Strengthening Fundamentals And Higher Market Share Might Change The Case For Investing In Houlihan Lokey (HLI)

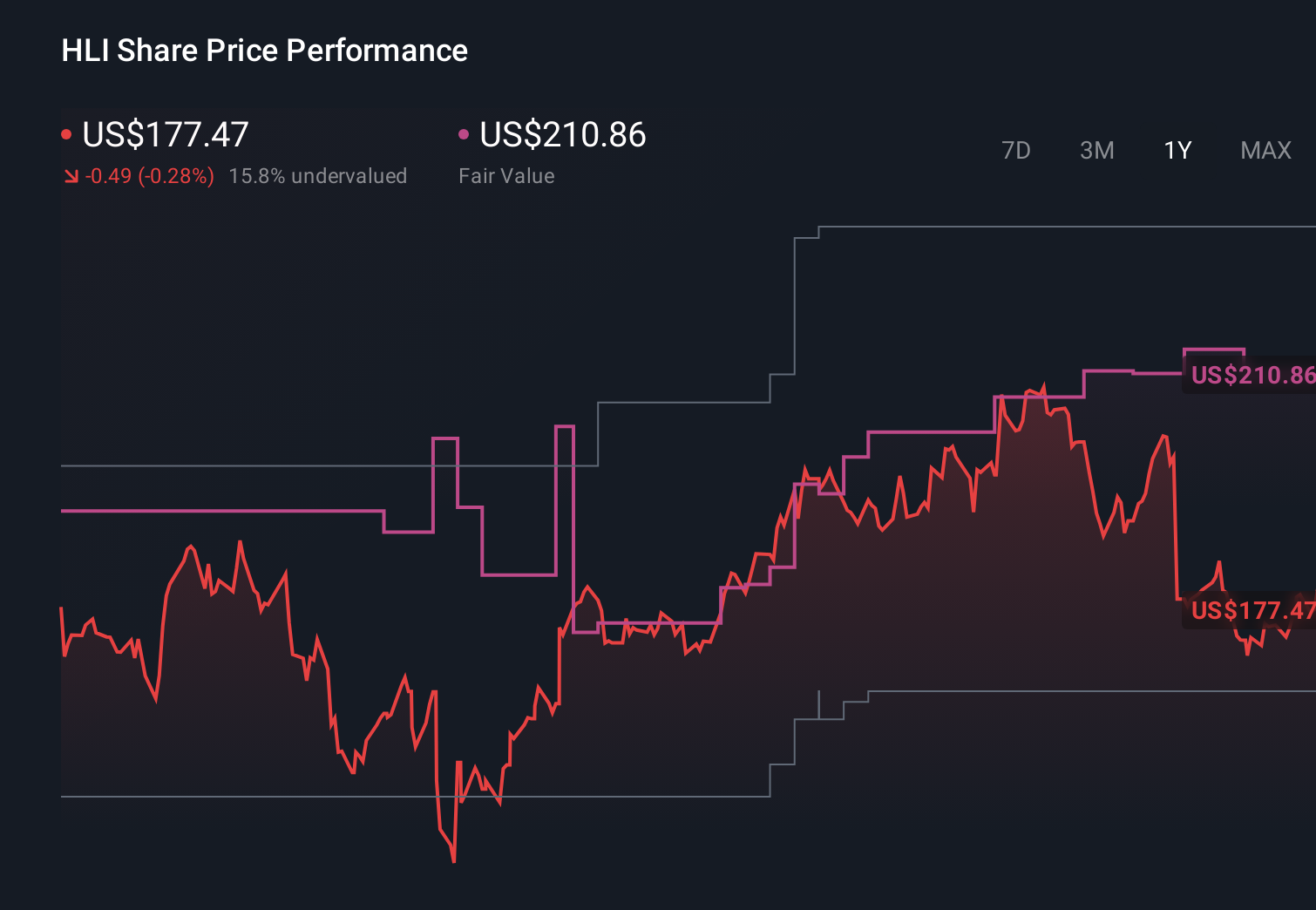

Houlihan Lokey, Inc. Class A HLI | 0.00 |

- In recent periods, Houlihan Lokey has reported strong growth in revenue, earnings per share and tangible book value per share, alongside a solid net cash position and rising market share in financial restructuring, M&A and valuation advisory.

- This combination of balance sheet strength and expanding franchise suggests the firm is actively building equity value through the current cycle rather than relying on leverage.

- We’ll now examine how Houlihan Lokey’s rising market share and solid fundamentals may influence its existing investment narrative and outlook.

This technology could replace computers: discover 31 stocks that are working to make quantum computing a reality.

Houlihan Lokey Investment Narrative Recap

To own Houlihan Lokey, you need to believe it can convert its strong balance sheet, rising market share, and diversified advisory platform into durable fee income, even if deal activity stays uneven across regions. The recent confirmation of robust revenue, EPS, and tangible book value growth supports the near term catalyst of continued earnings expansion, while also sharpening the key risk that high compensation and non-compensation costs could weigh on margins if activity slows.

The recent full year 2026 results, with net income of US$425.7 million and continued dividend growth to US$0.70 per quarter, are especially relevant here. They tie directly into the thesis that Houlihan Lokey is building equity value through disciplined capital returns and reinvestment in talent, while expanding in areas like restructuring and M&A advisory that underpin the current earnings trajectory and potential future catalysts.

Yet against this solid progress, investors should still watch closely for the risk that elevated restructuring revenue could fade faster than expected if...

Houlihan Lokey's narrative projects $3.6 billion revenue and $583.7 million earnings by 2029. This requires 11.0% yearly revenue growth and about a $158 million earnings increase from $425.7 million today.

Uncover how Houlihan Lokey's forecasts yield a $172.50 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue of about US$4.0 billion and earnings near US$591.5 million by 2029, which is a far more upbeat view than consensus. In light of Houlihan Lokey’s latest strong cash generation and rising market share, you may find that these higher forecasts, and concerns like automation reshaping advisory work, either look more reasonable or more stretched once you consider how the new data might reshape both narratives.

Explore 2 other fair value estimates on Houlihan Lokey - why the stock might be worth as much as 38% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Houlihan Lokey research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free Houlihan Lokey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Houlihan Lokey's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.