Southern Copper (SCCO) Is Up 8.6% After Copper Rally And Analyst Upgrades - What's Changed

Southern Copper Corporation SCCO | 0.00 |

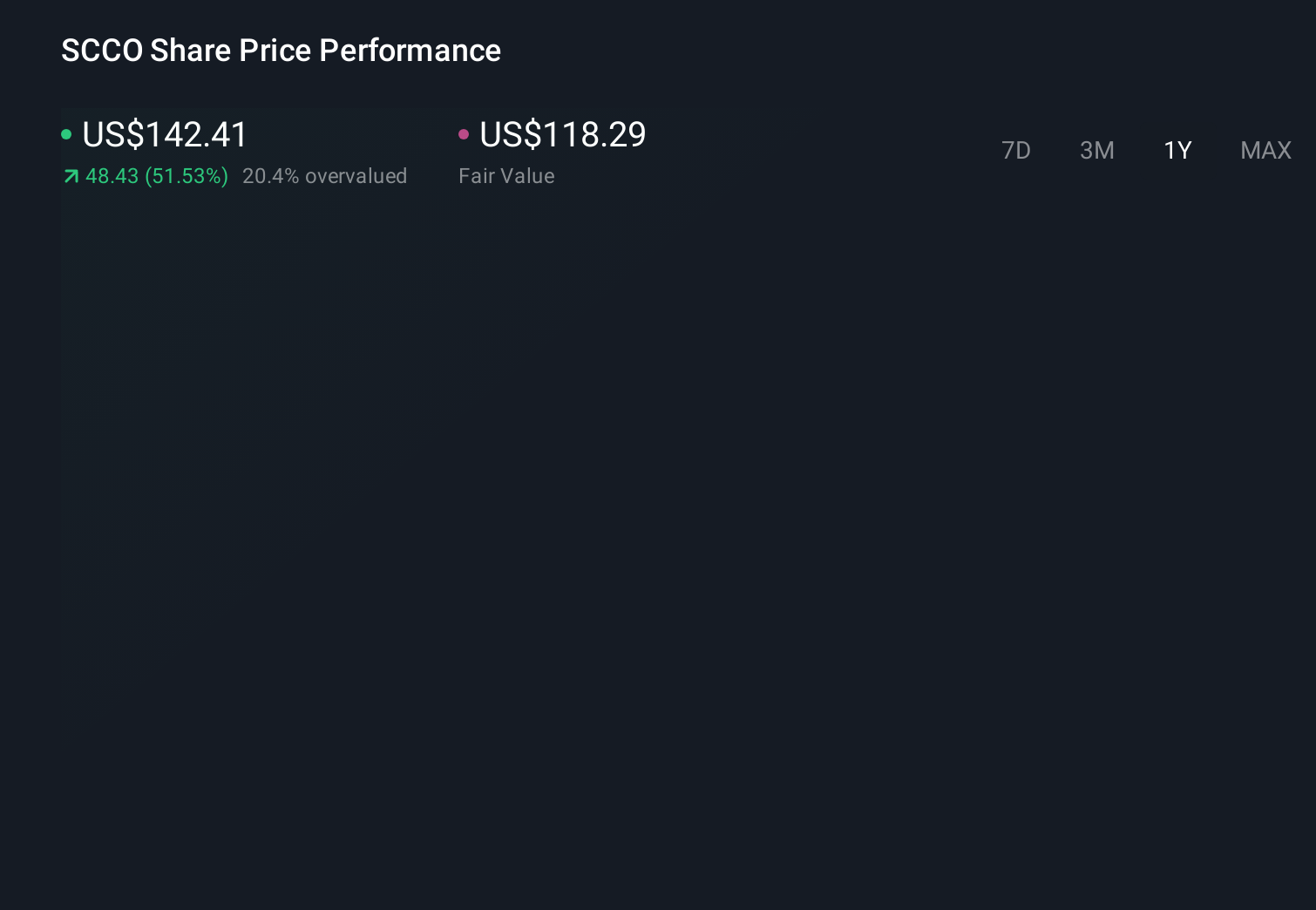

- In mid-July 2026, Southern Copper benefited from a broad upswing in mining names as gold, silver, and copper prices all moved sharply higher, while analysts at Zacks highlighted the company’s improving earnings estimates and favorable growth characteristics.

- This combination of stronger commodity pricing and an upgraded analyst stance has sharpened investor focus on how Southern Copper’s fundamentals might align with evolving expectations for its growth profile.

- We’ll now examine how the recent strength in copper prices could influence Southern Copper’s existing investment narrative built around major growth projects.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Southern Copper Investment Narrative Recap

To own Southern Copper, you need to believe that its large copper reserves and multi‑year growth projects can justify a premium valuation despite normal commodity and political volatility. The recent surge in metal prices and upbeat Zacks earnings revisions may support the near term catalyst around earnings momentum, but they do not remove the key risk of cost inflation and large capital spending potentially straining cash flow if conditions become less favorable.

In this context, the strong Q1 2026 results, with sales of US$4,251.4 million and net income of US$1,576.9 million, stand out. They highlight how higher realized prices and contributions from existing operations can support earnings while the company commits over US$15,000 million to long term projects such as Tia Maria, Los Chancas, and Michiquillay, which remain central to its growth story and to how investors assess today’s valuation.

Yet, against this backdrop, you should be aware of the risk that operating costs continue to rise faster than...

Southern Copper's narrative projects $16.5 billion revenue and $6.0 billion earnings by 2029. This requires 4.3% yearly revenue growth and about a $1.0 billion earnings increase from $5.0 billion today.

Uncover how Southern Copper's forecasts yield a $163.13 fair value, a 10% downside to its current price.

Exploring Other Perspectives

While consensus focuses on steady growth, the most optimistic analysts were already modeling earnings of about US$8.2 billion by 2029, which makes today’s copper price jump and ongoing regulatory and community risks around projects like Tia Maria and Los Chancas especially important for you to reassess which narrative you find more convincing.

Explore 4 other fair value estimates on Southern Copper - why the stock might be worth 40% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Southern Copper research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southern Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southern Copper's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.