Stanley Black & Decker (SWK) Rebounds Sharply, Is The Stock Already Fully Valued?

Stanley Black & Decker, Inc. SWK | 0.00 |

Stanley Black & Decker (SWK) is back in focus after recent share price moves, with investors weighing its tools and outdoor exposure, global footprint, and current valuation metrics against longer term return expectations.

The recent 30 day share price return of 15.76% and 90 day gain of 33.65%, alongside a 1 year total shareholder return of 42.16% but a 5 year total shareholder return that is down 47.07%, suggests improving momentum for Stanley Black & Decker while longer term holders are still catching up from earlier weakness.

If you are assessing how tools and industrial exposure fits into your portfolio, it can help to widen the lens and review other robotics and automation opportunities via the Simply Wall St screener for 29 robotics and automation stocks

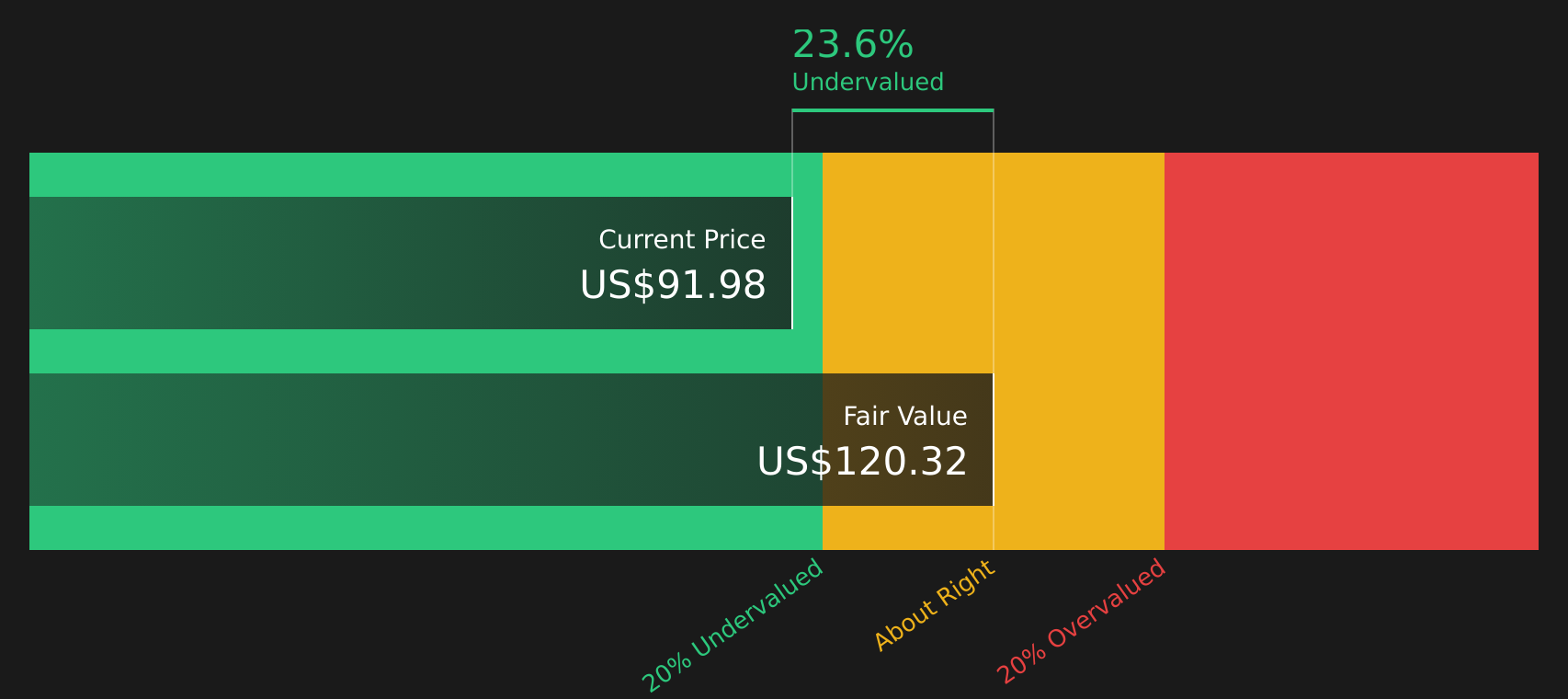

With Stanley Black & Decker trading near its analyst price target and an intrinsic value estimate that sits at a discount, the key question is whether the current share price still offers upside or if markets already reflect expectations for future growth.

Price-to-Earnings of 38.5x: Is it justified?

Stanley Black & Decker currently trades on a P/E of 38.5x, which sits close to its estimated fair P/E of 39.5x but above Machinery peers and leaves the stock pricing in a richer earnings profile than many competitors.

The P/E ratio compares the share price to earnings per share. A higher multiple generally reflects the market paying more today for each dollar of current earnings. For a tools and industrial business like Stanley Black & Decker, that usually ties back to expectations for how reliably those earnings can compound over time and how quickly profitability could improve from today’s base.

Here, the company is described as good value versus the estimated fair P/E of 39.5x, which suggests current pricing is close to the level the market could move towards if those assumptions play out. At the same time, the 38.5x P/E is described as expensive versus both the Machinery industry average of 28.3x and a peer group average of 25.9x. This indicates the stock trades on a premium multiple compared with many sector peers.

Result: Price-to-Earnings of 38.5x (ABOUT RIGHT)

However, Stanley Black & Decker still faces risks from its higher P/E premium if earnings expectations reset and from any slowdown in key tools and outdoor end markets.

Another View on Stanley Black & Decker’s Valuation

While the P/E of 38.5x suggests Stanley Black & Decker is trading close to its fair ratio of 39.5x, the SWS DCF model points in a different direction, with the stock at $91.98 versus an estimated future cash flow value of $119.77, implying undervaluation.

For investors, that gap raises the question of which signal matters more right now: earnings multiples or long term cash flow potential.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Stanley Black & Decker for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Stanley Black & Decker mixed between potential upside and clear risks, it makes sense to review the underlying data and decide quickly where you stand for yourself, starting with the balance of 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Stanley Black & Decker?

If you are weighing what to do next after reviewing Stanley Black & Decker, broaden your watchlist with other ideas that match your preferred risk and return profile.

- Target potential mispricings by scanning companies that combine quality fundamentals with attractive valuations using the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks offering resilient cash payouts screened through the 8 dividend fortresses.

- Dial down portfolio stress by focusing on companies with more resilient risk profiles inside the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.