Should CubeSmart’s (CUBE) Expanded US$1 Billion Revolver Shape Investors’ View of Its Risk Profile?

CubeSmart CUBE | 0.00 |

- On June 24, 2026, CubeSmart and CubeSmart, L.P. entered into a Third Amended and Restated Credit Agreement, expanding their unsecured revolving credit facility from US$850,000,000 to US$1.00 billion and extending its maturity to June 24, 2030, with pricing tied to SOFR, unsecured debt ratings, and leverage levels.

- This larger, longer-dated revolver, priced at 0.775% over SOFR plus a 0.15% facility fee at current metrics and containing customary covenants, increases CubeSmart’s financial flexibility by refinancing the prior facility and potentially supporting acquisition capacity and balance sheet resilience.

- We’ll now look at how this expanded US$1.00 billion revolver and extended maturity may influence CubeSmart’s investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

CubeSmart Investment Narrative Recap

To own CubeSmart, you need to believe its dense, supply constrained urban markets and steady storage demand can offset current pressure on same store revenue and earnings. The new US$1.00 billion unsecured revolver slightly strengthens the near term balance sheet story, but does not materially change the key catalyst of revenue stabilization or the main risk around persistent weakness in Sunbelt occupancy and pricing.

The recent dividend affirmation at US$0.53 per share is the clearest reference point alongside the upsized revolver, as together they outline how CubeSmart is balancing shareholder cash returns with balance sheet flexibility while it works through modest same store growth guidance and softer net income trends.

Yet while balance sheet flexibility has improved, investors should be aware that sustained new supply in key Sunbelt markets could still...

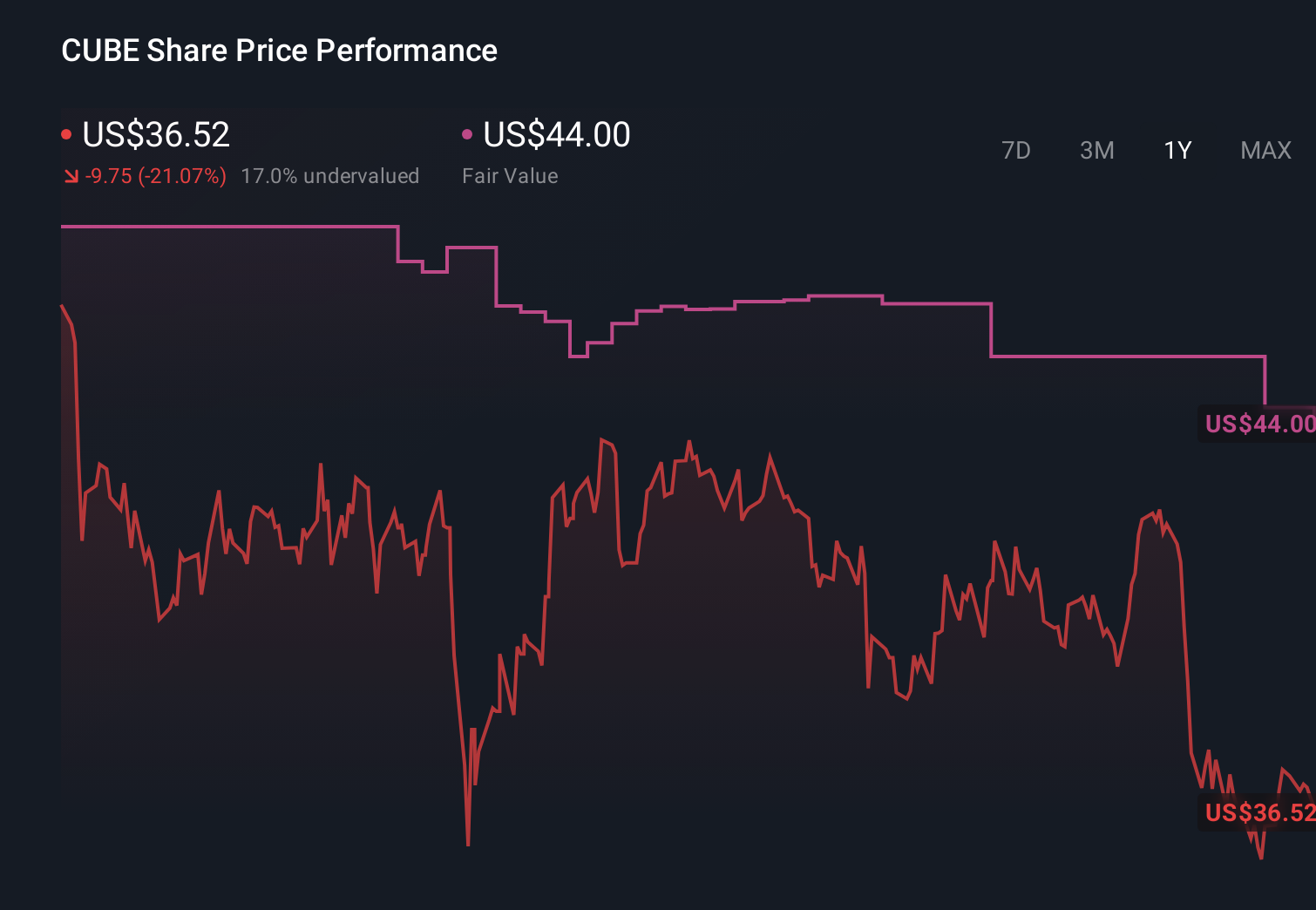

CubeSmart's narrative projects $1.2 billion revenue and $342.0 million earnings by 2029. This requires 3.0% yearly revenue growth and about a $14.5 million earnings increase from $327.5 million.

Uncover how CubeSmart's forecasts yield a $43.13 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$40 to about US$52.79 per share, underscoring how far apart individual views can be. Against this, the expanded US$1.00 billion revolver brings extra funding capacity, but ongoing Sunbelt supply and occupancy headwinds may still weigh on CubeSmart’s operating performance, so it is worth exploring several contrasting viewpoints before deciding where you stand.

Explore 4 other fair value estimates on CubeSmart - why the stock might be worth as much as 28% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CubeSmart research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CubeSmart research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CubeSmart's overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.