Revolution Medicines (RVMD) Stock Could Be 24% Overvalued After RASolute 302 Trial Data

Revolution Medicines RVMD | 0.00 |

R&D leadership changes put Revolution Medicines stock in focus

Revolution Medicines (RVMD) is back on investors’ radar after new RASolute 302 trial data, with the stock also reacting to a planned reshaping of the company’s research and development leadership team.

Over the past year, Revolution Medicines has moved from a niche oncology story to a stock attracting much broader attention, with a 90 day share price return of 73.59% and a 1 year total shareholder return of 314.11%, helped by positive RASolute 302 data and renewed focus on its R&D leadership transition.

If this kind of momentum in oncology has caught your eye, it may be worth widening your search to other potential opportunities in healthcare related technology using the 38 healthcare AI stocks

With Revolution Medicines now trading at $165.81 after very strong 1 year and multi year returns, the key question is whether the current price still reflects a discount to its prospects or if markets are already pricing in future growth.

Most Popular Narrative: 24% Overvalued

Compared with the most followed fair value estimate of $133.70, Revolution Medicines at $165.81 is priced well above that narrative anchor. This view hinges on ambitious growth and margin assumptions.

The move toward targeted oncology treatments for high unmet need tumors such as pancreatic, lung and colorectal cancer aligns with the company’s RAS(ON) portfolio, which could influence long term revenue growth if multiple registrational programs convert to approved therapies. Eight ongoing or planned Phase III registrational trials and clinical experience in more than 2,500 patients create multiple data points over the next few years that could change how investors view the durability and scale of the pipeline, with potential implications for future revenue visibility and earnings power.

Curious what kind of revenue ramp, margin shift and earnings multiple are baked into that $133.70 figure? The narrative leans on aggressive growth, rising profitability and a premium valuation that would place Revolution Medicines in rare company. The full story joins these moving parts into a single long term roadmap.

Result: Fair Value of $133.70 (OVERVALUED)

However, the Revolution Medicines story could shift quickly if RAS focused trials disappoint, or if heavy 2026 operating expenses of US$1.6b to US$1.7b pressure the balance sheet.

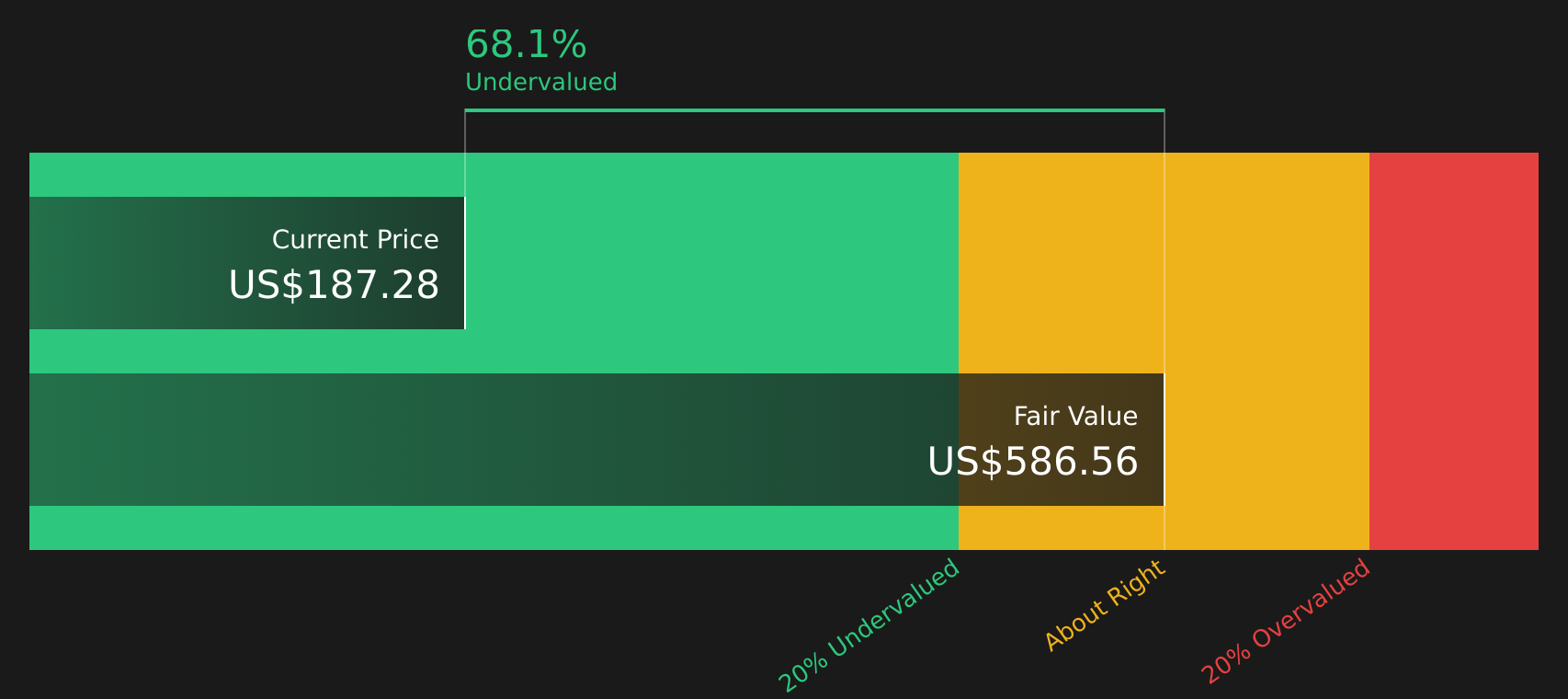

Another View: SWS DCF Signals Deep Discount

While the most popular Revolution Medicines narrative points to a $133.70 fair value and a stock that looks 24% overvalued, the SWS DCF model paints a very different picture. Its future cash flow value of $594.77 suggests the shares trade at a steep discount. When two methods diverge this sharply, which one do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Revolution Medicines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After weighing both the bullish and cautious narratives around Revolution Medicines, it makes sense to move quickly, review the underlying data and test each claim against your own expectations, then balance the upside and downside using the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Revolution Medicines?

If Revolution Medicines has sharpened your focus, do not stop at a single stock. Exploring a broader range of ideas can help you compare risks, potential returns and portfolio fit more clearly.

Use the Simply Wall Street Screener to identify fresh opportunities across different investment styles before they move too far from your buy zone.

- Target potential mispricing by scanning for high quality stocks that appear attractively valued using the 44 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies with higher yield potential through the 7 dividend fortresses.

- Prioritise resilience by concentrating on businesses with stronger financial footing using the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.