ResMed (RMD) Stock Looks Reasonable After A 23% Fall

ResMed Inc. RMD | 0.00 |

ResMed stock has fallen 23.2% over the past year, yet both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiples currently point to the shares trading at a discount to what the business may be worth.

- Over the last 12 months the share price declined 23.2%, which means the market has already reset expectations even as valuation indicators lean supportive.

- Recent coverage has highlighted recurring revenue from sleep apnea devices and software as a potential support for long term cash flows, while questions around competition and the impact of weight-loss treatments remain a clear risk to those expectations.

- On Simply Wall St's broader valuation checks, ResMed screens as undervalued in 5 of 6 tests, indicating that the stock appears inexpensive on several different metrics rather than just one headline ratio.

For investors, the debate is whether ResMed's recent share price weakness has already priced in the key risks or if the current discount to intrinsic value is justified.

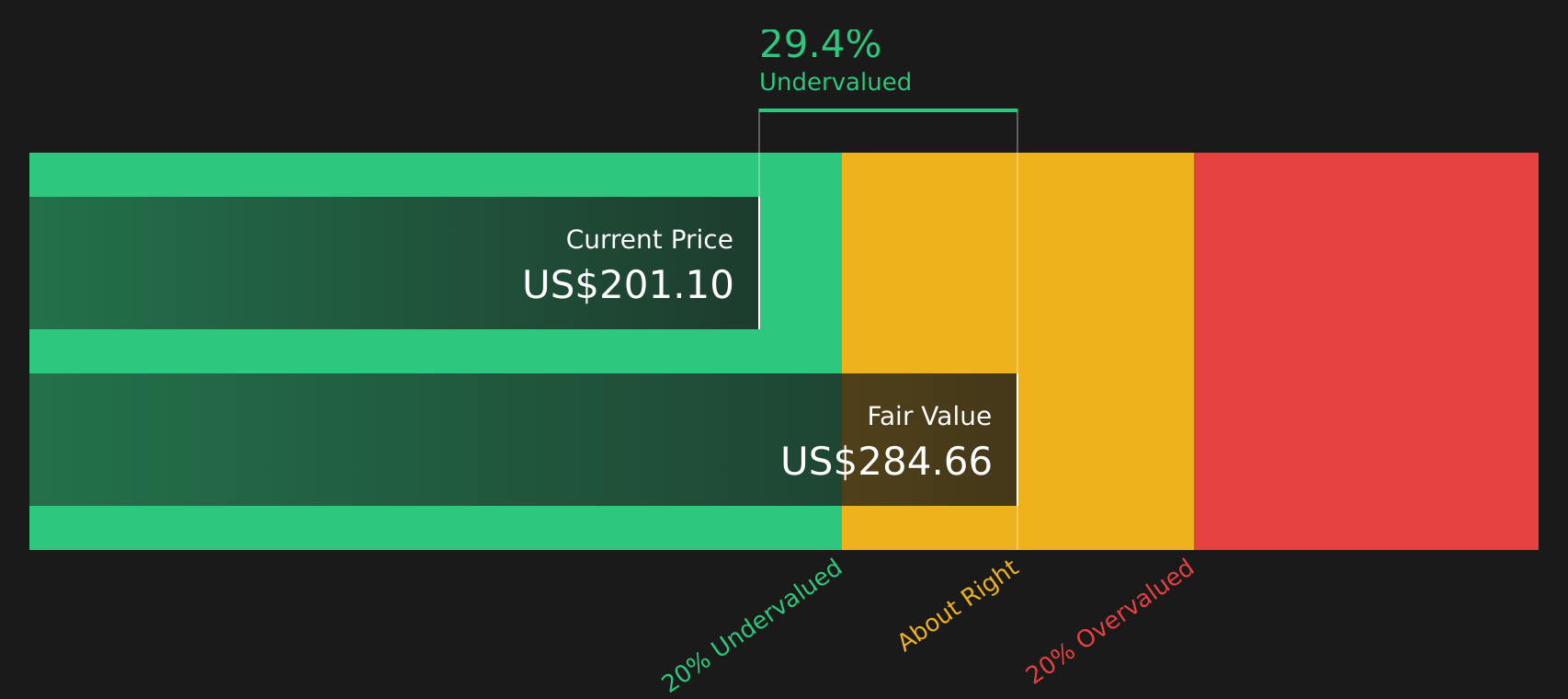

Does ResMed Look Undervalued on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what ResMed might be worth based on its future cash generation. For ResMed, the latest twelve month Free Cash Flow sits at about $1.75b, and the model assumes growing cash flows rather than a shrinking business, using a two stage Free Cash Flow to Equity approach.

On these assumptions, the DCF model points to an intrinsic value of about $275 per share. Compared with the current share price, that implies the stock is trading at roughly a 29.2% discount, so ResMed appears undervalued on cash flow grounds. The recent downgrade tied to competition and weight loss drug concerns helps explain why the market is pricing in a wide margin of safety despite these projected cash flows.

On this Discounted Cash Flow view, ResMed stock currently appears undervalued relative to the cash the business is expected to generate.

Our Discounted Cash Flow (DCF) analysis suggests ResMed is undervalued by 29.2%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Is ResMed Still Cheap on Earnings?

The P/E ratio is a useful cross check for ResMed because it ties the share price directly to the earnings investors are paying for today. ResMed currently trades on a P/E of about 18.5x, compared with a Medical Equipment industry average around 25.6x and a peer group average near 26.8x, so the stock is priced below both broad benchmarks.

On Simply Wall St's fair multiple framework, a P/E of roughly 23.2x would be in line with what might be expected for ResMed given its sector, profitability profile and risk factors. Against that yardstick, the current 18.5x implies a meaningful discount. This suggests the recent reset in expectations has pushed the earnings multiple below what the model indicates as a reasonable level.

On the P/E test, ResMed stock appears undervalued relative to both its industry and the fair multiple implied by its fundamentals.

The ResMed Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the valuation work on ResMed leaves off, explaining which combinations of future growth, margins and earnings would need to occur for the stock to be worth materially more or less than today’s price on the Community page. Each narrative links its figures to a clear view of how ResMed's growth, profitability and key risks might evolve, giving you a reference point you can revisit as new information emerges.

Community views on ResMed sit far apart, with one camp focused on long run sleep health demand and another fixated on GLP 1 and margin risks.

Bull case: 25% undervalued

"Acceleration in adoption of home-based, cloud-connected therapy solutions and digital health platforms (including software like Brightree and AirView) enhances recurring high-margin revenue streams and increases both user retention and net profit margins over time…"

Bear case: 7% overvalued

"GLP-1 therapies are being framed internally as a once-in-a-generation demand opportunity. However, if broader weight loss adoption or new clinical data leads to fewer patients requiring CPAP, growth in device and mask revenue could fall short of current expectations and pressure earnings…"

Do you think there's more to the story for ResMed? Head over to our Community to see what others are saying!

The Bottom Line

ResMed screens as undervalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and current earnings multiples, and the broader valuation checks are aligned with that message. For you as an investor, the key question is whether the discount reflects an overly cautious reaction to GLP 1 and competitive risks or a fair warning that future cash flows could be less robust than the models assume. The crux of the bull versus bear debate is whether ResMed can sustain attractive recurring cash generation from its sleep apnea and software ecosystem in the face of changing treatment patterns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.