Should Renewed Analyst Focus On Regional Bank Profit Resilience Require Action From Huntington Bancshares (HBAN) Investors?

Huntington Bancshares Incorporated HBAN | 15.79 | -0.57% |

- In recent days, Huntington Bancshares has been in focus as analysts reassessed U.S. regional banks, highlighting expectations for resilient profits ahead of upcoming earnings.

- This wave of analyst attention, combined with a more constructive view on regional bank fundamentals, has reinforced Huntington’s positioning within the sector.

- Now we’ll explore how this renewed analyst confidence in regional banks, especially around profit resilience, could influence Huntington’s investment narrative.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Huntington Bancshares Investment Narrative Recap

To own Huntington Bancshares, you need to believe in the resilience of a regional bank model that can sustain earnings while managing margin pressure, credit risk and ongoing expansion. The recent analyst focus on profit resilience supports that thesis but does not materially change the key short term catalyst, which remains upcoming earnings clarity on net interest margin trends, or the main risk, that expansion and integration costs or weaker demand could weigh on profitability.

Among recent developments, analysts have lifted Huntington’s average 12 month price target slightly, with one major firm raising its target to US$23 and expressing optimism about loan growth, net interest margin and capital return. This renewed attention ties directly into the near term earnings catalyst, as it reflects how closely the market is watching Huntington’s ability to balance growth, pricing and risk across both its core Midwest base and newer growth markets.

Yet beneath the renewed confidence, investors should be aware of the risk that Huntington’s expansion and integration efforts could...

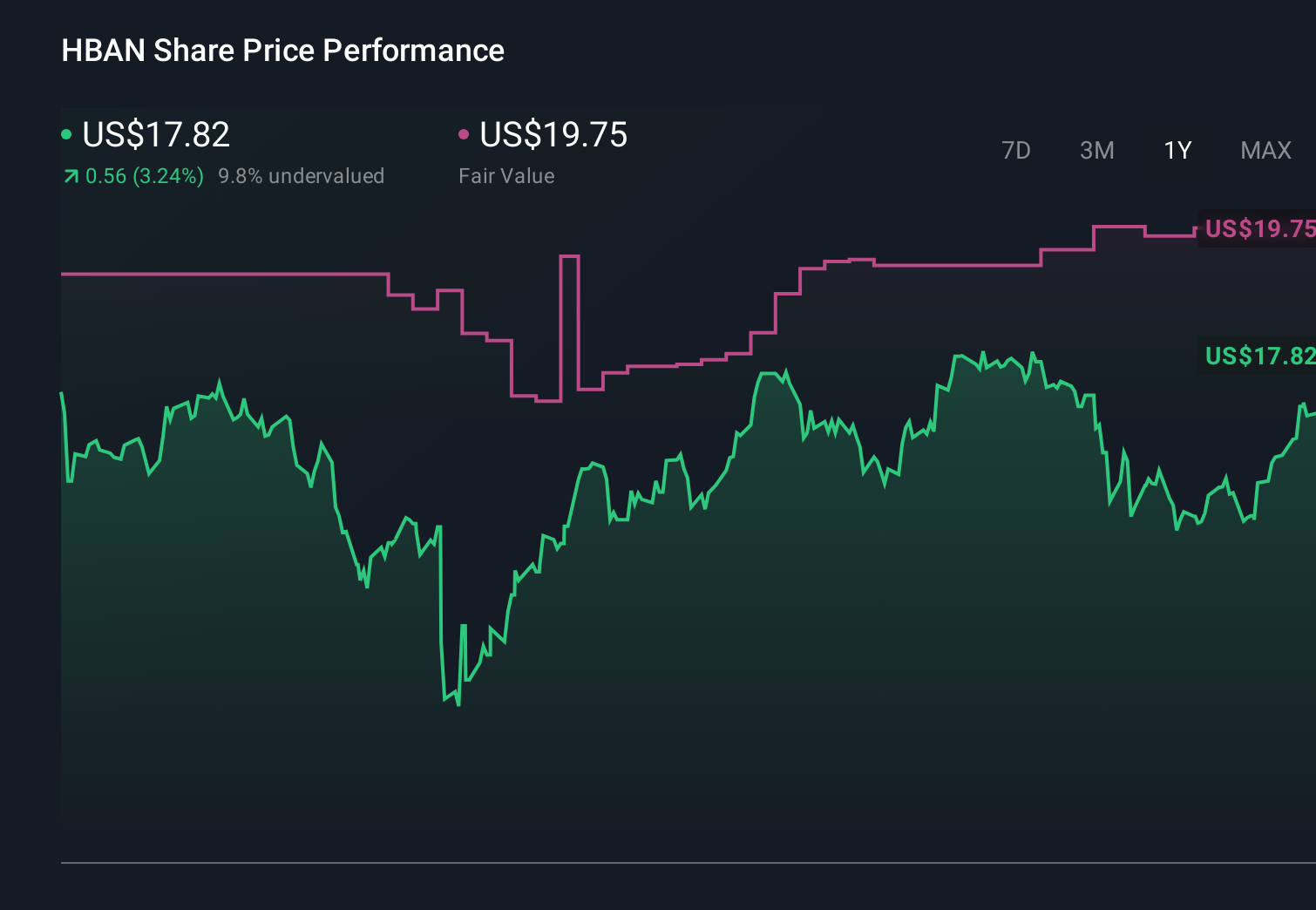

Huntington Bancshares' narrative projects $8.9 billion revenue and $2.3 billion earnings by 2028. This requires 7.3% yearly revenue growth and about a $0.3 billion earnings increase from $2.0 billion today.

Uncover how Huntington Bancshares' forecasts yield a $20.50 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently estimate Huntington’s fair value between US$20.50 and about US$35.90, highlighting very different expectations. You should weigh these views against the central issue of how profit resilience and margin pressures may shape Huntington’s earnings power over time, and consider how differing assumptions about those drivers can lead to very different conclusions about the stock.

Explore 3 other fair value estimates on Huntington Bancshares - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Bancshares research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Huntington Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Bancshares' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.