Southern Copper (SCCO) Is Up 11.1% After Long-Term Expansion Plan Offsets Softer Output Outlook - What's Changed

Southern Copper Corporation SCCO | 177.83 | -0.07% |

- Southern Copper recently reported slightly lower 2025 copper production and trimmed its 2026 outlook due to lower ore grades at Peruvian operations, while outlining nearly US$19.90 billion of long-term growth projects aimed at lifting annual output by 2035.

- At the same time, the company has kept earnings momentum intact, with consistent estimate beats and strong technical strength suggesting ongoing institutional interest despite nearer-term operational constraints.

- Now we’ll examine how this mix of resilient earnings momentum and a softer near-term production outlook could reshape Southern Copper’s investment narrative.

Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Southern Copper Investment Narrative Recap

To own Southern Copper, you have to believe its long list of long-dated projects and strong recent earnings can offset near term production pressure and project execution risks. The latest guidance cut for 2025 and 2026 copper output highlights grade and operational uncertainty, but it does not fundamentally change the bigger near term swing factor, which still centers on cost control, project delivery in Peru and Mexico, and exposure to global trade tensions.

Against that backdrop, the company’s roughly US$19.90 billion investment plan to lift production by 2035 is particularly important, because it ties today’s softer output outlook directly to tomorrow’s volume potential. These projects sit alongside already elevated capital spending and community related risks, so investors may want to weigh the growth ambition against the pressure large, multi year capex can place on cash flow, especially if operating costs continue to trend higher than expected.

Yet beneath the strong recent share price performance, investors should also be aware that concentrated assets in Peru and Mexico leave Southern Copper exposed to...

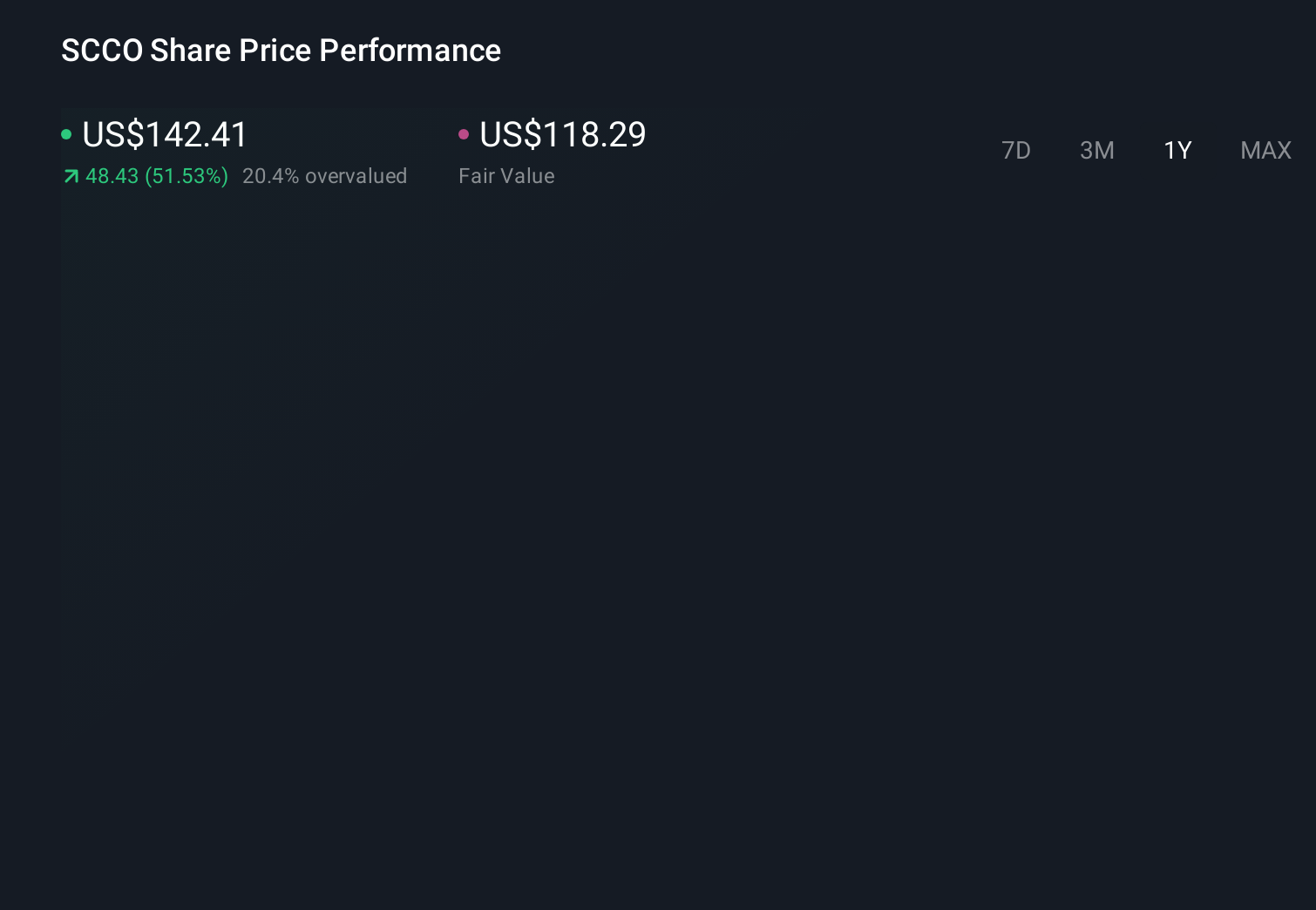

Southern Copper's narrative projects $13.0 billion revenue and $4.3 billion earnings by 2028. This requires 3.1% yearly revenue growth and about a $0.7 billion earnings increase from $3.6 billion today.

Uncover how Southern Copper's forecasts yield a $149.54 fair value, a 31% downside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts were assuming revenue near US$13.7 billion and earnings around US$4.9 billion by 2028, which is far more upbeat than consensus. In light of softer 2025 to 2026 production guidance and ongoing community and regulatory risks around projects like Tia Maria and Los Chancas, you may want to compare that optimistic path with more cautious views and decide which set of assumptions feels more realistic to you.

Explore 6 other fair value estimates on Southern Copper - why the stock might be worth as much as $218.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Southern Copper research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Southern Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southern Copper's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.