Reliable US Dividend Growth Stocks For Steadier Income In A Stable Rate Outlook

Rockwell Automation, Inc. ROK | 0.00 |

With the Supreme Court reinforcing the Federal Reserve’s independence and S&P Global reaffirming the U.S. AA+ debt rating, the market backdrop for dividend growth stocks has shifted in an important way. Confidence in U.S. Treasuries and the bond market can influence how investors think about income, stability, and risk across portfolios. This article looks at how that news interacts with a U.S. Dividend Growth Stocks screener and highlights three stocks that appear positively exposed to the ruling, helping you assess where resilient balance sheets and consistent dividend growth might fit into your long term investing playbook.

A. O. Smith (AOS)

Overview: A. O. Smith is a long established water technology company that sells residential and commercial water heaters, boilers, heat pumps, and water treatment systems across North America, China, Europe, and India, serving everyday needs in homes, hospitals, hotels, and other critical facilities.

Operations: A. O. Smith generates most of its revenue from North America at about US$2.99b, with the rest of the world contributing roughly US$0.85b and a small inter segment elimination of US$31.4m.

Market Cap: US$8.5b

A. O. Smith stands out in the Dividend Growth Stocks screener because it combines essential, replacement driven demand with a multi decade record of dividend increases, a 2.3% yield, and a P/E that screens as cheaper than many peers, even after a year when earnings growth was only 1% and guidance was trimmed on China softness. The company is leaning into higher efficiency and connected products and shifting water treatment toward higher margin dealer and e commerce channels, all while keeping returns on equity around 28% and leadership and CFO transitions structured for continuity. For investors who care about dividend reliability, balance sheet strength, and how a more stable Fed and bond market can support steady income stocks, A. O. Smith offers more to unpack beneath the headline numbers.

A. O. Smith’s rich dividend history and essential product line might not be the full story. The real question is whether the current P/E and balance sheet fully reflect its long term cash potential in the DCF valuation analysis for A. O. Smith.

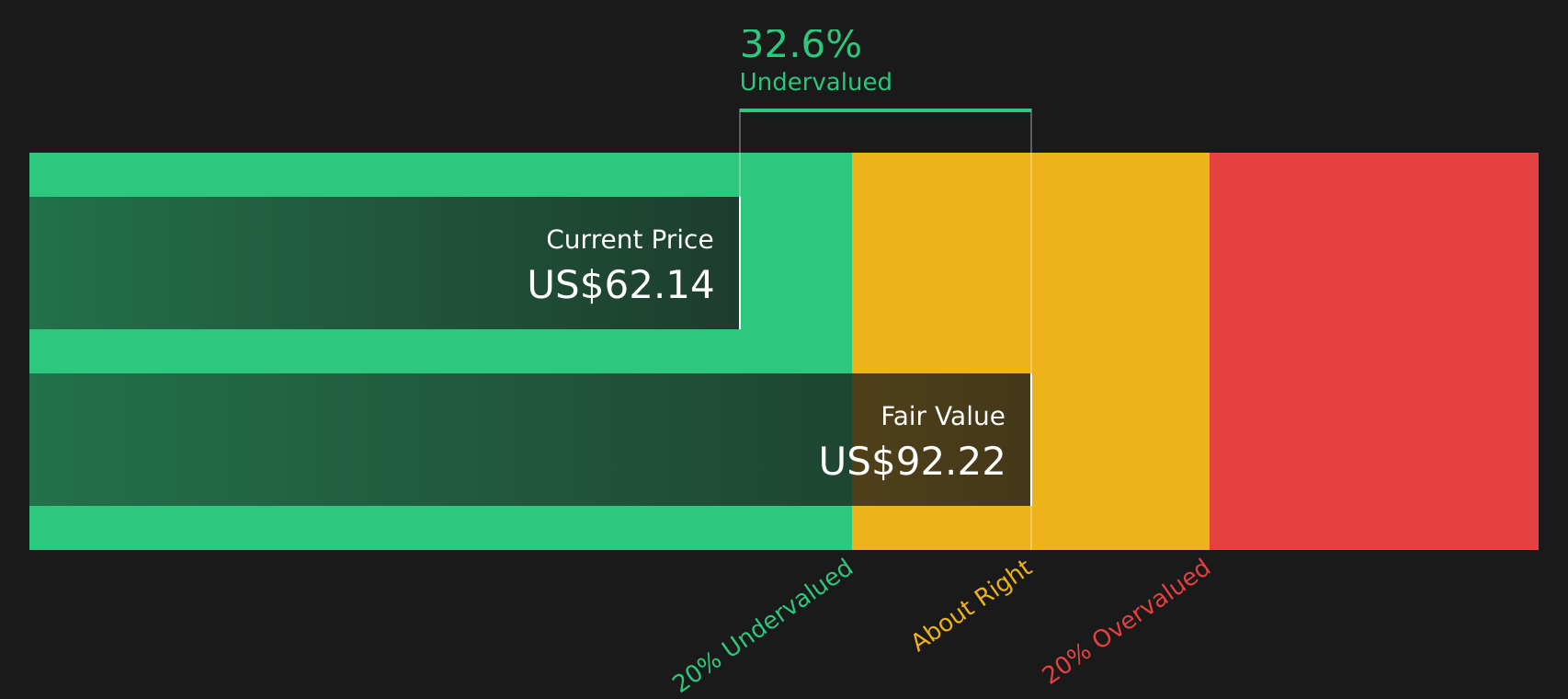

Rockwell Automation (ROK)

Overview: Rockwell Automation is a Milwaukee based industrial company that helps factories and warehouses run smarter by providing automation hardware, software, and services that connect machines, data, and workers across sectors such as automotive, semiconductors, food and beverage, and energy.

Operations: Rockwell Automation generates most of its revenue from Intelligent Devices at about US$4.02b, followed by Software & Control at roughly US$2.60b and Lifecycle Services at about US$2.19b.

Market Cap: US$53.67b

Rockwell Automation may be worth a closer look for investors who are interested in dividend growth companies tied to long term themes such as factory automation, AI enabled software, and reshoring. The business is focusing more on higher margin software and recurring services, yet still earns much of its income from equipment and project work, so delays in customer capital spending and a high debt load are important considerations for returns. At the same time, a long dividend track record, a recent buyback expansion, and recognition for advanced manufacturing projects indicate that management is confident in the company’s position. With the Federal Reserve’s independence reaffirmed and bond markets steadier, Rockwell Automation is part of the group of large cap industrials that many investors use as core income holdings, but its valuation and leverage mean the full story warrants careful scrutiny.

Rockwell Automation’s push into higher margin software and services could be masking a very different earnings profile than its equipment heavy past, and the real tension sits in the 1 key reward and 1 important warning sign

Donaldson Company (DCI)

Overview: Donaldson Company makes filtration systems and replacement parts that keep air, liquids, and industrial processes clean and running reliably, serving equipment makers and end users across construction, mining, transportation, factories, food and beverage, aerospace, and life sciences.

Operations: Donaldson generates most of its revenue from Mobile Solutions at about US$2.37b, followed by Industrial Solutions at roughly US$1.11b and Life Sciences at about US$325m.

Market Cap: US$10.25b

Donaldson Company combines more than 25 years of consecutive dividend growth, membership in the S&P High Yield Dividend Aristocrats, and a P/E that screens below the Machinery industry average. These characteristics help it stand out on a dividend growth list. Growth in higher margin filtration areas such as Life Sciences and gas and liquid handling, along with the Facet Filtration acquisition, is supporting earnings quality and recurring aftermarket revenue, while recent quarters have reported record sales and improved margins. However, slower revenue growth than the wider market, dependence on legacy engine filtration and aftermarket parts, and softer signals in some regions mean the story carries risks. With the Supreme Court reinforcing Federal Reserve independence and supporting confidence in income focused stocks, the key question for Donaldson is what that mix of resilience and growth potential might be worth over time.

Donaldson Company’s filtration shift toward higher margin areas and recurring aftermarket revenue could be masking a very different earnings engine. Read the analyst forecasts for Donaldson Company to see what the market might be missing next.

The three dividend growth stocks in this article are just a starting point, and the full U.S. Dividend Growth Stocks screener surfaces 17 more large U.S. companies with consistent dividend growth and equally compelling stories to weigh up. Use Simply Wall St to identify, filter, and analyze the specific catalysts, balance sheet strength, and dividend narratives that match your highest conviction ideas so you can focus on the opportunities that fit your income strategy most effectively.

Take Control of Your Investment Journey

If Rockwell Automation or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies Past?

Fresh opportunities do not stay quiet for long. Once momentum builds, ideal entry points can get caught flying away under the radar, so consider acting before they become crowded.

- Use the 74 resilient stocks with low risk scores to spot companies with cash, pricing power, and lower risk scores before the broader market focuses more on stability and consistency.

- Explore the 35 power grid technology and infrastructure stocks to look for structural growth ideas linked to infrastructure spending while the theme is still developing.

- Review the curated 29 robotics and automation stocks for automation leaders with solid fundamentals and consider how robotics and factory upgrades might fit into your long-term positioning.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.