Republic Services (RSG) On Strong Q1 And Deal Approval Faces A Valuation Test

Republic Services, Inc. RSG | 0.00 |

Republic Services (RSG) has been in focus after reporting first quarter results that beat analyst expectations on adjusted operating income. The company also received supportive analyst ratings and regulatory approval to acquire TD*X Associates assets.

The recent 6.3% 1 month share price return and 1.9% 7 day share price gain for Republic Services suggest firming momentum, even as the 1 year total shareholder return is down 12% and longer term 3 and 5 year total shareholder returns remain positive.

If strong earnings and project announcements have your attention, it can be helpful to see what else is moving in related themes, starting with 35 power grid technology and infrastructure stocks

With Republic Services posting steady revenue and net income growth and trading around a 17% intrinsic discount alongside a gap to analyst targets, the key question is whether investors are looking at value or at a stock that already reflects future growth.

Most Popular Narrative: 12.5% Undervalued

With Republic Services last closing at $213.08 against a narrative fair value of about $243.58, the current pricing gap raises questions about what future cash flows the market is and is not reflecting.

Sustainability efforts such as the development of Polymer Centers and the Blue Polymers joint venture could drive future revenue growth by enhancing plastic circularity and decarbonization. These operations are expected to contribute to earnings starting in the second half of 2025.

There is a detailed playbook sitting behind that valuation. It blends steady revenue expansion, firmer margins and a richer earnings multiple than the wider Commercial Services sector. Curious which assumptions really carry the fair value to its target level and how much depends on those new projects delivering as planned? The full narrative lays out the math and the timing behind that view.

Result: Fair Value of $243.58 (UNDERVALUED)

However, there are pressure points that could challenge this Republic Services narrative, including softer construction and manufacturing volumes, as well as execution risk around the planned US$1b acquisition pipeline.

Another View on Republic Services Valuation

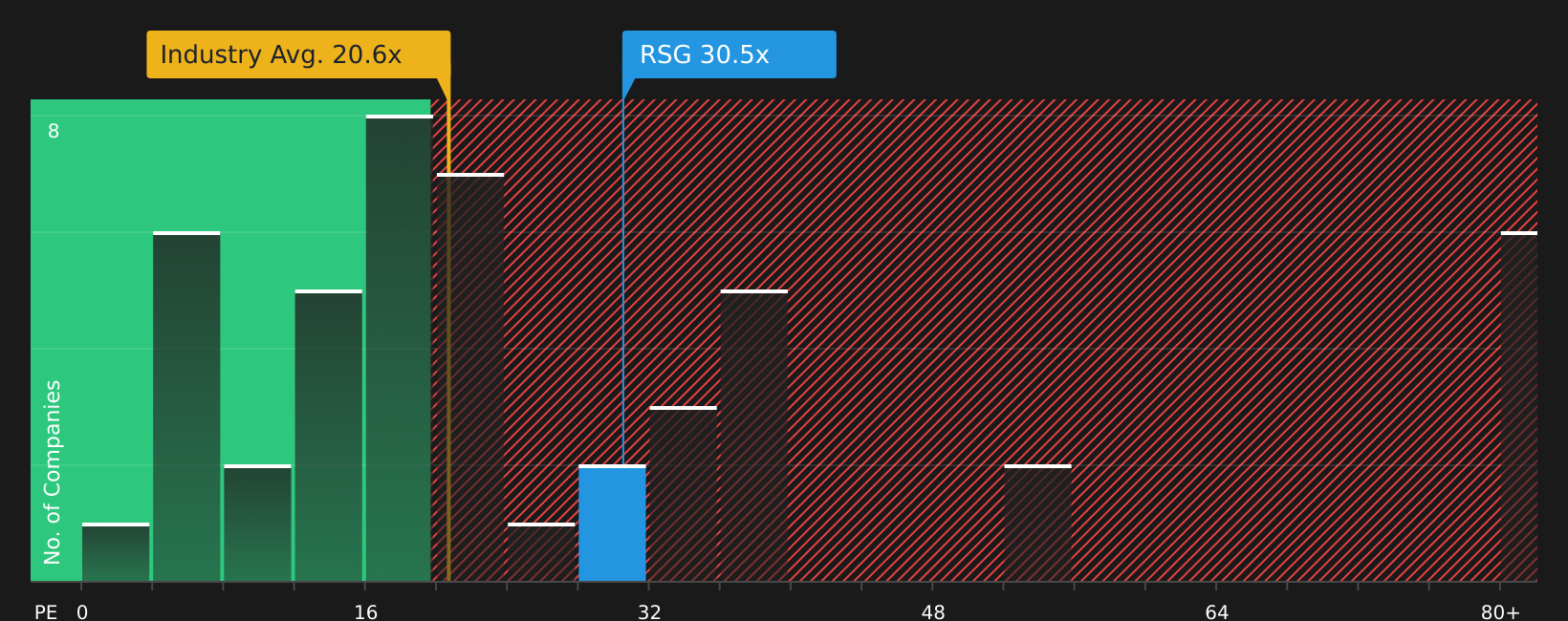

While the narrative fair value suggests Republic Services is 12.5% undervalued, the P/E picture is less forgiving. The stock trades on a 30.2x P/E, above both the US Commercial Services industry at 22.1x and a fair ratio of 22.7x. This points to valuation risk if sentiment cools.

For investors weighing these mixed signals, the key question is whether the cash flow story or the earnings multiple will matter more when the next shift in expectations arrives.

Next Steps

With a mix of optimism around Republic Services and clear concerns on the risk side, now is a good time to review the data yourself, weigh both sides of the argument, and see how the 3 key rewards and 1 important warning sign fits with your own view.

Looking for more ideas beyond Republic Services?

If Republic Services has sharpened your focus, do not stop there. Broadening your watchlist with quality stocks and fresh themes can keep your portfolio ideas moving.

- Target resilient compounding potential by scanning companies in the 43 high quality undervalued stocks that combine quality fundamentals with prices below their assessed worth.

- Prioritize consistency and income by reviewing the 10 dividend fortresses that pair higher yields with staying power through different market conditions.

- Protect your downside first by checking the 74 resilient stocks with low risk scores that show sturdier balance sheets and fewer red flags than the broader market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.