RadNet (RDNT) Stock Could Be 39.3% Below Fair Value After Reporting Pro Launch

RadNet, Inc. RDNT | 0.00 |

RadNet (RDNT) has drawn fresh attention after launching Reporting Pro, an AI-powered reporting platform that combines speech recognition, clinical AI findings and generative AI to support radiology workflows across high-volume clinical settings.

RadNet’s recent Reporting Pro launch and its expanded term loan facilities come after a period where the share price return has declined 24.26% year to date and the 1-year total shareholder return is slightly lower. However, the 3-year total shareholder return of 64.04% and 5-year total shareholder return of 58.81% indicate longer term holders have seen stronger gains.

If AI in radiology has your attention, this is a good moment to see what else is out there and review 38 healthcare AI stocks

With RadNet shares down 24.26% year to date yet still carrying multi year gains and a reported intrinsic discount of 39.27%, investors are left asking: is there real upside left here, or is future growth already priced in?

Most Popular Narrative: 40.1% Undervalued

Against RadNet's last close at $53.74, the most followed narrative points to a fair value of $89.75, framing a sizeable valuation gap that rests on ambitious growth and profitability assumptions.

Ongoing investments in AI-powered imaging solutions (e.g., DeepHealth, See-Mode, iCAD) are materially increasing center throughput, boosting capacity utilization, and driving more high-margin advanced procedures, directly enhancing both revenue growth and EBITDA margins as adoption scales through 2026.

Curious what has to happen for RadNet to earn materially higher profits on a much larger revenue base and still support a premium earnings multiple? The narrative lays out a detailed path for revenue growth, margin expansion and future valuation that goes well beyond headline guidance.

Result: Fair Value of $89.75 (UNDERVALUED)

However, the RadNet narrative still hinges on continued high imaging demand and favorable reimbursement terms, both of which could shift and undermine today’s optimistic assumptions.

Another View on RadNet’s Valuation

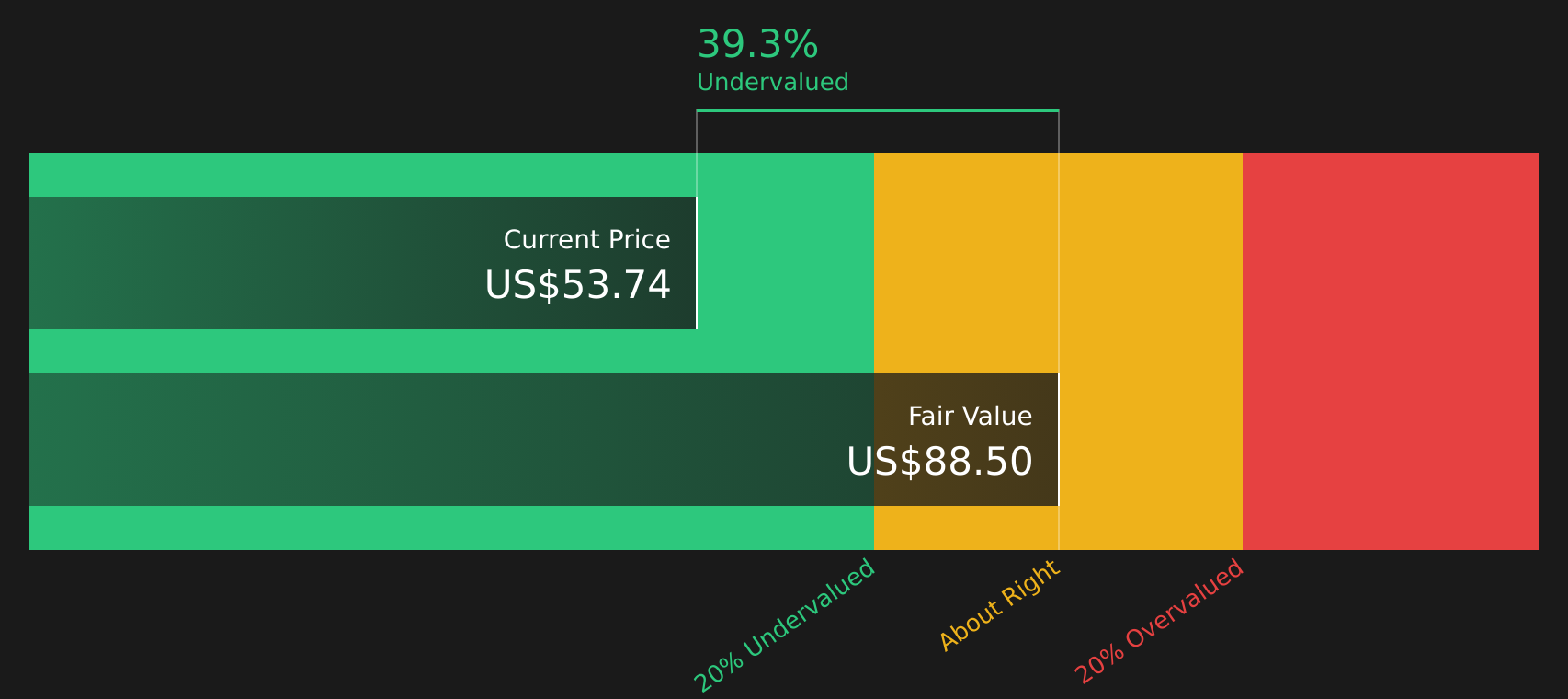

The narrative argues RadNet is about 39.3% below an estimated fair value of $88.50 using the SWS DCF model, which also classifies the stock as undervalued. That is a very different signal from multiples that look expensive. Which lens do you trust more when the story is this mixed?

Next Steps

With RadNet attracting both optimism and concern, this is a moment to move quickly, review the evidence yourself, and weigh the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond RadNet?

Do not stop your research with RadNet. Broaden your watchlist with other stocks that fit clear, focused criteria using the Simply Wall St Screener.

- Hunt for quality at a discount by reviewing companies flagged in the 45 high quality undervalued stocks.

- Prioritize resilience and peace of mind by checking out stocks in the 66 resilient stocks with low risk scores.

- Spot potential standouts early by scanning the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.