Progressive (PGR) Valuation Check As Strong Earnings Meet Softer Analyst Outlook And Sell Rating

Progressive Corporation PGR | 195.25 | +1.03% |

Why Progressive’s earnings and analyst sentiment are pulling investor focus

Progressive (PGR) has moved into the spotlight after a strong full year 2025 earnings report coincided with softer analyst expectations for the current quarter and fiscal year, along with a Zacks Rank #4 (Sell).

That mix of solid reported results and more cautious forward estimates is creating a gap between what the company just delivered and what some analysts now project. This difference is what many investors are trying to understand.

Despite the strong 2025 earnings story and the upcoming CFO transition, the share price has softened recently, with a 30 day share price return of a 5.98% decline and a 1 year total shareholder return of a 14.05% decline, while the 5 year total shareholder return of 162.38% suggests longer term momentum has been stronger than the recent pullback.

If this earnings news has you rethinking where you want insurance and financial exposure in your portfolio, it could be a good time to broaden your search with 22 top founder-led companies

With earnings, analyst targets and a recent share price pullback all pointing in different directions, the key question is whether Progressive at about $202 already reflects its 2025 performance or if the market is underestimating what comes next.

Most Popular Narrative: 18.8% Undervalued

Progressive’s most followed narrative sets a fair value of $248.98 against the last close of $202.29, which is why some investors see a valuation gap worth studying more closely.

Persistent growth in U.S. vehicle ownership, population, and rising vehicle complexity expand the addressable market and increase future demand for auto insurance, which should underpin sustained top-line revenue growth for Progressive.

The accelerating shift toward digital consumer preference for price transparency and coverage customization gives Progressive an edge due to its flexible, usage-based (e.g., Snapshot) offerings and advanced segmentation, supporting both premium growth and higher customer retention.

Want to see what is really baked into that valuation gap? The narrative leans heavily on future revenue growth, evolving margins, and a higher earnings multiple than the market is pricing in today. Curious which assumptions have the biggest impact on that $248.98 figure, and how sensitive it is to even small changes in growth or profitability? The full narrative lays out those moving parts in detail.

Result: Fair Value of $248.98 (UNDERVALUED)

However, there are clear watchpoints here, including rising claim costs outpacing pricing and increasing competition that could pressure margins and test the current valuation narrative.

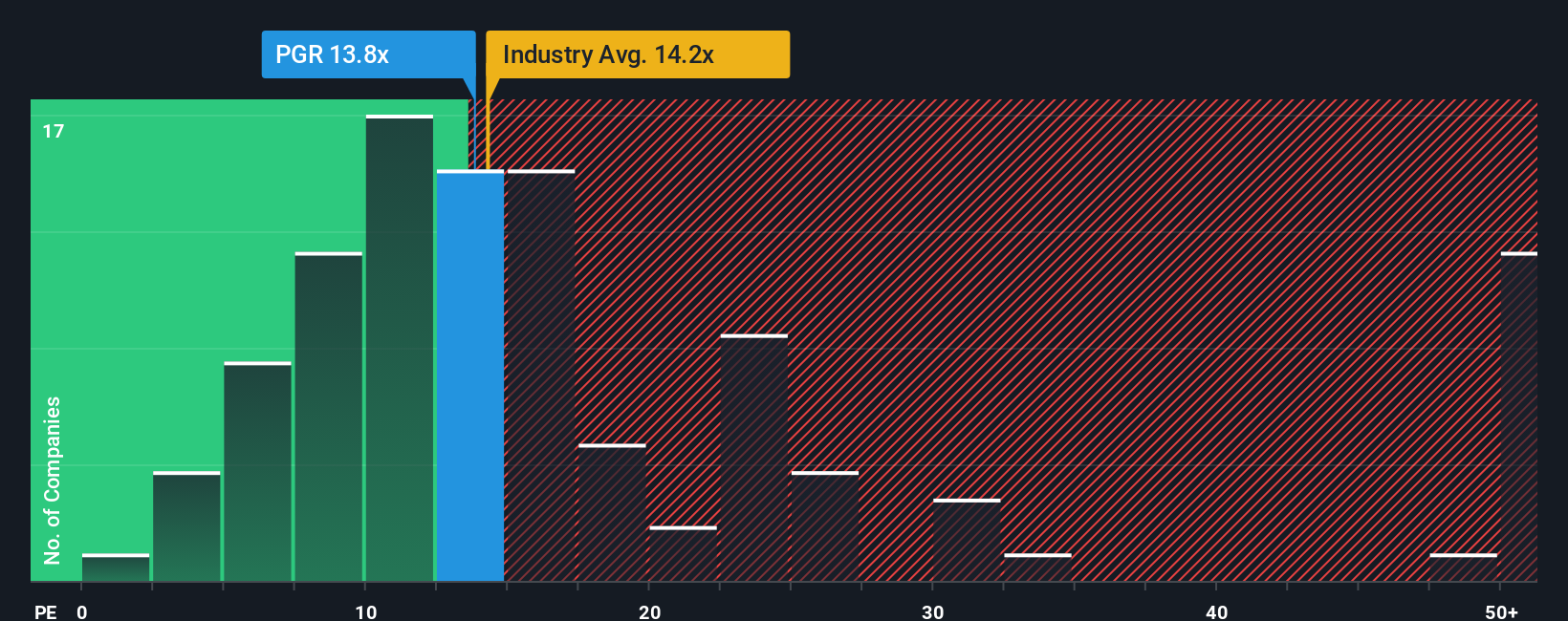

Another View: What P/E Says About The Current Price

The narrative-driven fair value of $248.98 suggests Progressive looks undervalued, but the simple P/E math tells a more cautious story. On 10.5x earnings, the shares trade above peer companies at 9.3x, yet below the US Insurance industry at 13x and below a fair ratio of 11.5x.

That mix hints at some valuation risk versus closer peers but also room for the market to move toward the higher fair ratio. For you, the real question is whether Progressive ends up priced more like its immediate competitors, or closer to the broader industry and that fair ratio.

Build Your Own Progressive Narrative

If you see the numbers differently or prefer to rely on your own work, you can pull the same data, stress test your assumptions, and build a custom view of Progressive in just a few minutes, then Do it your way

A great starting point for your Progressive research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Progressive has sharpened your thinking, do not stop here. Use the Simply Wall St screener to uncover fresh stock ideas that could better fit your goals.

- Target potential mispriced opportunities by reviewing our list of 52 high quality undervalued stocks that pair solid fundamentals with room for the market to reassess.

- Prioritise strength and resilience by scanning solid balance sheet and fundamentals stocks screener (45 results) that may better handle stress without stretching their finances.

- Spot underfollowed prospects early by checking the screener containing 24 high quality undiscovered gems that other investors might not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.