Spotlight On May 2026's Leading Growth Stocks With Insider Ownership

Ramaco Resources-A METC | 0.00 |

Over the last 7 days, the United States market has risen 2.5%, contributing to a remarkable 26% climb over the past year, with earnings anticipated to grow by 17% per annum in the coming years. In this thriving environment, growth companies with high insider ownership are particularly noteworthy as they often demonstrate strong alignment between management and shareholder interests, potentially positioning them well for sustained success.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 33.4% | 74.1% |

| Upstart Holdings (UPST) | 14.1% | 58.1% |

| KVH Industries (KVHI) | 16.3% | 146.1% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| IEH (IEHC) | 37.3% | 114.7% |

| EHang Holdings (EH) | 30.1% | 55.4% |

| Corcept Therapeutics (CORT) | 11.7% | 48.7% |

| Astera Labs (ALAB) | 10.3% | 31.5% |

| AppLovin (APP) | 27.4% | 21.7% |

| Abeona Therapeutics (ABEO) | 16.7% | 32.9% |

Let's review some notable picks from our screened stocks.

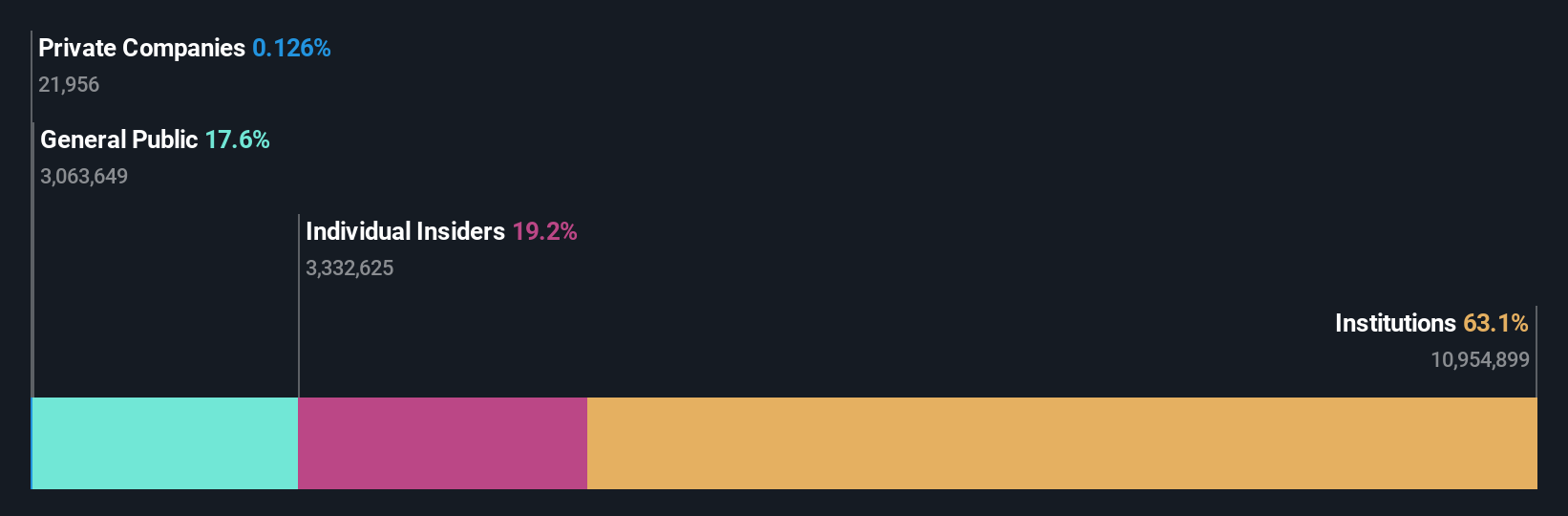

Boost Run (BRUN)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Boost Run, Inc. develops and provides cloud infrastructure for artificial intelligence and computing workloads, with a market cap of $1.56 billion.

Operations: Boost Run, Inc. generates revenue of $26.89 million from its computer services segment, focusing on cloud infrastructure for AI and computing workloads.

Insider Ownership: 13.8%

Earnings Growth Forecast: 101.5% p.a.

Boost Run's revenue is forecast to grow rapidly at 93.3% annually, outpacing the US market's growth rate of 11.7%, and its earnings are expected to increase significantly by 101.53% per year, becoming profitable within three years. Despite this potential, recent events highlight risks: delayed SEC filings and auditor concerns about ongoing viability. The company's share price has been volatile, and there have been no significant insider trading activities in the past three months.

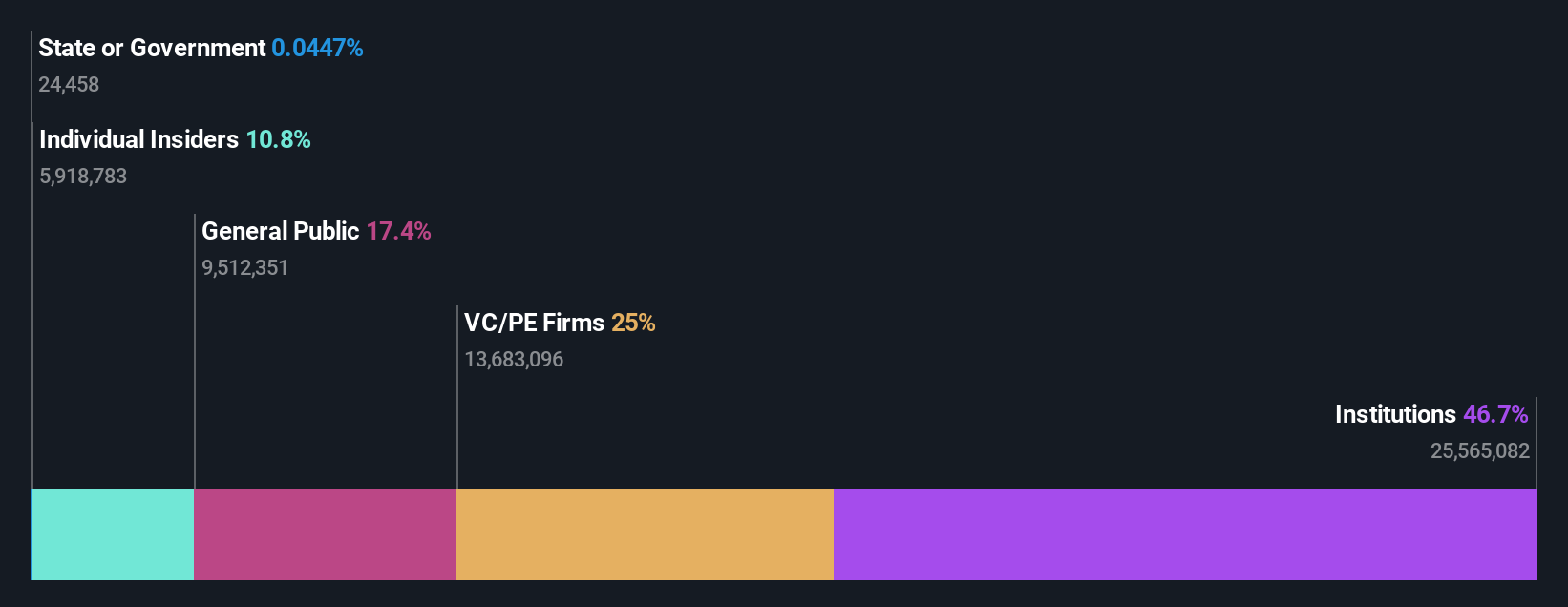

Bowman Consulting Group (BWMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bowman Consulting Group Ltd. provides engineering, technical consulting, and program management services in the United States with a market cap of $555.52 million.

Operations: The company's revenue primarily comes from offering engineering and related professional services, totaling $503.57 million.

Insider Ownership: 17.2%

Earnings Growth Forecast: 63.6% p.a.

Bowman Consulting Group is experiencing strong growth, with earnings expected to rise significantly by 63.56% annually over the next three years, outpacing the US market. Recent developments include a raised revenue guidance for 2026 and key contracts like a $22 million project with PhilaPort and a $4.9 million contract in Florida, enhancing multi-year revenue visibility. Despite trading below estimated fair value, Bowman faces challenges as interest payments are not well covered by earnings.

Ramaco Resources (METC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Ramaco Resources, Inc. is involved in the development, operation, and sale of metallurgical coal with a market cap of $863.91 million.

Operations: The company's revenue is primarily derived from the metallurgical coal segment, which generated $523.58 million.

Insider Ownership: 10.7%

Earnings Growth Forecast: 100.7% p.a.

Ramaco Resources is poised for significant growth, with earnings expected to grow by 100.74% annually, surpassing average market projections. Despite a recent net loss of US$18.32 million in Q1 2026 and decreased sales of US$121.61 million, the company anticipates full-year production between 3.7-4.1 million tons and sales of 4.1-4.5 million tons, indicating potential recovery and expansion opportunities in the coming years amidst high insider ownership levels.

Taking Advantage

- Navigate through the entire inventory of 173 Fast Growing US Companies With High Insider Ownership here.

- Curious About Other Options? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.