Royal Caribbean Group (RCL) Valuation Check After Fortune Admired List Recognition And New Miami Terminal Project

Royal Caribbean Group RCL | 273.59 | -3.00% |

Royal Caribbean Cruises (RCL) is back in focus after its inclusion in the Fortune World’s Most Admired Companies 2026 list, along with fresh projects such as a new LEED-focused Cruise Terminal G at PortMiami.

These recognitions and projects come after a period where Royal Caribbean Cruises’ 1 year total shareholder return of 19.13% contrasts with a weaker recent patch, including a 30 day share price return of 7.63% decline and a 90 day share price return of 12.34% decline. This suggests longer term momentum alongside some cooling in shorter term sentiment.

If this kind of travel and leisure story has your attention, it could be a good moment to see what else is setting course in aerospace and defense stocks as you compare opportunities.

With Royal Caribbean shares delivering a 19.13% 1 year total return but seeing a 7.63% and 12.34% decline over the past 30 and 90 days, investors may be asking whether this recent pullback represents a potential entry point or whether the market is already pricing in future growth.

Price-to-Earnings of 18.6x: Is it justified?

Royal Caribbean’s last close of $277.77 sits against a P/E of 18.6x, which screens as cheaper than peers and some fair value indicators that are available.

The P/E ratio compares the current share price with the company’s earnings per share, so you are effectively seeing how much investors are paying for every dollar of earnings.

For Royal Caribbean, the statements indicate that a P/E of 18.6x is described as good value compared with its peer average of 29.6x and the wider US Hospitality industry average of 21.4x. It is also flagged as attractive against an estimated fair P/E of 28.6x, a level the market could move towards if sentiment and earnings expectations stay aligned with that fair ratio framework.

Result: Price-to-Earnings of 18.6x (UNDERVALUED)

However, you still need to weigh risks such as sensitivity to travel demand, higher financing costs on its fleet, and any setback to earnings expectations that underpin the current P/E.

Another View: Cash Flows Tell an Even Cheaper Story

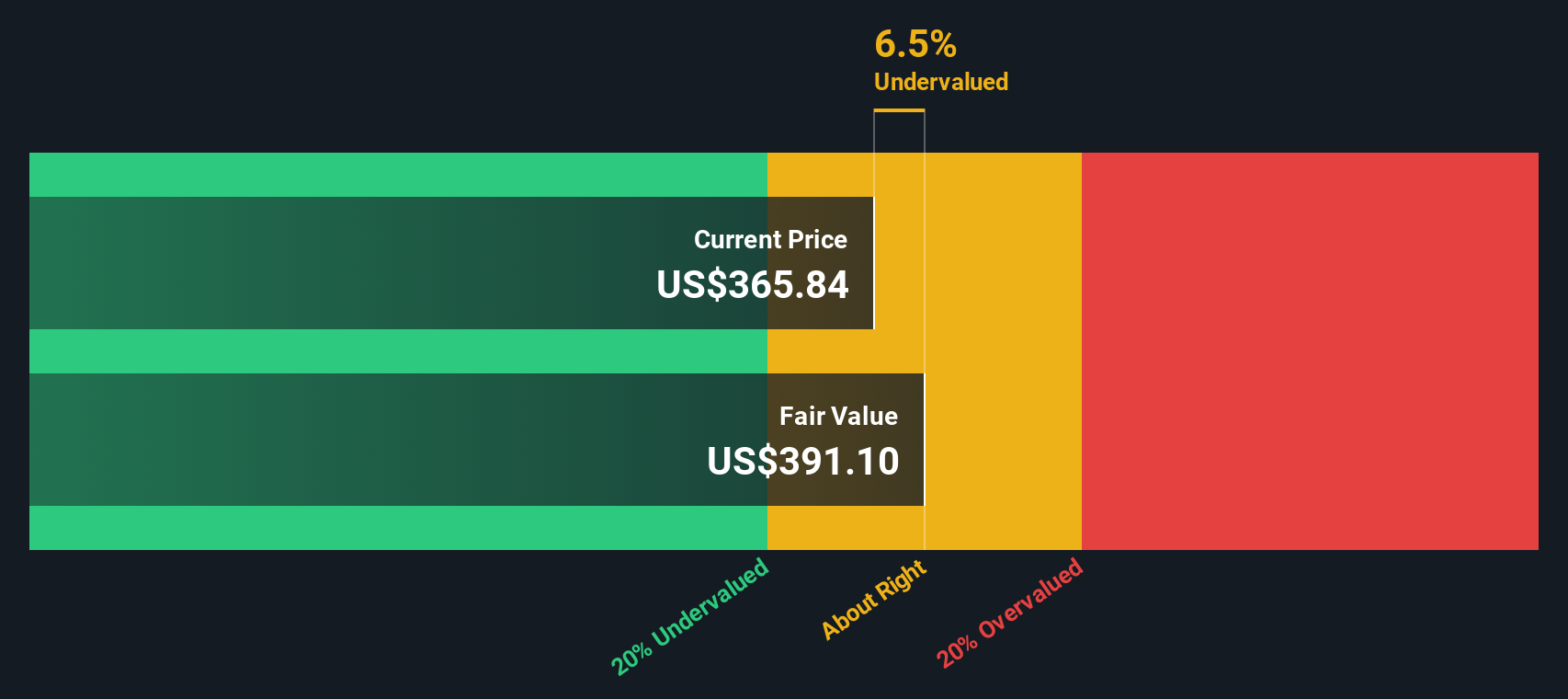

While the 18.6x P/E points to good value against peers, our DCF model goes further and suggests Royal Caribbean Cruises, at $277.77, is trading at a 51.4% discount to an estimated future cash flow value of $571.61. If both are right, is the market still catching up?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Royal Caribbean Cruises for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Royal Caribbean Cruises Narrative

If you look at the numbers and come to a different conclusion or simply prefer to test your own view, you can build a complete narrative in just a few minutes with Do it your way.

A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop with one company. Use the Simply Wall St screener to spot opportunities others might miss.

- Target potential bargains by scanning these 877 undervalued stocks based on cash flows that currently trade below what their cash flows might suggest.

- Ride powerful tech trends by checking out these 23 AI penny stocks pushing the boundaries of artificial intelligence adoption.

- Boost your income focus by reviewing these 13 dividend stocks with yields > 3% offering yields above 3% with clearer cash return potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.