Robert Half (RHI) Stock After Recent Rebound And Sector Reassessment

Robert Half Inc. RHI | 0.00 |

- If you are wondering whether Robert Half stock offers value at today's price, this article breaks down what the current share price might be implying about the business.

- The stock recently closed at US$32.76, with gains of 3.7% over the past week and 20.8% over the past month, while longer term returns include a 19.8% gain year to date but declines of 13.7% over 1 year, 49.4% over 3 years and 55.3% over 5 years.

- Recent news around Robert Half has largely focused on its position within the professional services sector and how investors are reassessing staffing and consulting companies in light of changing client demand and hiring trends. This context helps explain why shorter term price moves can look very different to the multi year performance.

- Robert Half currently has a valuation score of 3/6, which means it screens as undervalued on half of the checks used. The next sections will walk through these traditional valuation approaches before finishing with a broader way to think about what the stock could be worth.

Approach 1: Robert Half Discounted Cash Flow (DCF) Analysis

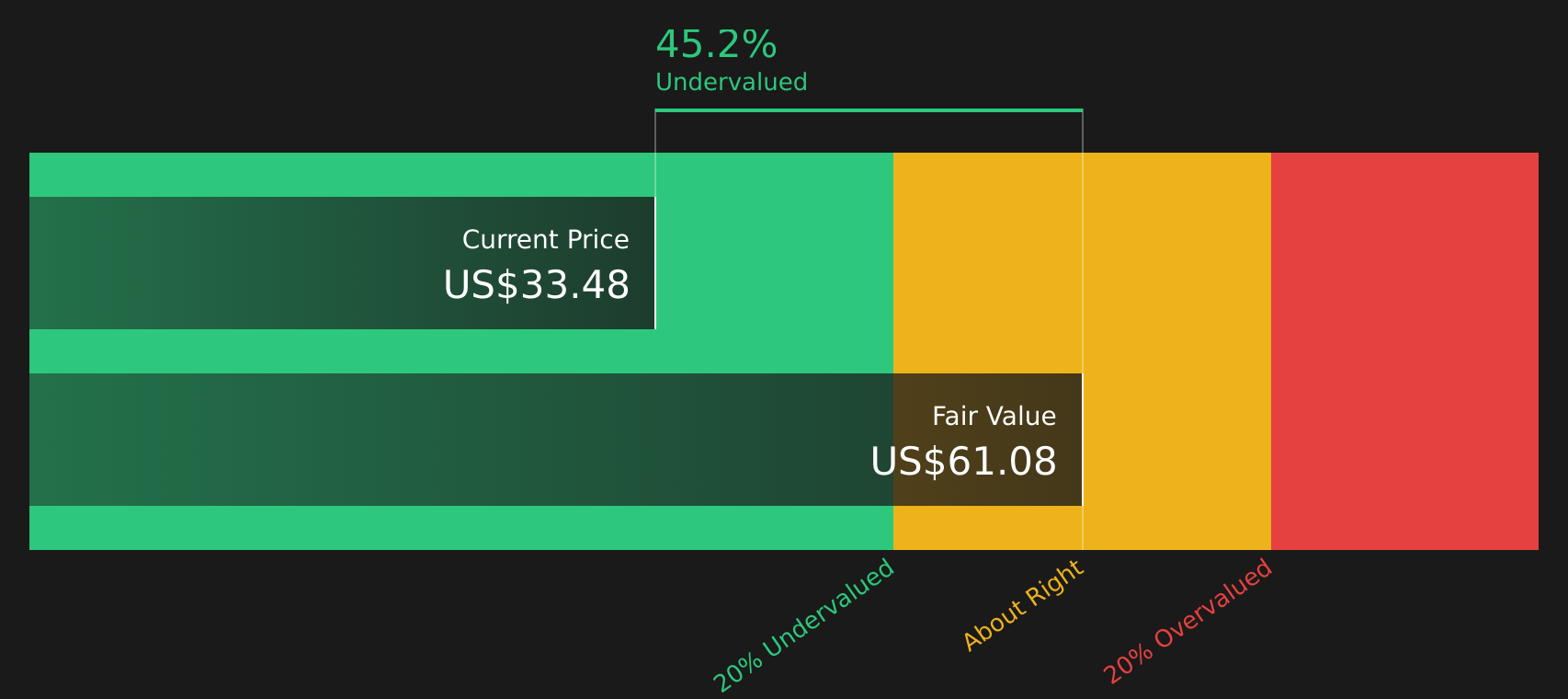

A Discounted Cash Flow model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today’s value, so you can compare that estimate to the current share price. For Robert Half, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections.

Robert Half’s latest twelve month free cash flow is about $219 million, and analysts plus extrapolated estimates point to annual free cash flows in the mid $200 million range over the coming decade, with a projected figure of $318.46 million by 2035. Simply Wall St discounts these future cash flows back to today using its own assumptions, which results in an estimated intrinsic value of $60.21 per share.

Compared with the recent share price of $32.76, this DCF outcome suggests the stock trades at roughly a 45.6% discount to that intrinsic value. On this model, Robert Half stock screens as undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Robert Half is undervalued by 45.6%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Approach 2: Robert Half Price vs Earnings

For profitable companies like Robert Half, the P/E ratio is a common way to think about value because it links what you pay for the stock to the earnings the company is generating today. In general, higher expected growth and lower perceived risk can support a higher P/E, while slower expected growth or higher risk usually points to a lower, more cautious P/E.

Robert Half currently trades on a P/E of 25.45x. That sits above the Professional Services industry average P/E of 18.34x and also above the peer group average of 15.60x. Simply Wall St also calculates a “Fair Ratio” for Robert Half of 27.26x. This is the P/E level that might be reasonable given factors such as its earnings profile, industry, profit margins, market cap and identified risks.

This Fair Ratio is more tailored than a simple peer or industry comparison because it adjusts for company specific characteristics rather than assuming every stock should trade at the same multiple. Comparing the Fair Ratio of 27.26x with the current P/E of 25.45x, Robert Half screens as slightly cheaper than this customised benchmark, which points to the stock being undervalued on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Robert Half Narrative

Earlier it was mentioned that there is an even better way to think about valuation, and on Simply Wall St that comes through Narratives, where you link your view of Robert Half’s business story to a set of revenue, earnings and margin assumptions, which then roll into a fair value that you can compare with today’s price.

In practice, a Narrative is your own storyline for the company, captured as numbers. Instead of only accepting a single model you can see, for example, one investor on the Community page using the lower fair value of US$20.00 and another using a higher fair value of about US$47.99, each backed by different assumptions about how automation, AI and consulting demand affect Robert Half over time.

Because these Narratives sit on Simply Wall St’s platform, used by millions of investors, they are easy to explore, update automatically when fresh news or earnings guidance arrives, and help you decide whether the stock looks expensive or inexpensive by comparing each Narrative’s fair value to the live market price rather than relying on a single static estimate.

For Robert Half, here are previews of two leading Robert Half Narratives:

Fair value: US$47.99 per share

Implied discount to this fair value: about 31.7% compared with the recent price of US$32.76

Revenue growth assumption: 4.5% a year

- Views Robert Half as benefiting over time from AI enabled productivity, cost discipline and operating leverage tied to restructuring and technology investment.

- Assumes a shift toward higher bill rates, specialization and more project based and contingent staffing, which support margins and earnings in the talent solutions and consulting operations.

- Highlights risks from automation, digital marketplaces and slower permanent placement demand, which could pressure revenue and profitability if the business transformation lags competitors.

Fair value: US$32.39 per share

Implied premium to this fair value: about 1.1% compared with the recent price of US$32.76

Revenue growth assumption: 3.2% a year

- Frames Robert Half around a more modest recovery path using analyst consensus assumptions that factor in slower revenue growth and more conservative profit margins.

- Points to ongoing pressure from softer hiring demand, higher SG&A as a share of revenue and margin compression, along with exposure to legacy staffing lines that face automation risk.

- Emphasizes that cost actions and AI recruitment spending may help efficiency, but that execution risk, digital competition and uneven consulting demand could limit upside if conditions remain challenging.

If you want to see how these Robert Half narratives compare with the full community range, including different fair values, growth paths and risk views, head to the narrative hub where you can review assumptions side by side and decide which story best fits your own research on the stock.

Do you think there's more to the story for Robert Half? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.