Should Strong Q1 2026 Results and Global Same‑Store Sales Growth Require Action From MINISO (MNSO) Investors?

MINISO Group Holding Ltd. Sponsored ADR MNSO | 0.00 |

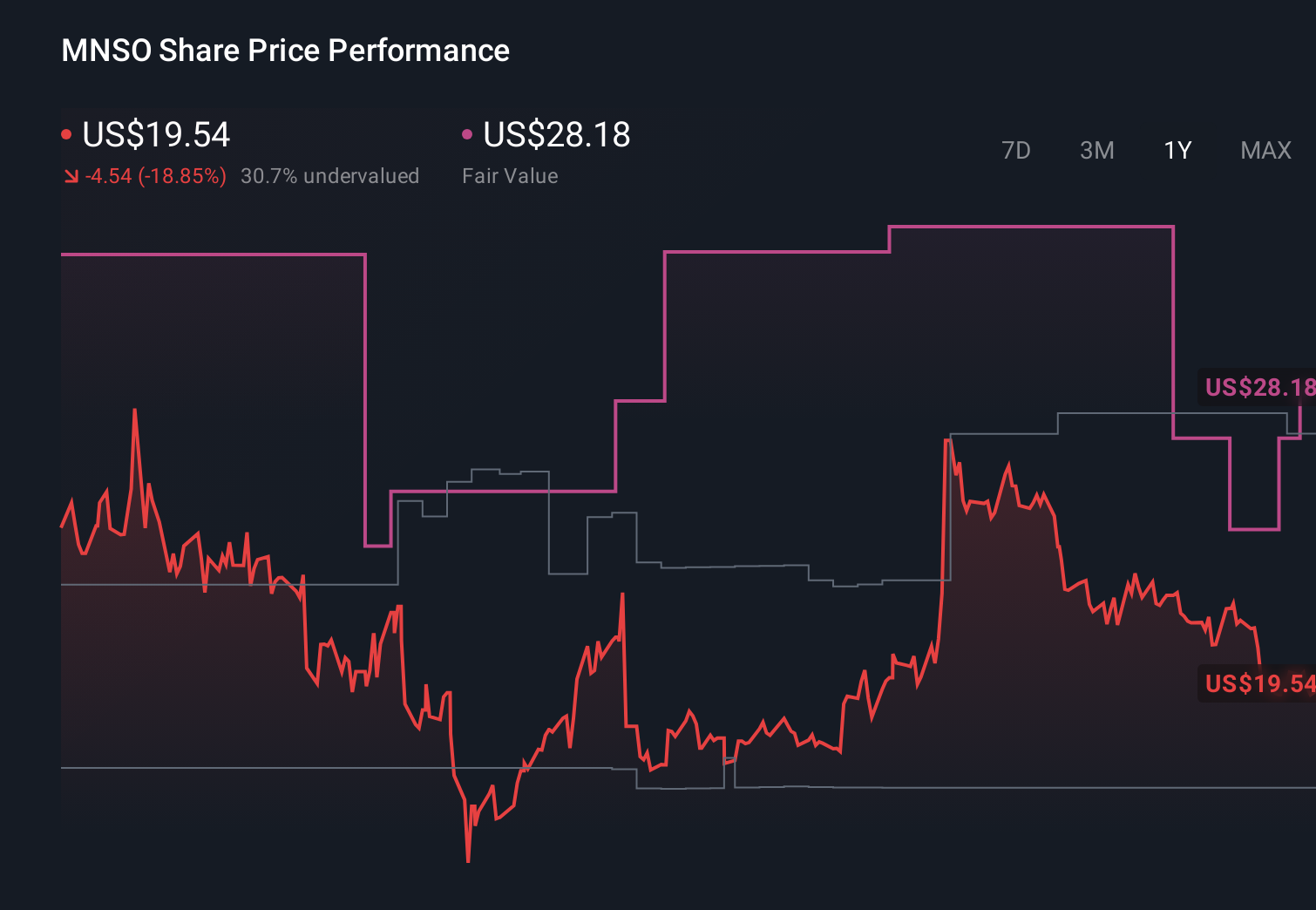

- MINISO Group Holding Limited reported past first-quarter 2026 results with sales of CNY 5,688.39 million and net income of CNY 1,250.74 million, both higher than a year earlier, alongside increased basic and diluted earnings per share from continuing operations.

- These results highlighted robust same-store sales growth in both the Chinese mainland and overseas markets, reinforcing the importance of MINISO’s expanding global footprint and product appeal across regions.

- Next, we’ll examine how this strong first-quarter revenue and earnings performance may influence MINISO’s longer-term investment narrative and outlook.

Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

MINISO Group Holding Investment Narrative Recap

To own MINISO, you generally need to believe that its global store rollout and IP led product mix can keep driving healthy same store sales while costs stay in check. The strong Q1 2026 revenue and profit figures support that growth story in the near term, but they do not remove the key risk that rapid physical expansion and rising expenses could eventually weigh on margins if demand cools or new stores underperform.

The most relevant recent announcement here is JPMorgan’s post earnings move to cut its MINISO price target to US$16 from US$26 while keeping an Overweight rating. That reaction underlines how, even after a quarter of 28.5% year on year revenue growth, some analysts remain focused on execution risks around store expansion and profitability rather than simply extrapolating one strong set of results into the future.

Yet even with these gains, investors should still be watching the risk that rising selling and labor costs could...

MINISO Group Holding's narrative projects CN¥33.1 billion revenue and CN¥3.9 billion earnings by 2029. This requires 15.6% yearly revenue growth and about CN¥2.7 billion earnings increase from CN¥1.2 billion today.

Uncover how MINISO Group Holding's forecasts yield a $23.25 fair value, a 76% upside to its current price.

Exploring Other Perspectives

The most bullish analysts were expecting revenue near CN¥37.0 billion by 2029 and earnings around CN¥4.8 billion, so Q1’s outperformance may either reinforce or challenge that optimism depending on how you view the ongoing threat from e commerce and store traffic pressure.

Explore 7 other fair value estimates on MINISO Group Holding - why the stock might be worth just $20.71!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MINISO Group Holding research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MINISO Group Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MINISO Group Holding's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.