Strait Of Hormuz Risk Puts Evergreen Marine And Chubb Stock In Focus

Chubb Limited CB | 0.00 |

Geopolitical risk in the Strait of Hormuz has moved from background worry to front page market factor, with an attack on a container ship and suspended evacuation plans rattling confidence in one of the world’s key energy arteries. For investors, this kind of disruption can reshape costs, reroute trade and alter risk pricing across shipping and marine insurance stocks. This article walks through three stocks exposed to the latest tensions, each facing potential headwinds from higher insurance premiums, unsettled vessel traffic and uncertain access to a critical shipping corridor.

Mitsui O.S.K. Lines (TSE:9104)

Overview: Mitsui O.S.K. Lines is a Japan based shipping and logistics group that moves bulk commodities, energy cargoes like oil and LNG, containers and vehicles worldwide, alongside ferry, cruise, real estate and support services such as terminals and logistics.

Operations: Mitsui O.S.K. Lines generates most of its revenue from Product Transport, with approximately ¥592.1b from car carriers, terminals and logistics, ¥537.0b from Energy, ¥456.0b from Dry Bulk and smaller contributions from container ships, real estate, ferries and associated businesses.

Market Cap: ¥1.81t

Investors looking at Mitsui O.S.K. Lines need to weigh its large exposure to energy and vehicle transport against some uncomfortable warning signs. The company sits in the middle of rising geopolitical risk in the Strait of Hormuz, where any disruption can feed directly into higher fuel, insurance and rerouting costs for its oil, LNG and container fleets. Recent results already show pressure on profit margins, weak cash flow coverage of debt and dividends, and a logistics business affected by trade policy shifts. At the same time, new ammonia and LNG contracts hint at long dated earnings streams that could offset some of that strain. The key issue for investors is whether these greener, contract backed projects can compensate for rising operating and financing risks in a more volatile shipping cycle.

Rising Hormuz risk and thinning cash coverage suggest Mitsui O.S.K. Lines’ balance sheet story may be more fragile than it looks, and the deeper concern only really appears once you review the Mitsui O.S.K. Lines financial health report

Evergreen Marine Corporation (Taiwan) (TWSE:2603)

Overview: Evergreen Marine Corporation (Taiwan) is a global container shipping and port services group that runs cargo vessels, container terminals and inland logistics. It also offers container manufacturing, storage, repair, leasing and related IT and consulting services across Asia, Europe, North America and other regions.

Operations: Evergreen Marine Corporation (Taiwan) generates almost all its revenue from its Transportation Division at about NT$437.8b, with only a small contribution from Other Department activities and an adjustment and write off line reducing reported totals.

Market Cap: NT$400.5b

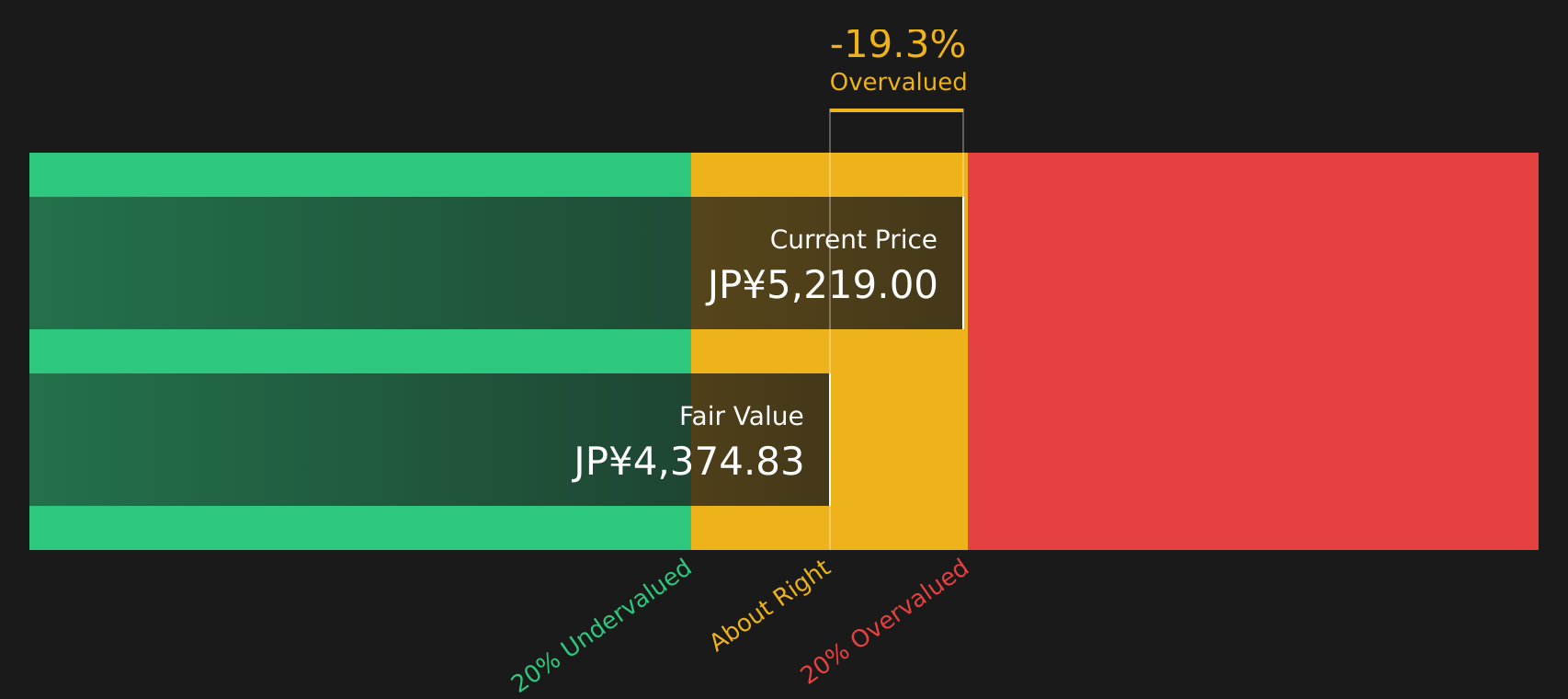

Evergreen Marine Corporation (Taiwan) is directly exposed to current Hormuz tensions as owner of the attacked container ship. Any prolonged disruption could mean longer routes, higher insurance costs and more volatile earnings on top of already shrinking profit margins and lower EPS. The stock screens as relatively cheap on P/E and analysts see room between price and target. However, recent results show revenue and net income well below last year, with ROE in single digits and dividends that have not been consistently reliable. With funding heavily reliant on external borrowing and management pay at the upper end of peers, investors may wish to consider whether the perceived value is sufficient compensation for rising operational and geopolitical risk in its core trade lanes.

Evergreen Marine’s shrinking margins, single digit ROE and hit ship suggest the real story may be rising risk, not cheap P/E. Before assuming the discount is harmless, read the 4 key rewards and 2 important warning signs

Chubb (CB)

Overview: Chubb is a global insurer and reinsurer that covers everything from commercial property, liability and marine risks to homeowners, autos, crop insurance and life products, serving both large corporations and individuals across many countries.

Operations: Chubb generates most of its revenue from North America Commercial P&C Insurance at about US$24.4b, Overseas General Insurance at US$16.1b, North America Personal P&C Insurance at US$7.4b and North America Agricultural Insurance at US$3.0b, with smaller contributions from Life Insurance at US$9.0b and Global Reinsurance at US$1.7b.

Market Cap: US$130.0b

Chubb is often viewed as a mix of disciplined underwriting and shareholder payouts. However, the current Strait of Hormuz crisis highlights how fragile that picture can be for a leading marine insurer tied into a US$400m war risk consortium and a US$20b reinsurance program. Higher premiums may not fully compensate if a major loss event occurs, particularly as some analysts have flagged pricing softness, margin pressure and an earnings trajectory that they expect to decline over the next few years. Combined with reliance on external borrowing, recent insider selling and underperformance relative to the broader US market, Chubb’s perceived value gap is accompanied by tail risks that investors may wish to consider carefully before relying on the stock’s reputation as a P&C “masterpiece.”

Chubb’s reputation as a P&C powerhouse may be masking how war risk exposure, pricing pressure and reliance on external borrowing really fit together, and the full picture only emerges in the 2 key rewards and 2 important warning signs (1 is major!)

Take Control of Your Investment Journey

If Mitsui O.S.K. Lines or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Beyond Shipping Risks?

Fresh ideas do not stay under the radar for long, and once momentum builds the best entry points can be gone. Scan these potential breakouts before the crowd and review them while they are still developing.

- Target reliable income streams while others chase headlines by reviewing the curated 54 dividend fortresses that focus on durable payouts in a world of uncertain yields.

- Spot early beneficiaries of the AI build out by using the hand picked 49 AI infrastructure stocks powering data centers, networking gear and supporting technology before momentum gets fully priced in.

- Monitor potential supply tightness by checking the focused 8 top copper producer stocks tied to electrification, grid upgrades and long term demand for this essential metal.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.