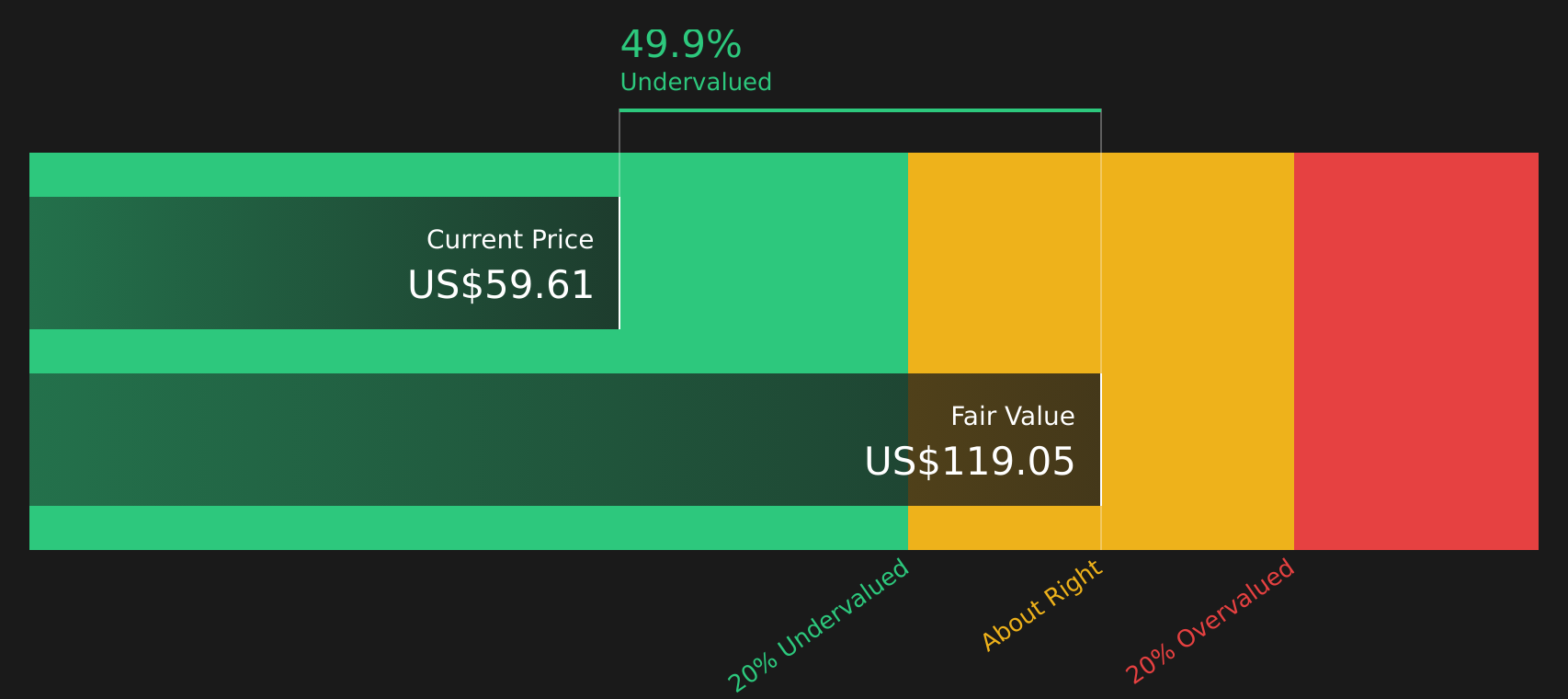

St. Joe (JOE) Could Be 49% Undervalued After Watersound Town Center Expansion

St. Joe Company JOE | 0.00 |

Watersound Town Center expansion puts St. Joe stock in focus

St. Joe (JOE) is drawing fresh investor attention after announcing a wave of new retailers, restaurants and service tenants at its Watersound Town Center open air lifestyle development in Inlet Beach, Florida.

The company highlighted recent openings from national and regional apparel brands, new dining and wellness concepts, and additional office users, along with plans for two more retail buildings to break ground later this year.

At a share price of $60.72, St. Joe has seen its short term share price momentum cool, with the 30 day share price return down 6.4% and the 90 day share price return down 6.8%, while the 1 year total shareholder return of 27.1% points to stronger longer term sentiment.

If the Watersound Town Center expansion has you thinking about longer term real estate themes, it can be useful to compare St. Joe with other asset heavy businesses and see how different stories are priced. A good starting point is a focused list of 20 top founder-led companies

After St. Joe’s strong 1 year run and more recent pullback, the puzzle now is whether Watersound fueled growth still leaves meaningful upside on the table or if most of the stock’s gains are already reflected in the price.

Price-to-Earnings of 31.1x: Is it justified?

On a P/E of 31.1x, St. Joe trades at a higher earnings multiple than both its US Real Estate peers at 13.3x and the broader US Real Estate industry at 24.6x, even after the recent pullback from $60.72.

The P/E ratio compares the share price to earnings per share, so a higher multiple often reflects the market assigning a richer price to each dollar of current earnings. For an asset heavy real estate developer and operator like St. Joe, that can reflect expectations around future cash generation from projects such as Watersound, as well as the quality and consistency of existing earnings.

At the same time, the SWS DCF model estimates a future cash flow value of $119.81 per share, which is well above the current $60.72 price. That gap, alongside a P/E that already sits ahead of peers and the industry, highlights a tension between what earnings multiples imply today and what a cash flow based valuation suggests the business could be worth if its projects and profitability stay on track.

Result: Price-to-Earnings of 31.1x (OVERVALUED).

However, St. Joe’s premium P/E and reliance on successful execution across residential, hospitality and commercial projects mean that delays, cost pressures or softer demand could quickly challenge the current narrative.

Another view on St. Joe’s value

While the 31.1x P/E suggests St. Joe is expensive next to peers and the broader US Real Estate industry, the SWS DCF model points in the opposite direction. On this view, an estimated future cash flow value of $119.81 per share versus today’s $60.72 price screens as undervalued.

Both methods rely on different assumptions, so the real question for you is which story you trust more: earnings today, or the cash flows the business could generate over time.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out St. Joe for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern around St. Joe leaves you undecided, take time to review the underlying numbers and form your own judgment using the 2 key rewards and 1 important warning sign

Looking for more investment ideas beyond St. Joe?

Do not stop your research with St. Joe; broaden your watchlist now using focused stock ideas so you are not relying on a single story.

- Target dependable cash flows with companies that have robust payouts by scanning 8 dividend fortresses before the next ex dividend dates start stacking up.

- Zero in on potential mispricings by reviewing 41 high quality undervalued stocks that already pair stronger balance sheets with appealing valuations.

- Strengthen your downside protection by filtering for 74 resilient stocks with low risk scores so sudden setbacks in one stock do not catch you off guard.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.