Should Dividend Hike And Submarine-Focused Upgrade Reshape Capital Allocation Priorities For General Dynamics (GD) Investors?

General Dynamics Corporation GD | 0.00 |

- Recently, General Dynamics’ board declared a regular quarterly dividend of US$1.59 per share, payable on August 7, 2026, to shareholders of record on July 2, 2026, while the company also reported double-digit growth in revenue and operating earnings across all major segments.

- At the same time, a Jefferies rating upgrade highlighting accelerating U.S. submarine demand and a multi-billion-dollar Columbia-class contract have sharpened investor attention on the Marine Systems division as a key contributor within General Dynamics’ diversified defense and aerospace portfolio.

- We’ll now examine how the Jefferies upgrade, centered on accelerating submarine demand, may reshape General Dynamics’ investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

General Dynamics Investment Narrative Recap

To own General Dynamics, you need to be comfortable with a long pipeline of defense and aerospace work, underpinned by large submarine and jet programs, and the operational complexity that comes with them. The latest dividend affirmation and Jefferies’ focus on Marine Systems do not materially change the near term picture, where supply chain execution in shipyards and broader margin resilience still look like the key catalyst and the biggest operational risk.

Among the recent announcements, the multi billion dollar Columbia class submarine contract stands out as most relevant, because it directly underpins the Marine Systems growth story that Jefferies has highlighted. It reinforces the backlog and revenue visibility supporting the current investment narrative, but it also raises the stakes on execution, as any persistent shipyard or supplier bottlenecks could quickly turn this growth engine into a source of pressure on costs and margins.

Yet even with strong order momentum, investors should be aware that persistent supply chain and shipyard disruptions could still...

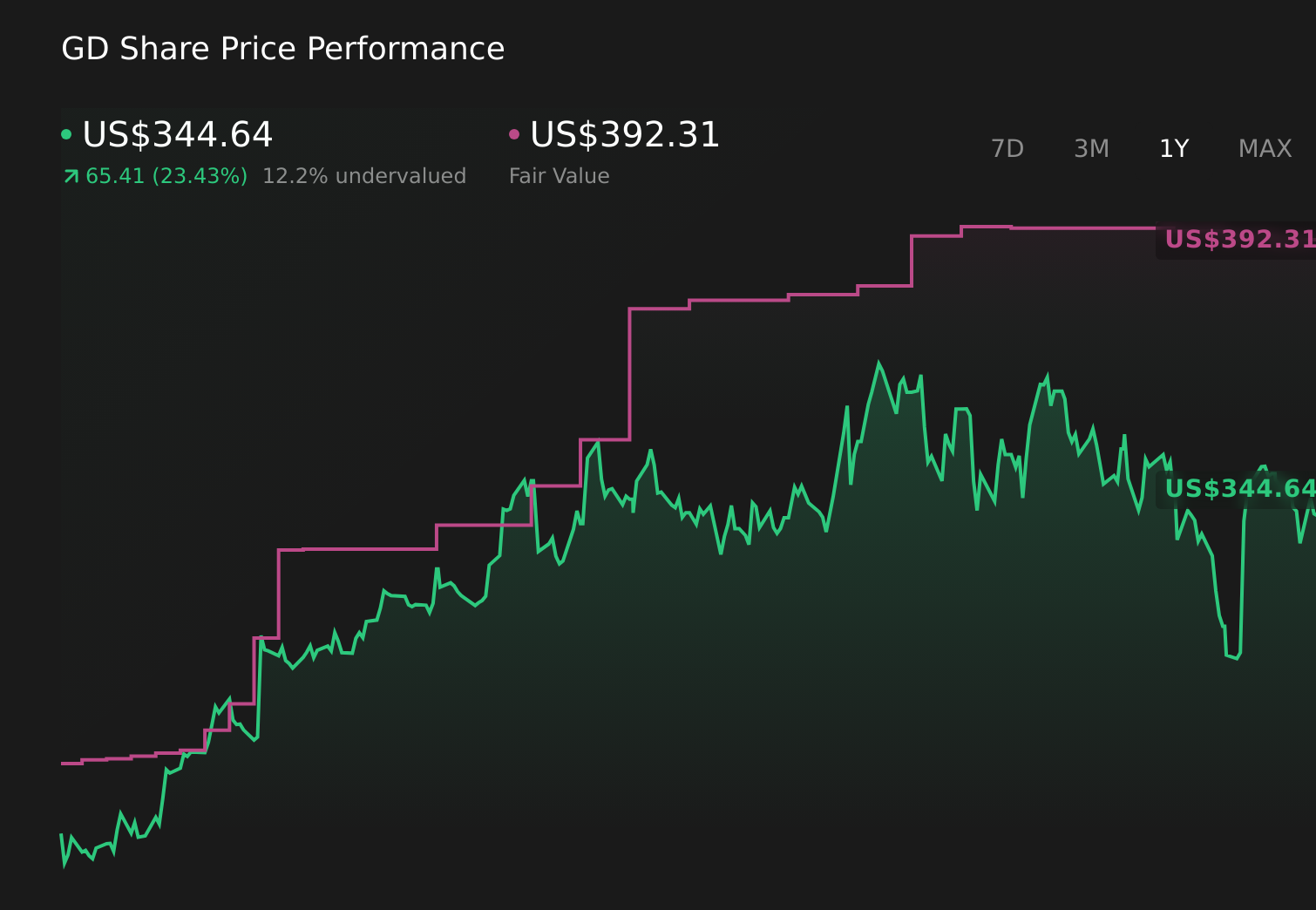

General Dynamics' narrative projects $60.7 billion revenue and $5.4 billion earnings by 2029. This requires 4.1% yearly revenue growth and about a $1.1 billion earnings increase from $4.3 billion.

Uncover how General Dynamics' forecasts yield a $392.22 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently value General Dynamics between US$392.22 and US$409.18 per share, underscoring how far views can differ. You should weigh those opinions against the concentration of future growth on Marine Systems, where any setbacks in submarine production could have wider implications for the company’s performance.

Explore 4 other fair value estimates on General Dynamics - why the stock might be worth as much as 14% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Dynamics research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free General Dynamics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Dynamics' overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.