StoneX Group (SNEX) Launches Bank Research As Its Undervalued Narrative Faces A Test

StoneX Group Inc. SNEX | 0.00 |

StoneX Group (SNEX) has drawn fresh attention after its subsidiary, StoneX Financial, launched a Financial Institutions Group research practice within The Benchmark Company. This move extends equity research coverage to regional and community banks.

StoneX Group’s launch of FIG research comes on the back of powerful momentum, with a 30 day share price return of 20.52%, a 90 day gain of 75.19% and a very strong 1 year total shareholder return of 126.58%, while the share price now trades at $137.28.

If this kind of move has you looking beyond a single stock, it could be a good moment to broaden your watchlist with 20 top founder-led companies

With StoneX Group now trading at $137.28, against an analyst price target of $123.00 and an intrinsic value estimate that sits higher than today’s price, investors may ask whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 11.4% Undervalued

StoneX Group is trading at $137.28 while the most followed narrative on the stock points to a fair value of $155. This raises a clear question about how much of the recent strength is already reflected in the price.

The reason SNEX is interesting now is that the company is becoming a larger, more strategically relevant financial intermediary at exactly the time when volatility, hedging demand, derivatives usage, commodity complexity, and cross-border flows remain elevated.

That matters because StoneX’s model benefits when clients need to hedge, trade, finance inventory, access liquidity, or manage risk. In uncertain markets, StoneX does not need to perfectly predict direction. It benefits from activity.

Want to understand why this fair value sits meaningfully above today’s price? The narrative leans heavily on earnings power, book value compounding and the impact of recent acquisitions. The core issue is how sustainable those drivers are. The full breakdown shows exactly which assumptions support that $155 figure.

Result: Fair Value of $155 (UNDERVALUED)

However, StoneX Group’s story could change quickly if volatility, interest rates or derivatives activity cool, or if the R.J. O’Brien integration proves more difficult than expected.

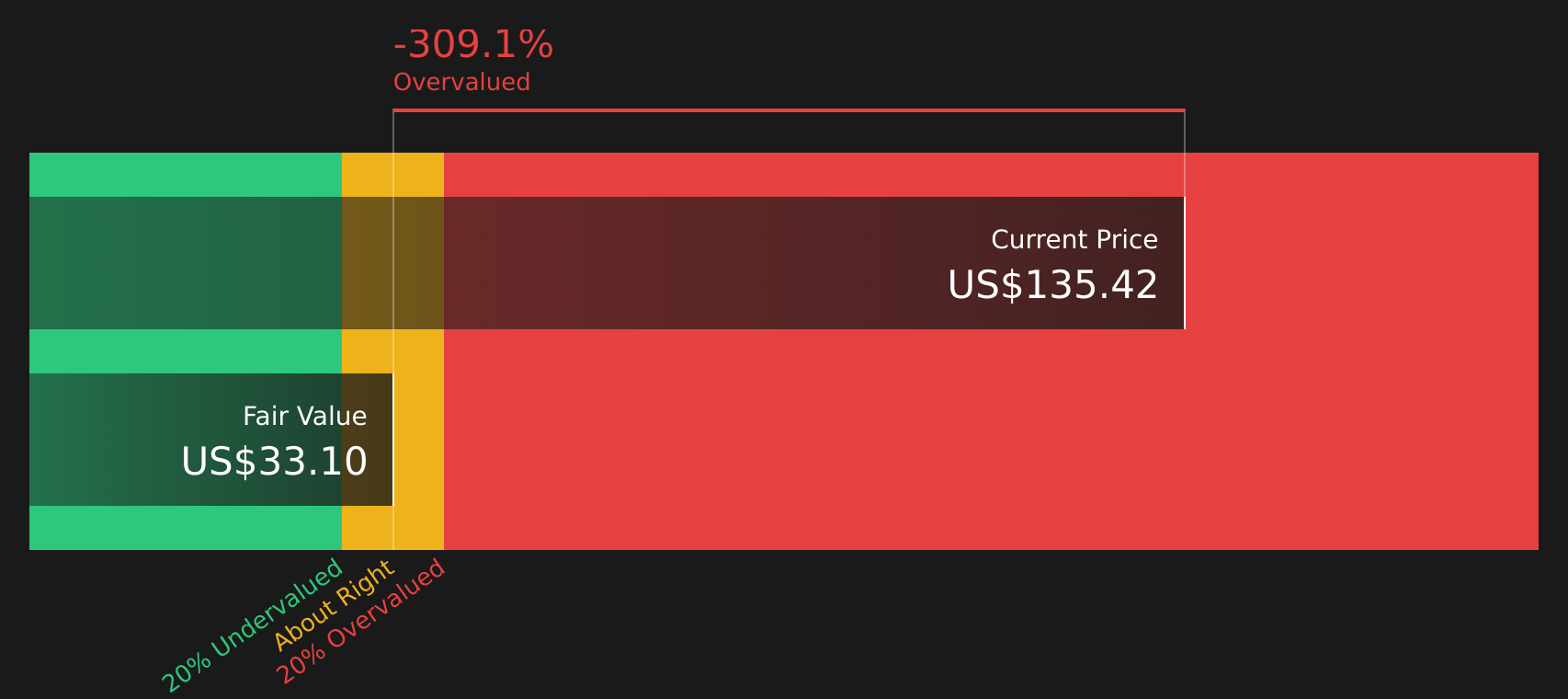

Another View: StoneX Group Through a Cash Flow Lens

While the user narrative argues StoneX Group is undervalued at a fair value of $155, the SWS DCF model points in a different direction. On this view, SNEX at $137.28 trades well above an estimated future cash flow value of $32.88, which frames the stock as expensive rather than cheap. Which story feels more robust to you: earnings power or long run cash flows?

For investors who want to see how this cash flow view is built from the ground up, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out StoneX Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With StoneX Group’s mixed signals on valuation and contrasting narratives, the real question is how you weigh the balance of risk and reward for yourself. Take a moment to look through the underlying data and then judge whether the trade off makes sense by reviewing the 3 key rewards and 1 important warning sign

Looking for more StoneX Group style investment ideas?

If StoneX Group has sharpened your focus, do not stop here, broaden your watchlist with other clear ideas that could strengthen your overall portfolio.

- Spot potential mispricing early by scanning for companies that look attractively valued using the 43 high quality undervalued stocks.

- Build a steadier income stream by reviewing companies that feature in the 9 dividend fortresses.

- Reduce portfolio stress by focusing on companies highlighted in the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.