Should BAC’s New Long-Dated Bonds And Preferred Dividends Strategy Require Action From Bank of America (BAC) Investors?

Bank of America Corp BAC | 0.00 |

- In recent weeks, Bank of America has launched multiple senior unsecured bond offerings across maturities out to 2066, while its board authorized regular dividends on several preferred stock series with payments scheduled through late July and early August 2026.

- These capital markets moves, alongside regulatory shifts such as the Federal Reserve’s proposal to ease Basel III capital requirements and a hawkish stance on interest rates, highlight how Bank of America is actively shaping its funding mix and capital position amid a changing policy backdrop.

- We’ll now examine how looser Basel III requirements and a more hawkish Federal Reserve stance could influence Bank of America’s existing investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

Bank of America Investment Narrative Recap

To own Bank of America, you need to be comfortable with a large, diversified bank whose earnings are tightly linked to credit quality, interest rates, and regulation. The near term story still hinges on how a more hawkish Federal Reserve and easing Basel III rules flow through to net interest income and capital flexibility, while the biggest current risk sits in litigation and regulatory scrutiny, which these latest bond and preferred dividend moves do not materially change.

Among the recent announcements, the Federal Reserve’s proposal to soften Basel III capital requirements looks most relevant, as it could affect how investors think about Bank of America’s ability to support lending, sustain buybacks, and absorb credit or legal shocks if volatility in funding and credit spreads resurfaces.

Yet investors should be aware that ongoing scrutiny of Bank of America’s debanking practices and potential litigation costs could still...

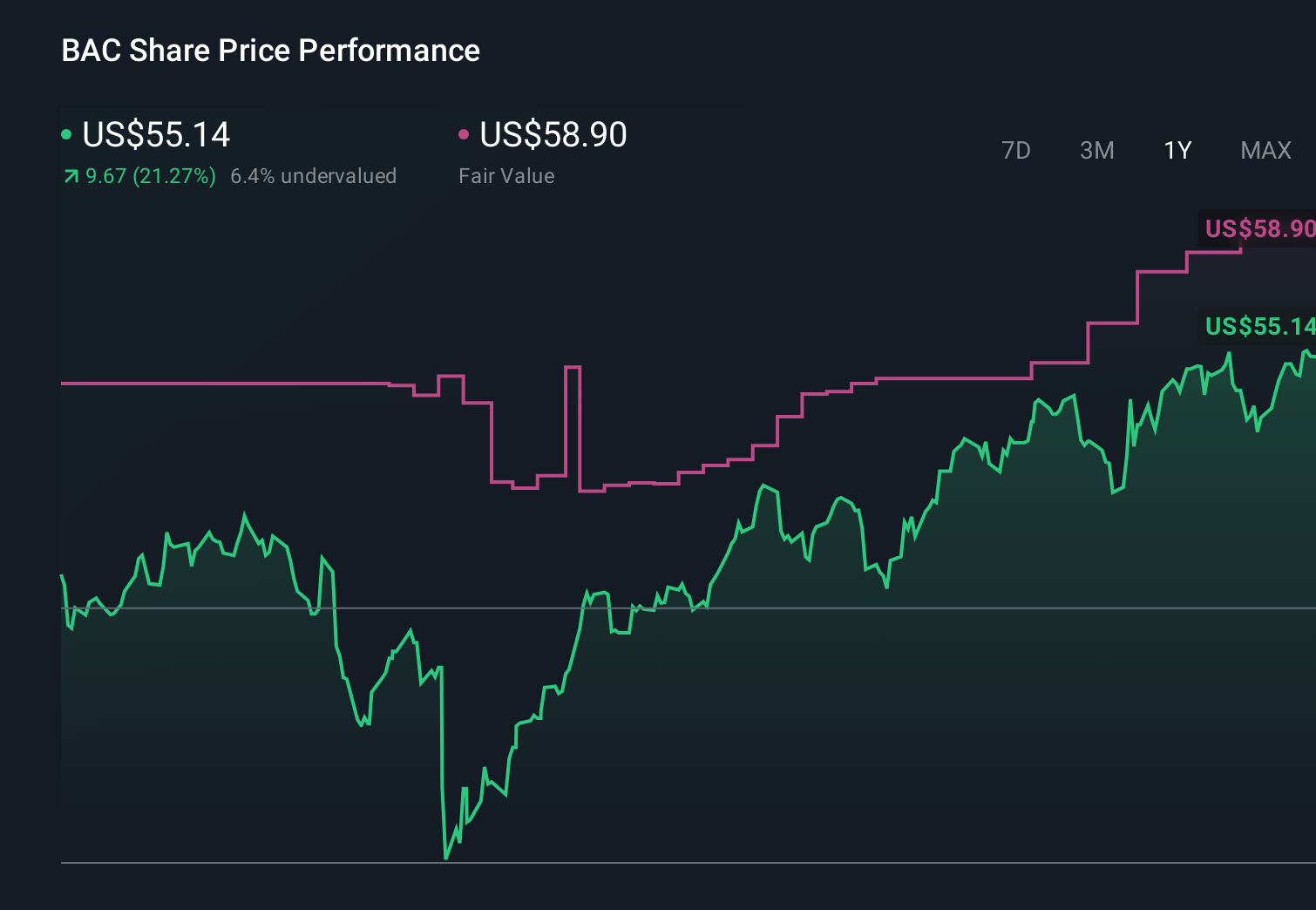

Bank of America's narrative projects $133.8 billion revenue and $36.7 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $6.4 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $63.16 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently estimate Bank of America’s fair value between US$63.16 and US$69.57, highlighting how far opinions on upside can stretch. You should weigh that diversity against the key risk that market volatility and credit quality shifts could pressure margins and earnings, and explore how different investors factor those scenarios into their views.

Explore 4 other fair value estimates on Bank of America - why the stock might be worth as much as 24% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.