Should Millicom’s Newly Approved US$3 Dividend Schedule Reshape TIGO’s Income Profile and Risk-Reward Outlook?

Millicom International Cellular SA TIGO | 0.00 |

- Millicom International Cellular S.A. reported that its Annual General Meeting on May 20, 2026 approved a total dividend of US$3.00 per share, to be paid in four equal instalments on or around July 15 and October 15, 2026, and January 15 and April 15, 2027.

- This multi-step dividend schedule highlights management’s emphasis on steady cash returns over time, offering investors clearer visibility on upcoming income payments.

- We’ll now examine how this newly approved, phased US$3.00 per-share dividend distribution could influence Millicom’s investment narrative and risk-reward profile.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

Millicom International Cellular Investment Narrative Recap

To own Millicom, you need to believe in its ability to convert Latin American data growth and postpaid migration into resilient cash generation while managing heavy capex and FX volatility. The newly approved US$3.00 per share dividend, spread over four payments, reinforces the near term income story but does not materially change the key catalyst of execution on growth investments, nor the main risk of balance sheet pressure from capex and refinancing needs.

The AGM’s dividend approval comes shortly after Millicom upsized its 7.375% senior notes by US$87.5 million in April 2026, earmarked for general corporate purposes including capex and M&A. That funding decision, alongside the phased dividend, underlines the tension between rewarding shareholders today and funding ongoing network expansion, which sits at the heart of both the upside catalyst in data growth and the downside risk around sustained high investment requirements.

Yet investors should also be aware that rising competition and heavy 4G and 5G capex could still...

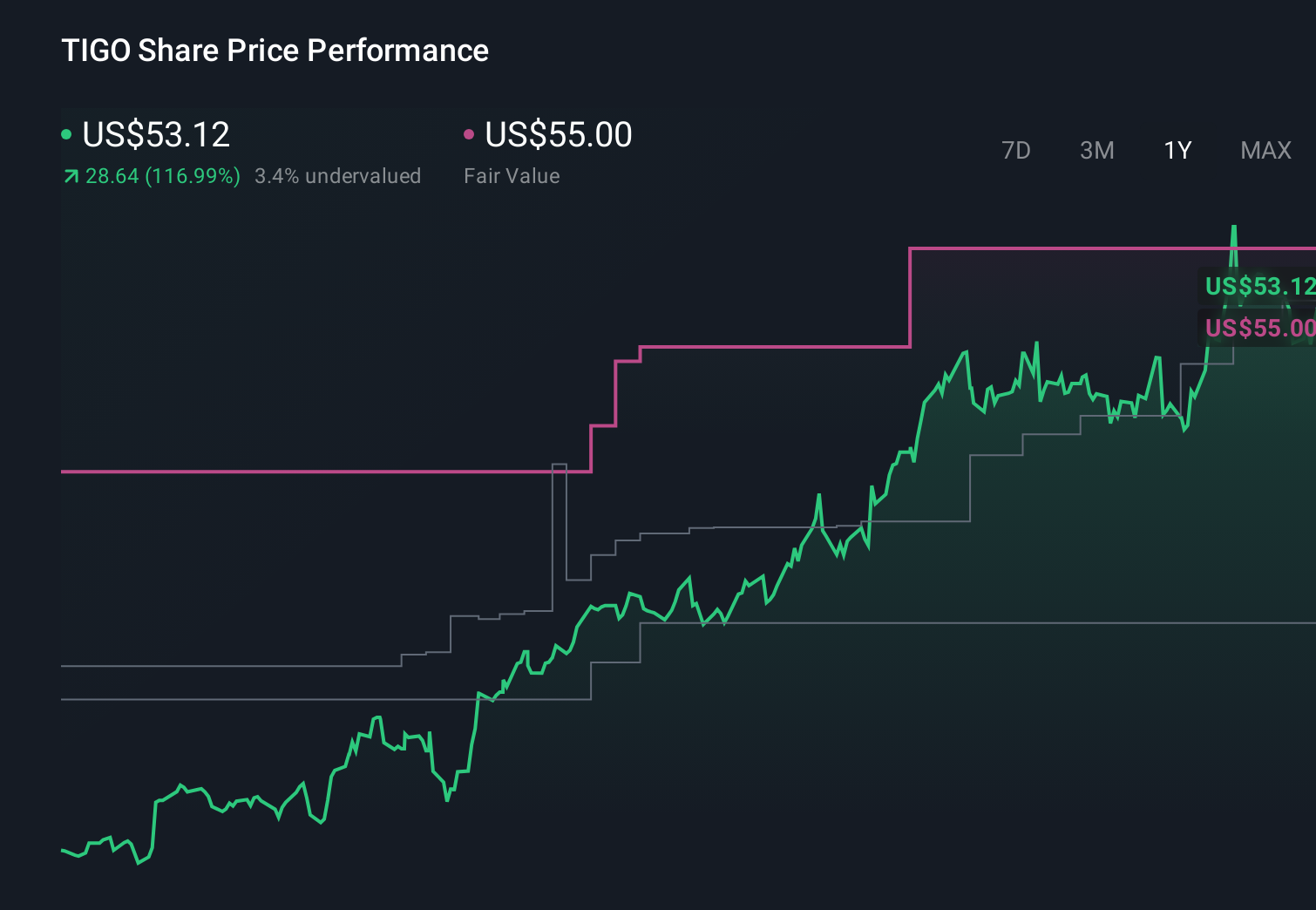

Millicom International Cellular's narrative projects $5.9 billion revenue and $628.3 million earnings by 2028. This assumes 1.7% yearly revenue growth and an earnings decrease of $326.7 million from $955.0 million today.

Uncover how Millicom International Cellular's forecasts yield a $52.35 fair value, a 39% downside to its current price.

Exploring Other Perspectives

While consensus focuses on steady cash returns, the most optimistic analysts saw earnings reaching about US$1.4 billion and revenue near US$9.2 billion, which is a far more bullish view that could shift again as this dividend decision and ongoing capital needs reshape how you weigh upside against the risk of sustained high network investment.

Explore 7 other fair value estimates on Millicom International Cellular - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Millicom International Cellular research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Millicom International Cellular research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Millicom International Cellular's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.