Quality of Life Trends Shaping U.S. REIT Stocks Worth Watching

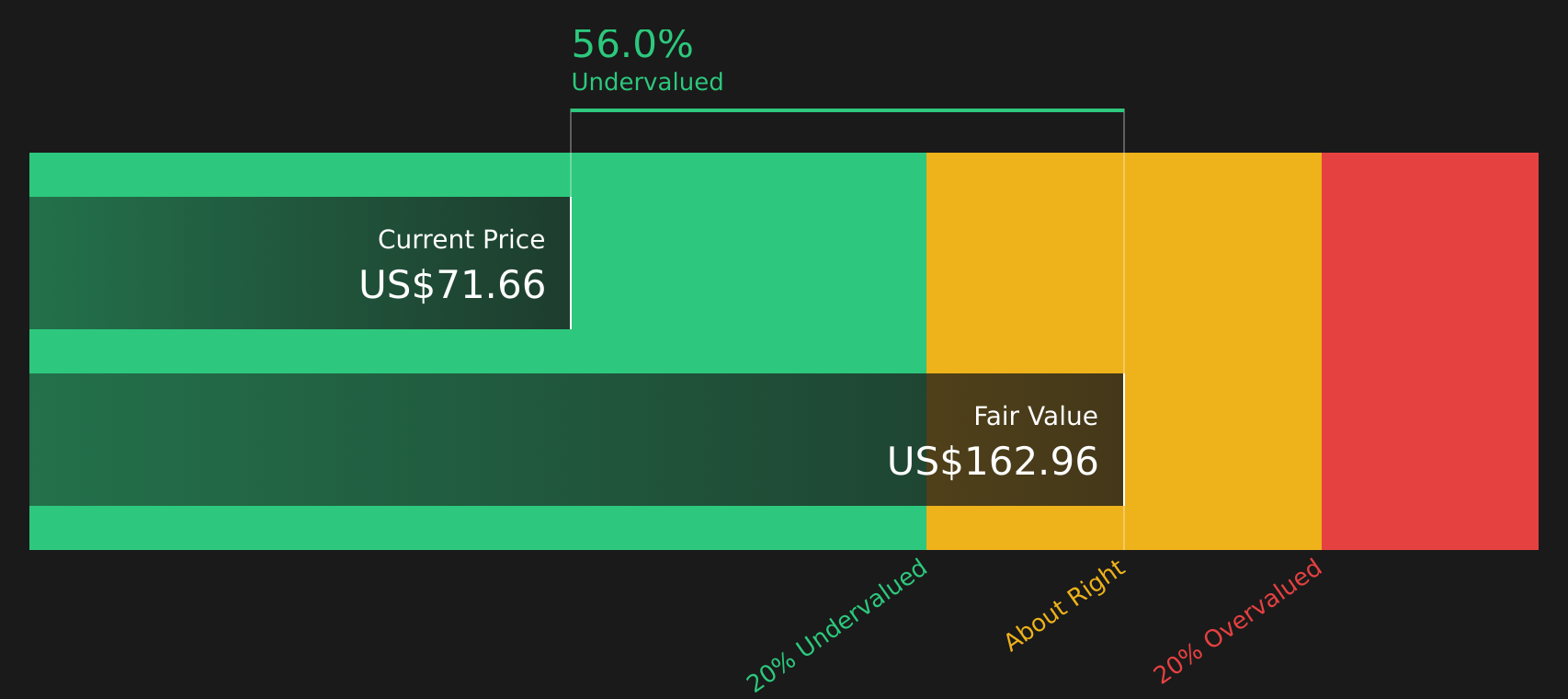

Millrose Properties Inc Class A MRP | 0.00 |

Quality of life is moving higher up the list of things companies care about when choosing where to put offices and attract employees, and that shift can ripple straight into U.S. Real Estate Investment Trusts focused on office and multifamily properties. As firms respond to return to office policies and talent shortages, states that score better on safety, health, childcare, and local laws may see different demand patterns for both commercial and residential space. This article walks through three REIT stocks that appear especially exposed to this quality of life driven trend.

Millrose Properties (MRP)

Overview: Millrose Properties (MRP) is a Miami based REIT that acquires and prepares residential land into finished homesites, supplying large homebuilders with a predictable, just in time pipeline of lots supported by a data driven technology platform and independent due diligence on each project.

Operations: Millrose Properties generates about US$712.7 million in revenue from its REIT commercial segment, all from the United States.

Market Cap: US$4.7b

Investors looking at Millrose Properties get targeted exposure to housing supply and quality of life trends, as the company finances homesites for large builders in states that are drawing both workers and employers. Its technology backed underwriting and focus on finished lots aim to create relatively predictable income, and recent inclusion in defensive equity indices has raised its profile. At the same time, high leverage, a relatively new leadership team and reliance on continued homebuilding activity mean the situation carries risk. The combination of meaningful dividend payments, valuation support and exposure to quality of life driven migration may make Millrose worth a closer look for long term investors.

Millrose Properties sits at the intersection of housing supply, quality-of-life migration and income-focused real estate, but the real story sits inside the 5 key rewards and 1 important warning sign

Ryman Hospitality Properties (RHP)

Overview: Ryman Hospitality Properties (RHP) is a hotel and entertainment REIT built around large convention resorts like the Gaylord hotels and JW Marriott properties, paired with country music and live events brands such as the Grand Ole Opry and Ryman Auditorium. This gives it a mix of meeting, leisure, and experiential revenue streams.

Operations: Ryman Hospitality Properties generates about US$2.23b from Hospitality and US$423.6m from Entertainment, with a small segment adjustment of US$10.0m, all sourced from the United States.

Market Cap: US$7.9b

Ryman Hospitality Properties operates at the intersection of quality of life, experiential travel, and business meetings, with large resort assets in high quality of life markets and an entertainment arm anchored by the Grand Ole Opry. The stock screens as expensive on P/E. Some investors see support in its discount to fair value estimates, high but leverage driven ROE, and a convention pipeline that ties into states benefitting from corporate relocations. At the same time, high debt, an unstable dividend history, and sensitivity to rates and group travel mean any downturn or financing squeeze could affect the business quickly. The push to expand Gaylord Opryland and the ongoing review of Opry Entertainment Group raise questions about how much upside and risk is actually priced in.

Ryman Hospitality Properties appears to be a pure play on quality-of-life travel, but the real tension lies in the relationship between its P/E, high leverage and group travel exposure. That balance only becomes clear in the 2 key rewards and 2 important warning signs (1 is major!)

W. P. Carey (WPC)

Overview: W. P. Carey (NYSE:WPC) is one of the largest net lease REITs, owning more than 1,700 single tenant industrial, warehouse and retail properties across roughly 185 million square feet in the U.S. and Europe, with long term leases where tenants handle most operating costs and rents typically step up over time.

Market Cap: US$16.0b

W. P. Carey stands out if you care about how quality of life trends and corporate site selection filter through to rental income. Its focus on operationally critical industrial and warehouse assets, long leases with inflation linked or fixed rent escalators, and sale leaseback demand can support steady cash flows, even as earnings growth is expected to be slower than the broader U.S. market. On the flip side, leverage, reliance on single tenant leases, an unstable dividend history and tenant specific events like the Hellweg bankruptcy highlight that credit risk and refinancing decisions matter. The key consideration is whether the combination of diversified assets in higher quality of life markets, ESG focus and current valuation compensates for those risks.

W. P. Carey’s long leases and sale leaseback focus can look calm on the surface, but tenant risk and refinancing choices may be quietly reshaping the story; the real twist sits inside the 3 key rewards and 2 important warning signs (1 is major!)

The three REIT stocks covered here are only a starting point, and the full U.S. Real Estate Investment Trusts (REITs) Focused on Office and Multifamily Properties in High Quality-of-Life States screener surfaces 3 more companies with equally compelling quality-of-life-driven stories across office and multifamily real estate. Use Simply Wall St to identify and analyze the exact catalysts, risk profiles, and narratives that matter to you so you can focus on the highest conviction opportunities in this corner of the market.

Take Control of Your Investment Journey

If Ryman Hospitality Properties or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Seeking Fresh Alternatives?

Fresh ideas can move from quiet to breakout before most investors react, and the strongest stories rarely stay under the radar for long, so act now.

- Spot companies building real momentum before they are widely talked about by scanning a curated set of 19 high quality undiscovered gems that most investors have not caught yet.

- Target consistent cash flow potential with a focused pool of 9 dividend fortresses designed to help you find income ideas while yields and entry points still look appealing.

- Ride structural growth in digital infrastructure by reviewing 52 AI infrastructure stocks before the story goes mainstream and the early pricing window starts dropping away.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.