SB Financial Group (SBFG): Profit Margin Declines to 19.5% Challenges Bull Case on Value and Stability

SB Financial Group Inc SBFG | 21.00 | -1.04% |

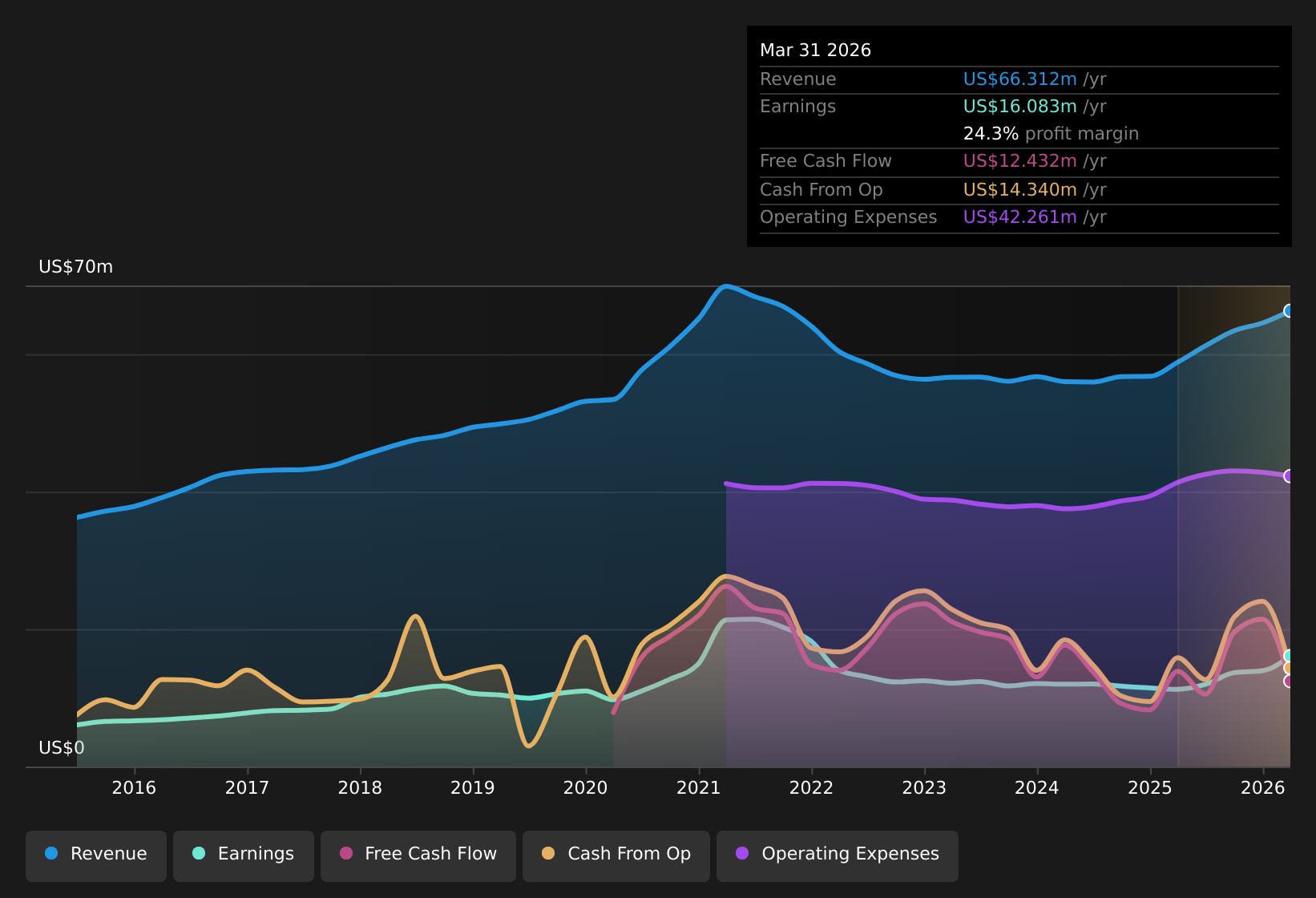

SB Financial Group (SBFG) posted a net profit margin of 19.5%, down from last year’s 21.5%, while earnings have fallen an average of 11.2% per year over the past five years. Most recently, the company experienced another year of negative earnings growth, making further year-to-year acceleration comparisons less meaningful. With high-quality earnings but profit and margin pressures still in play, investors are left weighing value and dividends against a lack of growth in the foreseeable future.

See our full analysis for SB Financial Group.Next, we will see how these latest results compare when set against the wider market narratives and community perspectives. There may be surprises where the numbers and stories do not fully align.

Profit Margins Expected to Rebound Sharply

- While profit margins have slipped to 19.5% from 21.5% last year, analysts forecast an impressive climb to 46.1% over the next three years despite projected annual revenue declines of 14.6%.

- Analysts' consensus view highlights a striking tension between falling sales and expected margin expansion:

- This optimism is pinned on management's strategic push in digital banking and cost controls. If successful, these initiatives could nearly double margins even as top-line challenges persist.

- However, the gap between declining revenues and soaring margin forecasts signals real execution risk. Critics will question if efficiency improvements can fully offset competitive and expense pressures in a tough lending climate.

- See whether the full Consensus Narrative sheds new light on how management aims to hit these ambitious margin targets and why analysts remain cautiously constructive about the outlook. 📊 Read the full SB Financial Group Consensus Narrative.

Valuation Appears Undemanding Versus Peers

- At a price-to-earnings ratio of 10.3x, SB Financial Group trades cheaper than both the US Banks industry average (11.2x) and its closest peer group (15.6x), and well below its DCF fair value of $29.21, with shares currently at $19.56.

- Consensus narrative notes the stock's discounted valuation could present an opening for long-term investors:

- The current share price sits at a 33% discount to DCF fair value, and only 5.9% below the analyst price target of $23.00. This suggests analysts see minimal downside but limited short-term upside as well.

- Bulls may argue that the attractive dividend plus room for rerating could reward patient holders. Others will point out that low valuation alone may not be enough without clear growth catalysts.

Regional Focus a Double-Edged Sword

- SB Financial Group’s growth is mostly anchored in Midwest and rural markets, with regional loan growth up 8.9% and deposit growth up 12% according to consensus narrative. However, its footprint leaves the company exposed to local downturns and rising competition.

- Consensus narrative emphasizes both sides of the coin for SB Financial’s business model:

- On the upside, successful expansions in places like Indianapolis and Cincinnati, plus resilience in home lending and new fee income streams, suggest the company can carve out a niche against larger rivals.

- The lack of broader diversification and higher expenses from digital investments mean even modest local disruptions or competitive flare-ups could quickly squeeze profits and test the company’s efficiency targets.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for SB Financial Group on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you have a unique take on the results? Take a moment to craft your own narrative and share a fresh angle. Do it your way

A great starting point for your SB Financial Group research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Despite high-quality earnings, SB Financial Group faces declining revenues, pressured margins, and a lack of consistent growth. These factors put its future performance at risk.

For investors seeking companies with a track record of steady revenue and profit growth, consider focusing on stable growth stocks screener (2103 results) to spot opportunities delivering more reliable results across changing markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.