Stanley Black & Decker (SWK) Valuation Check As Restructuring And Dividend Commitment Reshape Investor Expectations

Stanley Black & Decker, Inc. SWK | 0.00 |

Stanley Black & Decker (SWK) is reshaping its business after an aggressive acquisition phase by selling non core assets, tightening operations, and maintaining a 50 year dividend streak that keeps income focused investors watching the stock.

Recent price action has been mixed, with the share price down 3.19% over the past month but up 3.78% over 90 days and a 22.75% one year total shareholder return. This combination hints that restructuring progress and dividend resilience are gradually improving sentiment.

If you are weighing industrial stocks like Stanley Black & Decker against other long term opportunities, it can help to compare them with companies that have resilient business models and strong incentives at the top. Now might be a good time to broaden your search and check out 20 top founder-led companies

With the stock trading at a discount to both some analyst targets and certain intrinsic value estimates, the key question is whether this reflects lingering concerns or if markets are already factoring in the company’s potential for future growth.

Most Popular Narrative: 12.7% Undervalued

Against a last close of $78.48, the most followed narrative points to a fair value of about $89.87, putting the focus squarely on margins and earnings power rather than near term revenue momentum.

The multi year supply chain transformation nearing its final phase is delivering substantial recurring cost reductions, improved operational flexibility, and resilience to trade/tariff shocks. Management expects these initiatives to drive gross margin back to 35%+ by late 2026, supporting sustained improvements in net margins and earnings.

Want to see how modest top line assumptions, a steeper earnings ramp, and a lower future earnings multiple still add up to that valuation gap? The full narrative spells out the earnings path, margin rebuild, and discount rate that have to line up for this fair value to hold.

Result: Fair Value of $89.87 (UNDERVALUED)

However, the narrative can break if DIY and Outdoor demand stays weak or if heavy reliance on price increases continues to drive volume declines and margin pressure.

Another View: Earnings Multiple Sends a Different Signal

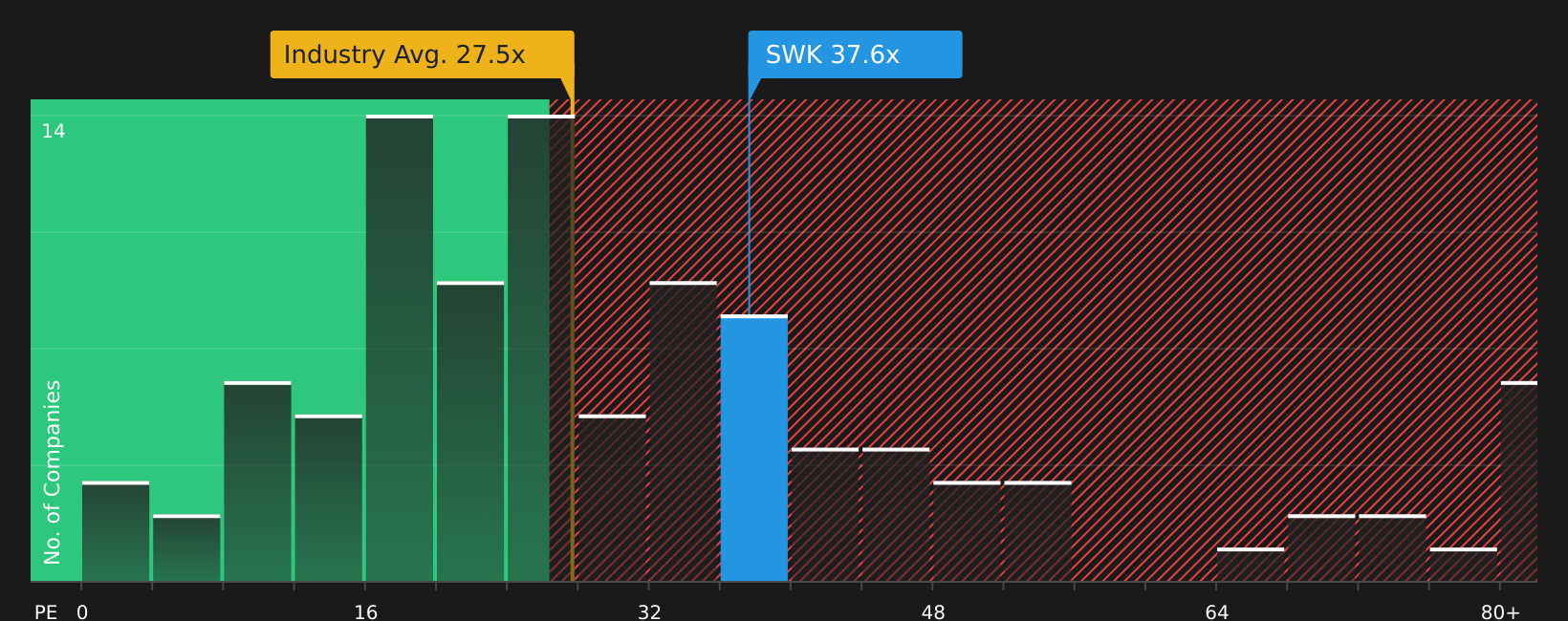

The fair value narrative points to a 12.7% undervaluation, but the current P/E of 32.9x tells a more cautious story. That multiple sits above the US Machinery industry at 26.7x and the 24.6x peer average, even if it is below the 38.1x fair ratio implied by our work.

In practice, that means the stock is already priced richer than many direct comparisons, so any earnings slip or slower progress on margins could weigh more heavily. On the other hand, if results move closer to the fair ratio, current pricing could look more reasonable. Which side of that trade off do you think is closer to reality?

Next Steps

With mixed signals on valuation, sentiment and business progress, it can be useful to review the underlying data yourself and move quickly to shape your own stance based on 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might fit your goals even better, so broaden your search before making your next move.

- Target resilient value by scanning companies that combine quality fundamentals with attractive pricing through the 49 high quality undervalued stocks.

- Secure potential income streams by checking out stocks offering stronger yields via the 9 dividend fortresses.

- Prioritize stability by focusing on companies with robust finances using the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.