Starwood Property Trust (STWD) Valuation Check After Share Buyback Plans And Dividend Hold

Starwood Property Trust, Inc. STWD | 0.00 |

Starwood Property Trust (STWD) is back in focus after announcing a US$400 million share buyback and maintaining its quarterly dividend, even as tighter coverage follows a recent dilutive acquisition and sector wide headwinds.

The share price is at US$18.05, with a 4.58% 1 month share price return contrasting with a small decline year to date, while the 1 year total shareholder return of 5.02% and 3 year total shareholder return of 48.81% show how patience has been rewarded even as recent acquisition concerns and sector headwinds temper short term momentum.

If this kind of income focused REIT has your attention, it can be helpful to see what else is moving, especially outside property. After reviewing STWD, broaden your search and check out 19 top founder-led companies

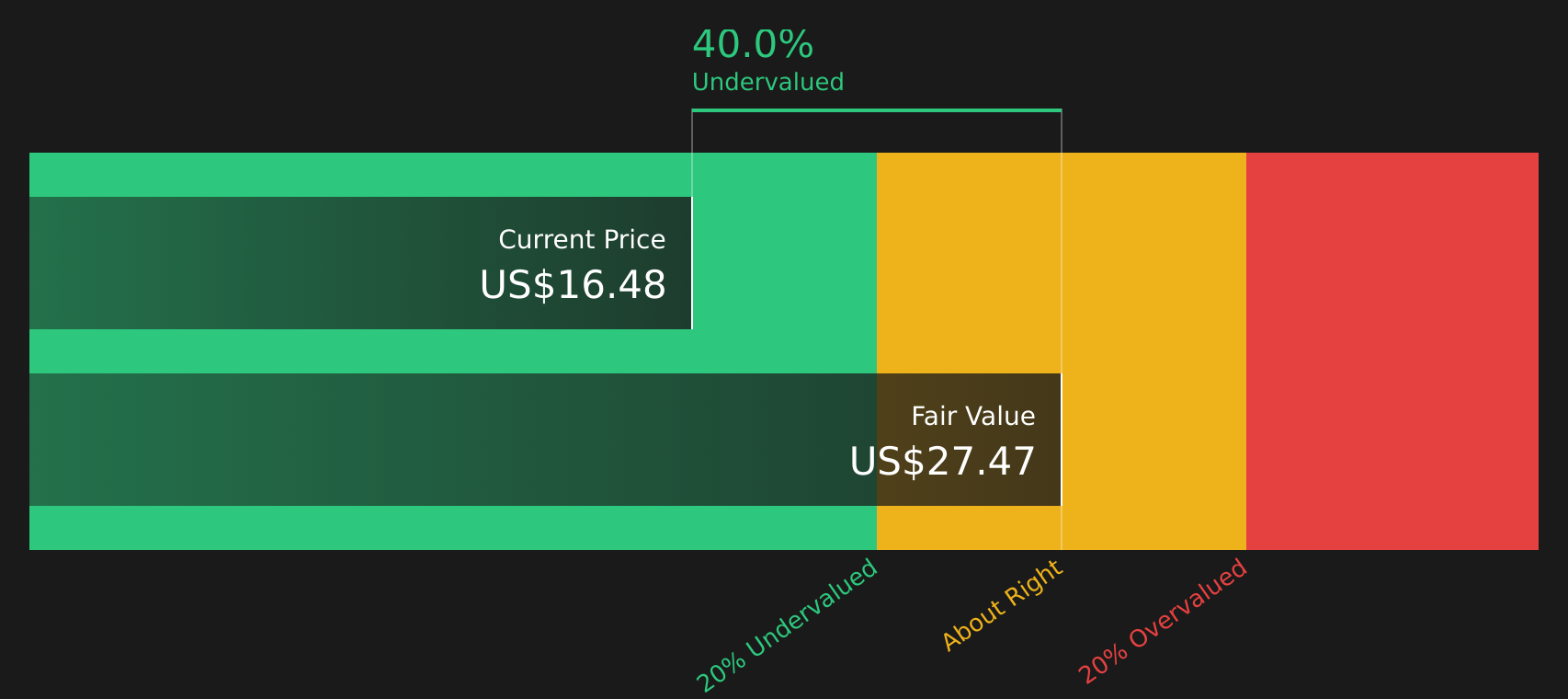

With the stock at US$18.05, a 14% discount to the average analyst price target and recent acquisition concerns still fresh, you have to ask: is this an income REIT on sale, or is the market already pricing in future growth?

Most Popular Narrative: 12.3% Undervalued

With Starwood Property Trust trading at $18.05 against a narrative fair value of $20.57, the current setup centers on whether earnings and buybacks can outweigh dilution and credit noise.

The acquisition and ramp-up of the net lease portfolio (Fundamental Income), combined with ongoing infrastructure lending growth, position Starwood to generate high-quality, durable earnings streams across a more diversified asset base, supporting both net margin expansion and greater earnings consistency.

Curious what kind of revenue surge, margin reset and future earnings multiple need to come together to support that valuation gap? The underlying projections lean on rapid top line expansion, a very different profit profile years out and a richer P/E than the broader mortgage REIT group. The full narrative lays out exactly how those moving parts are expected to line up.

Result: Fair Value of $20.57 (UNDERVALUED)

However, sizeable nonaccrual assets and integration risk around the US$2.2b Fundamental Income acquisition could still upset the earnings path implied by the current narrative.

Another Angle On Value

The SWS DCF model paints a much harsher picture, with an estimated future cash flow value of $7.40 per share compared with the current $18.05 price. That gap suggests meaningful downside risk if cash generation falls closer to the DCF assumptions than to the analyst narrative.

Before leaning on either view too heavily, it can help to see exactly how the cash flow math is built, where the key sensitivities sit, and which inputs you agree with most. You can then weigh that against your own expectations for dividend durability and deployment pace. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Starwood Property Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across valuation models and sentiment split between risks and rewards, now is the time to look through the details yourself and decide what matters most, starting with the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that could fit your goals better, so widen your lens and let the data do the work.

- Tap into potential mispricing by scanning a curated set of companies trading on compelling valuations through the 51 high quality undervalued stocks.

- Lock in your focus on income by checking stocks that combine higher yields with financial resilience using the 12 dividend fortresses.

- Prioritize peace of mind by filtering for companies with sturdier finances and robust fundamentals via the solid balance sheet and fundamentals stocks screener (44 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.