ResMed (RMD) Stock After 21% Year-To-Date Slide Is There An Opportunity Now

ResMed Inc. RMD | 0.00 |

- If you are wondering whether ResMed at around US$192 per share offers value or just more volatility, the starting point is understanding what the current price actually reflects.

- The stock is down 1.0% over the past week, 5.6% over the past month, and 21.4% year to date, with a 23.0% decline over the last year and 16.4% over five years, which may change how investors are thinking about both risk and opportunity.

- Much of the recent conversation around ResMed has focused on how the company is positioned within medical equipment and sleep apnea treatment, especially as competitors refine their offerings and investors reassess expectations for demand. These themes help frame why the share price has moved and why valuation is front of mind for many holders.

- On Simply Wall St’s 6 point valuation check, ResMed scores 5 out of 6. The rest of this article will walk through what that means across different valuation methods, then finish with a more holistic way to think about what the stock is really worth.

Approach 1: ResMed Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts those projections back to today using a required rate of return. The aim is to estimate what the business might be worth based on the cash it is expected to generate for shareholders.

For ResMed, the model used is a 2 Stage Free Cash Flow to Equity approach, working off last twelve months free cash flow of about $1.75b. Analyst inputs are used for the nearer years, and Simply Wall St then extrapolates further out. For example, projected free cash flow for 2028 is $1.79b, with subsequent years continuing to be modeled out to 2035 using gradually changing growth assumptions. Each of these annual figures is discounted back to a present value and then summed.

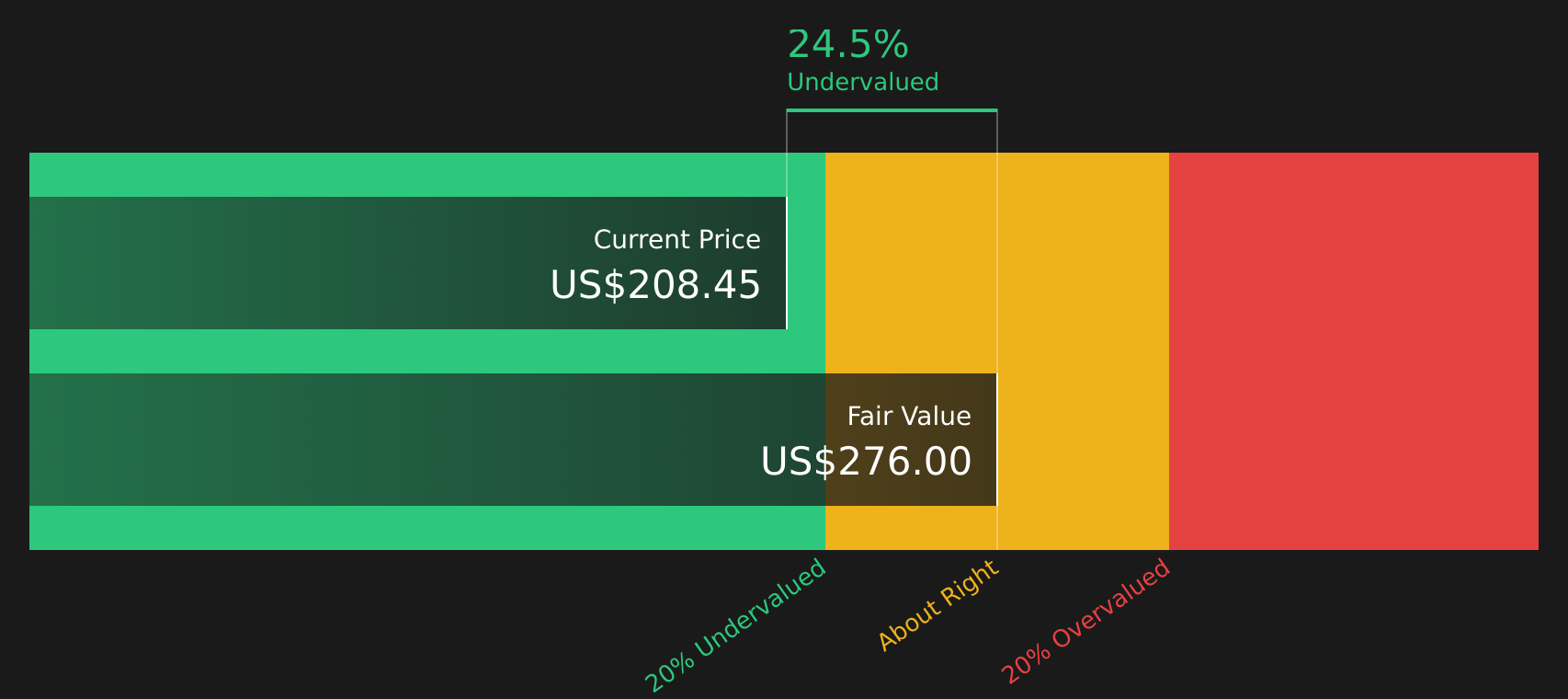

On this basis, the DCF model arrives at an estimated intrinsic value of about $277.89 per share. Against a current share price around $192, this implies a 30.8% discount, which indicates the stock screens as undervalued on this methodology.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ResMed is undervalued by 30.8%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: ResMed Price vs Earnings

For profitable companies, the P/E ratio is a useful way to connect what you pay for the stock with what the business is currently earning. It lets you see how many dollars investors are willing to pay today for each dollar of earnings.

What counts as a “normal” P/E depends a lot on growth expectations and risk. Higher expected earnings growth or a perception of lower risk can justify a higher multiple, while slower growth or higher uncertainty can pull that number down.

ResMed currently trades on a P/E of 18.28x, compared with the Medical Equipment industry average of about 24.81x and a peer average of 28.15x. Simply Wall St’s Fair Ratio for ResMed is 23.21x. This Fair Ratio is a proprietary estimate of what a more tailored P/E might look like once factors such as earnings growth, profit margins, industry, market cap and company specific risks are considered.

Because it blends these company specific drivers, the Fair Ratio aims to be more informative than a simple comparison with peers or the broad industry, which may have very different profiles. Set against the current P/E of 18.28x, the Fair Ratio of 23.21x indicates that the stock screens as undervalued on this metric.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your ResMed Narrative

Earlier it was mentioned that there is an even better way to think about valuation. Meet Narratives, a simple tool on Simply Wall St’s Community page that lets you set out your story for ResMed and tie it directly to your own forecasts for revenue, earnings, margins and fair value. You can then compare that fair value with the current price to help you decide whether the stock fits your goals. The view updates automatically as new earnings or news arrive. For example, one investor might adopt a more optimistic Narrative that lines up with a Fair Value near the higher analyst target of US$340.0, while another might choose a cautious Narrative that anchors closer to the US$180.0 end of the range, both using the same shared data but expressing very different expectations.

For ResMed, however, we will make it really easy for you with previews of two leading ResMed Narratives:

Fair value in this bullish Narrative: US$270.60

Implied discount versus the recent price of US$192.39: about 29% below this Narrative fair value

Revenue growth assumption: 7.67% a year

- Acquisitions, broader sleep health awareness and digital tools are used to widen the diagnosis-to-treatment funnel and support revenue and earnings over time.

- Analysts using this Narrative build in higher profit margins and a P/E of 23.9x by 2029, with earnings of about US$2.0b and earnings per share of US$13.91.

- This view depends on continued execution in connected devices, software and manufacturing efficiency, as well as manageable regulatory and competitive risks.

Fair value in this bearish Narrative: US$182.45

Implied premium versus the recent price of US$192.39: about 5% above this Narrative fair value

Revenue growth assumption: 6.89% a year

- This Narrative leans on more cautious revenue and margin assumptions, including a P/E of 17.7x by 2029 and earnings of about US$1.8b.

- Concerns center on GLP 1 therapies, cost pressures, integration of new acquisitions and the risk that extra spending on digital and primary care outreach does not fully translate into earnings.

- The bear case still allows for growth but assumes investors will be less willing to pay a high multiple if competition, reimbursement or execution risks weigh on sentiment.

If you want to see how other investors are joining the dots between these types of Narratives and the latest numbers on ResMed, you can use the Community page as a jumping off point with Curious how numbers become stories that shape markets? Explore Community Narratives.

Do you think there's more to the story for ResMed? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.