Standex International (SXI) Could Be 24% Undervalued After Russell Index Removal

Standex International Corporation SXI | 0.00 |

Standex International (SXI) was recently removed from several Russell value and small cap indexes, a technical event that could influence index fund positioning, passive ownership levels, and day to day liquidity for the stock.

Against this index removal backdrop, Standex International’s share price has had a strong run, with a year to date share price return of 37.70% and a 1 year total shareholder return of 86.87%. Shorter term moves have been more mixed, including a 7 day share price decline of 5.56% but a 90 day share price return of 15.41%. This suggests longer term momentum has been positive even as the latest index changes could be prompting some repositioning.

If you are weighing how this kind of index reshuffle might affect other opportunities, it can be useful to broaden your watchlist and scan 18 top founder-led companies

Given Standex International’s strong multiyear shareholder returns, alongside its removal from several Russell value and small cap indexes, are you looking at a business performance story, a sentiment swing around index flows, or some mix of both as you assess valuation next?

Most Popular Narrative: 6.5% Overvalued

Standex International last closed at $309.63 compared with a widely followed fair value estimate of $290.80, which is built on detailed growth and margin assumptions using an 8.7% discount rate.

The accelerating global shift towards automation, electrification, and grid modernization is driving persistent demand for Standex's high-value electrical, sensor, and precision engineering solutions, creating a runway for double-digit sales increases in fast growth end markets and supporting sustained above-GDP revenue growth.

Want to understand why this narrative still suggests the stock is overvalued, even with rising earnings and margins incorporated into the model? The answer lies in how projected growth, future profitability, and the implied P/E multiple interact in the valuation framework, and how much of that story the current share price already reflects.

Result: Fair Value of $290.80 (OVERVALUED)

However, Standex International’s reliance on acquisitions and exposure to trade and tariff changes could disrupt integration, pressure margins, and challenge the upbeat growth assumptions behind this valuation story.

Another View: SWS DCF Fair Value for Standex International

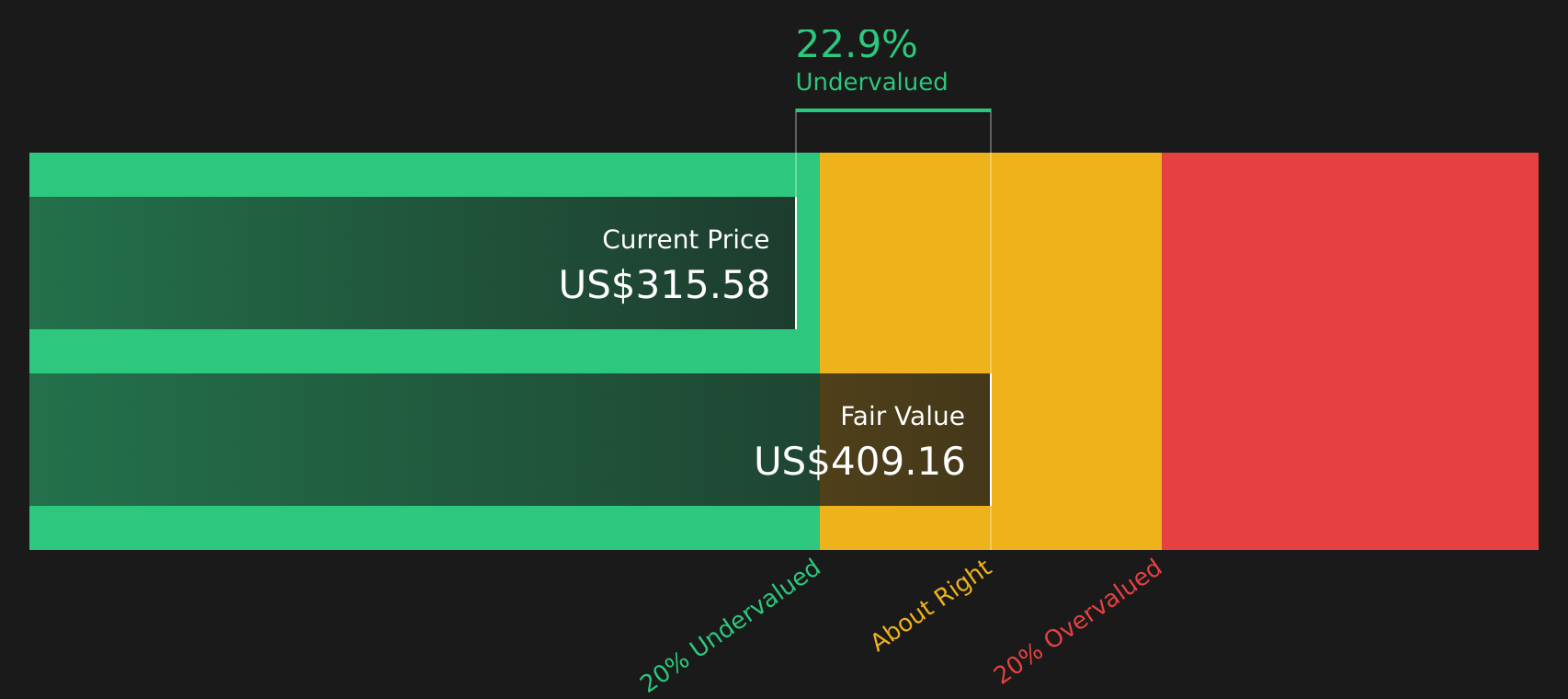

While the analyst-based fair value for Standex International sits at $290.80 and suggests the stock is 6.5% overvalued, the SWS DCF model points in the opposite direction, with a future cash flow value estimate of $408.19 indicating the shares trade at a 24.1% discount. Which set of assumptions do you find more convincing for your own framework?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Standex International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Feeling unsure whether Standex International’s mixed signals skew more positive or risky right now? Take a close look at the details, weigh them against your own expectations, and then size up the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Standex International?

If Standex International has you thinking harder about where to put your next dollar, do not stop here. The wider market holds plenty of other candidates worth your attention.

- Spot potential value opportunities early by scanning screener containing 19 high quality undiscovered gems before the broader market catches on.

- Strengthen your potential downside protection by checking companies in the 73 resilient stocks with low risk scores that score well on resilience.

- Prioritize balance sheet quality and fundamentals by running candidates through the solid balance sheet and fundamentals stocks screener (47 results) to see which stocks stand out.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.