstick than a simple comparison with industry or peer averages. Against this measure, Procter & Gamble’s current P/E is slightly below the Fair Ratio, which indicates that the stock screens as modestly undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Procter & Gamble Narrative

Earlier we mentioned that there is an even better way to think about Procter & Gamble than looking at single valuation outputs. That approach is to use Narratives, where you tell a clear story about the company, link that story to a set of forecasts for revenue, earnings and margins, and let the platform translate that into a Fair Value you can compare with today’s price.

On Simply Wall St’s Community page, Narratives let you set out your own view of Procter & Gamble in plain language, connect it to assumptions such as a fair value of US$95.17, US$121.06, US$150.00 or US$186.00 per share, and then see whether your Fair Value suggests the stock is trading at a premium or a discount. This can help you decide whether it looks closer to a buy, a hold or a sell for your portfolio.

Because Narratives on the platform are updated when new data, news or earnings arrive, your Procter & Gamble story does not stay static. You can also see how different investors frame the same stock, from those who focus on emerging wellness themes like brain health to those who put more weight on margins, cost of capital and historical multiples.

For Procter & Gamble however we'll make it really easy for you with previews of two leading Procter & Gamble Narratives:

Each narrative applies different assumptions to the same stock, which is why the conclusions vary. Seeing the bullish and bearish cases side by side can help you decide which set of assumptions feels closer to your own view of Procter & Gamble.

Fair value: US$150.00 per share

Implied discount vs last close (US$148.50): about 1.0% undervalued

Revenue growth used in the narrative model: 8.09%

- The bullish narrative frames the recent share price weakness against a long list of global household brands, with the view that Procter & Gamble’s core franchise and consumer loyalty remain strong.

- Margins near 50% at the gross level and close to 18–19% at the net level, plus a high interest coverage ratio, are highlighted as signs of a resilient, cash generative business even when conditions are challenging.

- Concerns such as insider selling and a higher debt to equity ratio are acknowledged, but the narrative still argues the stock belongs on a watchlist, with valuation anchored around US$150 as a reasonable fair value reference point.

Fair value: US$121.06 per share

Implied premium vs last close (US$148.50): about 22.7% overvalued

Revenue growth used in the narrative model: 3.32%

- The bearish narrative accepts that Procter & Gamble has a wide moat, high returns on invested capital and solid credit ratings, but questions whether the current share price is justified given more modest projected growth.

- It leans on multiple valuation methods, including DDM, DCF and several historical multiples, with some of these approaches suggesting the stock screens as expensive when compared with the narrative’s own assumptions.

- After weighting these methods, the author settles on a fair value of about US$121 per share and concludes that Procter & Gamble looks overvalued on this framework, while encouraging investors to test their own inputs rather than relying on a single model.

If you want to see how other investors frame Procter & Gamble, these Narratives are a useful starting point rather than a final verdict. You can compare their assumptions with your own expectations for the business, then decide where you think fair value sits for your portfolio and risk tolerance.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Procter & Gamble on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Procter & Gamble? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.