Should Record Volumes and Higher Payouts at Enterprise Products Partners (EPD) Require Action From Investors?

Enterprise Products Partners L.P. EPD | 0.00 |

- Enterprise Products Partners recently presented at the 23rd Annual Energy Infrastructure CEO & Investor Conference in Aventura, Florida, highlighting record operational volumes, higher adjusted EBITDA, and a 2.8% increase in its quarterly cash distribution.

- The partnership emphasized how new assets such as the Bahia NGL pipeline, Permian gas processing plants, and growing export dock throughput are reinforcing its toll-like cash flow model and long distribution growth track record.

- Now we’ll explore how record operational volumes and expanding export infrastructure shape Enterprise Products Partners’ existing investment narrative and risk-reward balance.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to believe in the durability of its toll-like midstream model, supported by record volumes and expanding export capacity. The latest conference update reinforces that story and modestly strengthens the near term catalyst of higher utilization, while leaving key risks like leverage, tariff exposure and Permian producer activity essentially unchanged.

The most relevant update here is Enterprise’s 2.8% increase in its quarterly cash distribution to US$0.55 per unit, backed by higher adjusted EBITDA and record throughput. That decision sits alongside new assets such as the Bahia NGL pipeline and Permian gas processing plants, which feed into the same volume driven catalyst that investors are watching most closely.

Yet behind the steady distributions, investors should be aware of how Enterprise’s sizeable debt load could interact with shifting credit conditions and interest rates...

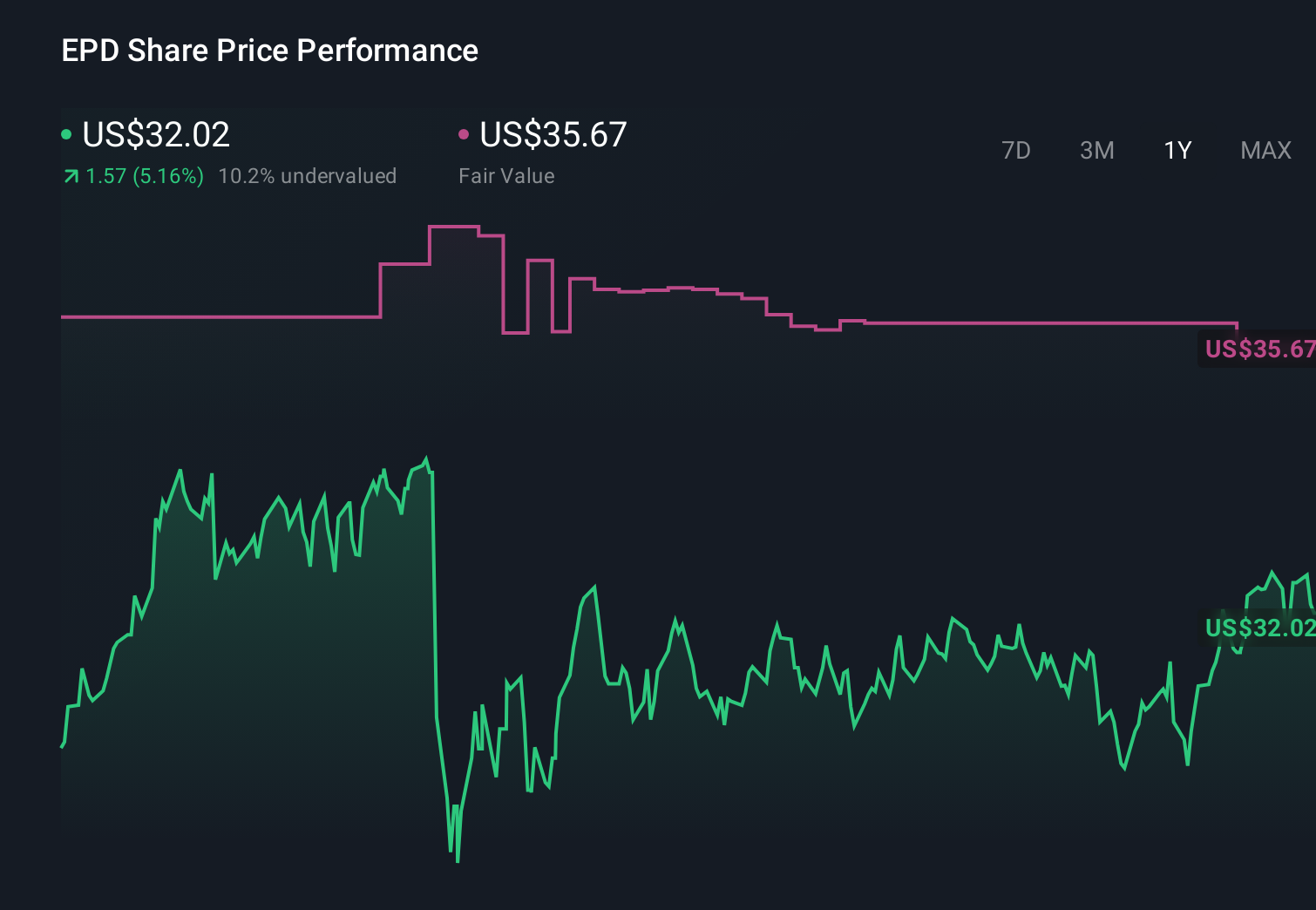

Enterprise Products Partners' narrative projects $60.5 billion revenue and $7.4 billion earnings by 2029. This requires 5.5% yearly revenue growth and about a $1.6 billion earnings increase from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $40.85 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Six Simply Wall St Community fair value estimates span roughly US$34 to US$92 per unit, showing how far apart individual views can be. As you weigh those opinions against Enterprise’s growing export and processing footprint, it is worth considering how volume driven catalysts might interact with tariff and Permian activity risks over time.

Explore 6 other fair value estimates on Enterprise Products Partners - why the stock might be worth 13% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.