Reassessing Rivian Automotive (RIVN) Valuation After Recent Mixed Share Price Performance

Rivian Automotive, Inc. Class A RIVN | 14.69 | -3.92% |

Rivian Automotive stock reaction and recent performance snapshot

Rivian Automotive (RIVN) has attracted attention after recent trading left the shares around $15.01, with the stock mixed over the past week and month, and weaker over the past 3 months.

For context, the stock shows a 1 day return of about a 2.1% decline, a roughly flat return over the past week, around a 1.8% gain over the past month, and about a 12.9% decline over the past 3 months.

At around $15.01, Rivian’s shorter term share price return has been mixed, while the year to date share price return of a 22.7% decline contrasts with a 1 year total shareholder return of about 30.4%. This suggests sentiment has been shifting as investors reassess growth potential and execution risks.

If Rivian’s recent swings have you rethinking your watchlist, this could be a moment to see what else is available with our screener of 35 AI infrastructure stocks.

With Rivian trading around $15.01 and sitting at about a 22.7% year to date decline alongside a 30.4% 1 year total return, you have to ask: is this a genuine reset, or is the market already pricing in future growth?

Most Popular Narrative: 40.9% Undervalued

According to McLarenFund, the most followed narrative sees Rivian’s fair value at $25.41 per share compared with the recent $15.01 close, creating a wide gap that hinges on execution across vehicles, software and partnerships.

Gen2 R1T and R1S, refinement from feedback and lower cost building R2, R3 and R3X lower cost options for different audience. JV with VW and the ripple effects for Software and Electrical Architecture deals through not just VW but also others. Utilizing Supplier leverage from VW. Amazon expanding EDV's in Europe with recent order. Europe expansion in general. RJ's focus on what's important approach while keeping out of politics and remaining neutral gives others including that are building up hate for Tesla a great alternative. Revenue from existing and expanding charging infrastructure, not just for Rivian's but also third party OEM's. Gross Profitability guidance for FY25

Want to see why this narrative supports a much higher price than today’s? The story leans heavily on rapid revenue expansion, improving margins and a future earnings multiple that assumes real scale. Curious which parts of Rivian’s line up and software stack carry the most weight in that fair value? The full narrative lays out the assumptions in detail.

Result: Fair Value of $25.41 (UNDERVALUED)

However, this hinges on Rivian turning a US$3,646m loss and rapid revenue growth into durable profitability, while executing new models and partnerships without major delays or cost surprises.

Another View on Rivian’s Valuation

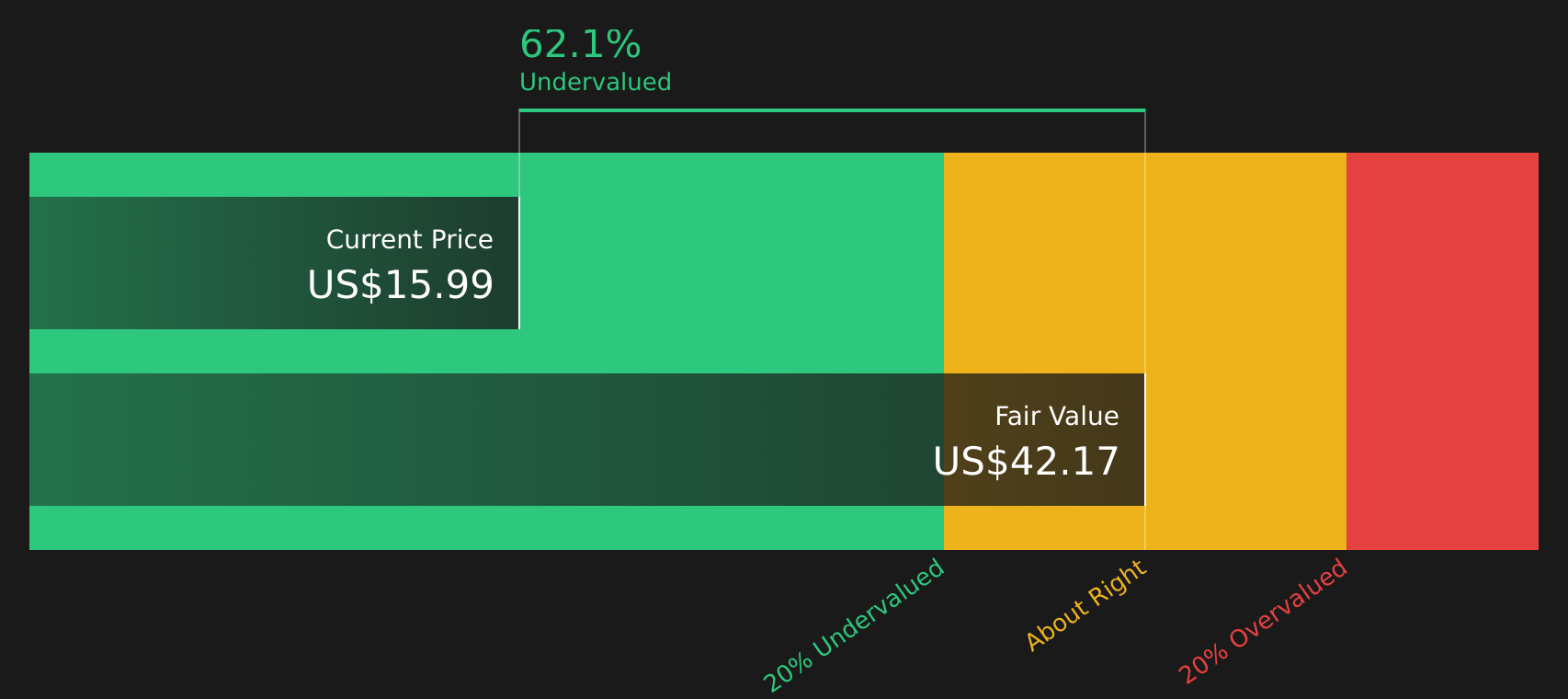

The user narrative leans on fast growth and a future earnings multiple, but our DCF model points to a very different anchor, with a fair value of $42.91 versus the current $15.01. That still flags Rivian as undervalued, but how comfortable are you with the cash flow assumptions behind that gap?

Next Steps

If this mix of optimism and caution around Rivian resonates with you, take a moment now to review the data and weigh up 2 key rewards and 2 important warning signs.

Ready to scout more stock ideas?

Before you move on, you can build a more focused watchlist by reviewing a few stock ideas that may suit your style and risk tolerance.

- Target income by reviewing companies with at least a 5% yield in our collection of 13 dividend fortresses.

- Look for quality at a sensible price by exploring our group of 45 high quality undervalued stocks.

- Prioritise resilience by scanning stocks with stronger balance sheets and fundamentals in our solid balance sheet and fundamentals stocks screener (41 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.