قد يُغيّر طرح شركة ستونكو لبرنامج ملكية أسهم الموظفين (ESOP) وانضمام أعضاء جدد إلى مجلس الإدارة من جدوى الاستثمار في شركة STNE

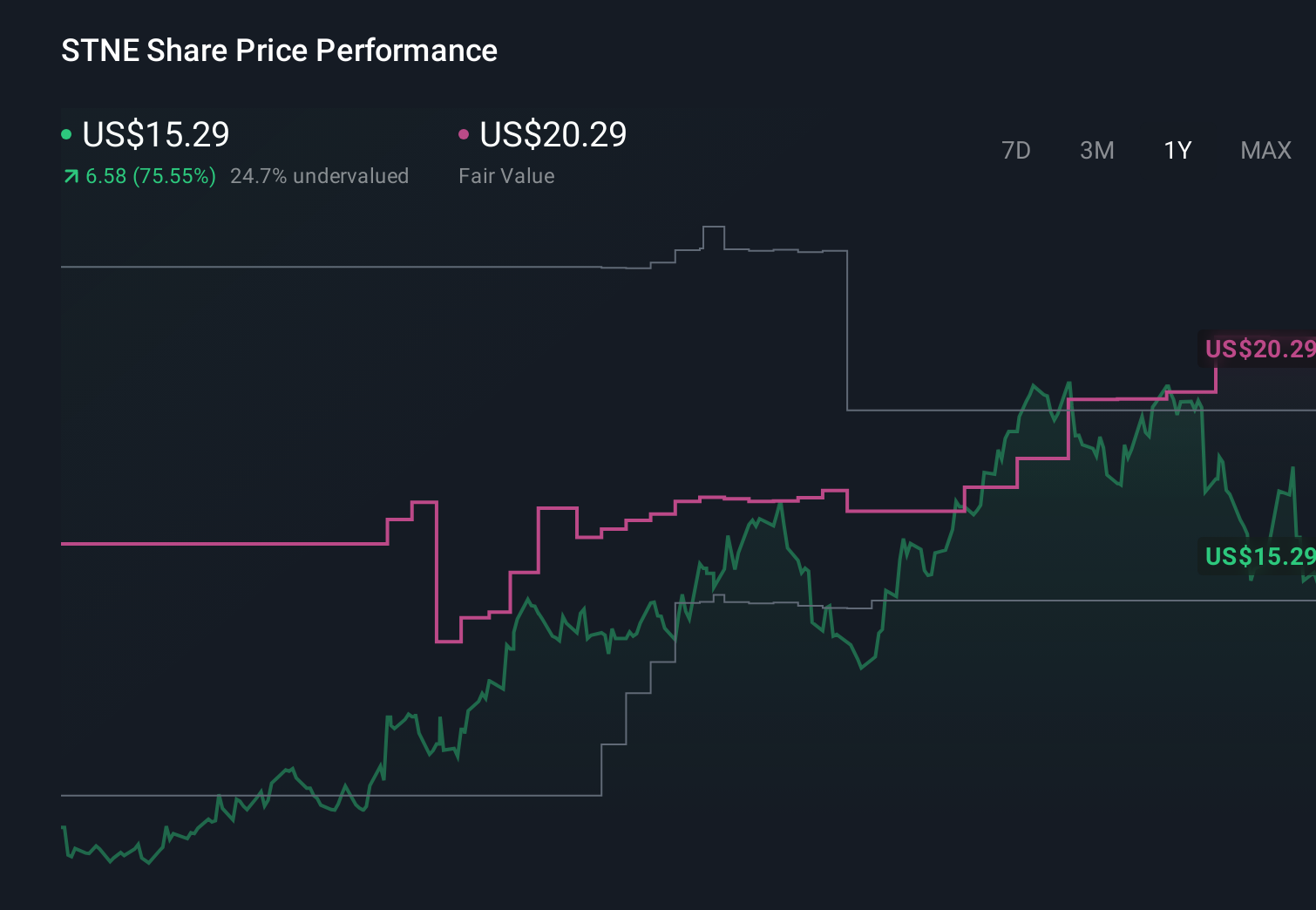

StoneCo Ltd. STNE | 0.00 |

- قدمت شركة StoneCo Ltd. مؤخرًا طلب تسجيل مسبق لما يصل إلى 41.19 مليون دولار أمريكي من الأسهم العادية، والتي تغطي 3,800,000 سهم في عرض متعلق ببرنامج ملكية أسهم الموظفين (ESOP)، وقد وافق المساهمون سابقًا على انتخاب مارسيلو كوبيل وبيدرو زينر كعضوين في مجلس الإدارة في الاجتماع العام السنوي المقرر عقده في 23 أبريل 2026.

- إن هذا المزيج من إصدار الأسهم المحتمل المرتبط بملكية الموظفين وتعيينات مجلس الإدارة الجديدة يسلط الضوء على نهج شركة ستونكو المتطور فيما يتعلق بهيكل رأس المال والحوكمة.

- بعد ذلك، سندرس كيف يمكن أن يؤثر تسجيل الأسهم المرتبط ببرنامج ملكية أسهم الموظفين (ESOP) على سردية الاستثمار لشركة StoneCo وتوقعاتها بشأن عوائد رأس المال المستقبلية.

استثمر في النهضة النووية من خلال قائمتنا التي تضم 91 مشروعاً رائداً في مجال البنية التحتية للطاقة النووية، والتي تدعم ثورة الذكاء الاصطناعي العالمية.

ملخص سردية استثمار ستونكو

لامتلاك أسهم شركة ستونكو اليوم، يجب أن تؤمن بأن تركيزها على مدفوعات الشركات الصغيرة والمتوسطة البرازيلية والخدمات المالية سيستمر في تحقيق أرباح قوية، حتى مع بقاء المنافسة ومخاطر الائتمان من أهم الشواغل. ولا يؤثر تسجيل برنامج ملكية أسهم الموظفين (ESOP) والتغييرات الأخيرة في مجلس الإدارة بشكل جوهري على المحفز القريب، وهو إعلان الأرباح المرتقب في 14 مايو، ولا على الخطر الرئيسي المتمثل في تباطؤ نمو حجم المدفوعات وارتفاع المخصصات في ظل بيئة اقتصادية كلية أكثر ضعفاً.

يأتي تسجيل أسهم عادية بقيمة تصل إلى 41.19 مليون دولار أمريكي ضمن برنامج ملكية أسهم الموظفين (ESOP) بالتزامن مع قرار شركة ستونكو الأخير بدفع توزيعات أرباح استثنائية قدرها 2.53 دولار أمريكي للسهم الواحد، مما يشير إلى نهج أكثر فعالية في تحقيق عوائد رأس المال مع الاستمرار في استخدام الأسهم كأداة لتحقيق التوافق بين مصالح الموظفين. ويمكن أن يؤثر تطور هذا التوازن بين المدفوعات النقدية والتخفيف المحتمل لحصص الملكية على كيفية تقييم المستثمرين لعامل تحفيز الأرباح في ضوء التساؤلات المستمرة حول تخصيص رأس المال وقوة الميزانية العمومية.

ومع ذلك، فبينما تبدو عوائد رأس المال وملكية الموظفين جذابة، ينبغي على المستثمرين أيضًا أن يكونوا على دراية بالمخاطر التي قد تنجم عن ارتفاع المخصصات وتباطؤ نمو القيمة الإجمالية للأصول...

تتوقع شركة ستونكو تحقيق إيرادات بقيمة 17.4 مليار ريال برازيلي وأرباح بقيمة 5.0 مليار ريال برازيلي بحلول عام 2028. ويتطلب ذلك نموًا سنويًا في الإيرادات بنسبة 8.2٪ وزيادة في الأرباح بقيمة 6.3 مليار ريال برازيلي مقارنة بخسارة قدرها 1.3 مليار ريال برازيلي اليوم.

اكتشف كيف أن توقعات شركة StoneCo تؤدي إلى قيمة عادلة تبلغ 20.29 دولارًا ، أي بزيادة قدرها 83٪ عن سعرها الحالي.

استكشاف وجهات نظر أخرى

توقع بعض المحللين الأكثر تفاؤلاً في السابق إيرادات تقارب 19.0 مليار ريال برازيلي وأرباحًا تقارب 5.4 مليار ريال برازيلي، وهو ما يعتبر أكثر تفاؤلاً بكثير من الإجماع، ومع ذلك، يمكن إعادة النظر في هذه التوقعات وقصة العائد الرأسمالي الأقوى في ضوء إصدار برنامج ملكية أسهم الموظفين والمخاطر المستمرة لارتفاع خسائر الائتمان والرياح المعاكسة لحجم المدفوعات.

استكشف 9 تقديرات أخرى للقيمة العادلة لشركة StoneCo - لماذا قد تكون قيمة السهم أكثر من 5 أضعاف السعر الحالي!

توصل إلى استنتاجك الخاص

هل تختلف مع الروايات السائدة؟ نادراً ما تأتي عوائد الاستثمار الاستثنائية من اتباع القطيع، لذا اتبع حدسك.

- تُعد تحليلاتنا التي تسلط الضوء على 4 مكافآت رئيسية وعلامة تحذيرية مهمة واحدة قد تؤثر على قرارك الاستثماري نقطة انطلاق رائعة لأبحاثك حول شركة StoneCo.

- يقدم تقريرنا البحثي المجاني عن شركة StoneCo تحليلاً أساسياً شاملاً مُلخصاً في رسم بياني واحد - ندفة الثلج - مما يسهل تقييم الوضع المالي العام لشركة StoneCo بنظرة سريعة.

هل أنت مهتم بخيارات أخرى؟

أفضل فرصنا الاستثمارية لا تحظى بالاهتمام الكافي - في الوقت الحالي. سارعوا بالاستثمار مبكراً:

- قد لا تكمن أفضل أسهم الذكاء الاصطناعي اليوم في شركات عملاقة مثل إنفيديا ومايكروسوفت. اكتشف فرصتك الاستثمارية الكبيرة القادمة مع هذه الشركات الـ 19 الأصغر حجماً والمتخصصة في الذكاء الاصطناعي، والتي تتمتع بإمكانات نمو قوية بفضل ابتكاراتها في المراحل المبكرة في مجالات التعلم الآلي والأتمتة وتحليل البيانات، ما قد يضمن لك مستقبلاً مالياً مزدهراً.

- اكتشف الفرصة الكبيرة القادمة مع 21 سهمًا رخيصًا من النخبة يوازن بين المخاطرة والعائد.

- استكشف 26 شركة رائدة في مجال الحوسبة الكمومية تقود ثورة تكنولوجيا الجيل القادم وتشكل المستقبل من خلال تحقيق اختراقات في الخوارزميات الكمومية، والبتات الكمومية فائقة التوصيل، والأبحاث المتطورة.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.