Strong 2025 Results and Acquisition Drive Might Change The Case For Investing In Everus Construction Group (ECG)

Everus Construction Group, Inc. ECG | 119.27 | -1.14% |

- In late February 2026, Everus Construction Group reported past fourth-quarter 2025 sales of US$1,011.47 million and full-year sales of US$3.75 billion, with net income of US$55.28 million for the quarter and US$201.77 million for the year, alongside revenue guidance of US$4.10 billion to US$4.20 billion for 2026.

- A day later, management highlighted a strengthened balance sheet and active M&A pipeline, signaling an intention to use acquisitions to broaden Everus Construction Group’s geographic reach and service mix while maintaining disciplined capital spending and financial flexibility.

- With this combination of robust 2025 earnings and a newly emphasized acquisition push, we’ll now examine how it reshapes Everus Construction Group’s investment narrative.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Everus Construction Group Investment Narrative Recap

To own Everus Construction Group, you need to believe its focus on complex infrastructure and data center work can support earnings while it leans more into acquisitions. The latest results and 2026 revenue guidance are helpful markers, but the bigger near term swing factor is how any deals affect returns and balance sheet flexibility. The main risk is still that capital deployed into M&A does not translate into sustainable earnings power.

The clearest link to this story is Everus’s late February 2026 update that it is actively pursuing a “broad and deep” M&A pipeline, supported by low leverage and ample liquidity. That push sits directly against the risk of overpaying for targets or integrating businesses that dilute margins, especially after a strong year like 2025, when adjusted EBITDA and net income are already supporting a relatively full earnings multiple.

Yet behind the strong 2025 numbers, investors should be aware that the real test may come if acquisition prices stay high and integration proves harder than...

Everus Construction Group’s narrative projects $4.3 billion revenue and $220.5 million earnings by 2028. This requires 7.2% yearly revenue growth and about a $39.5 million earnings increase from $181.0 million today.

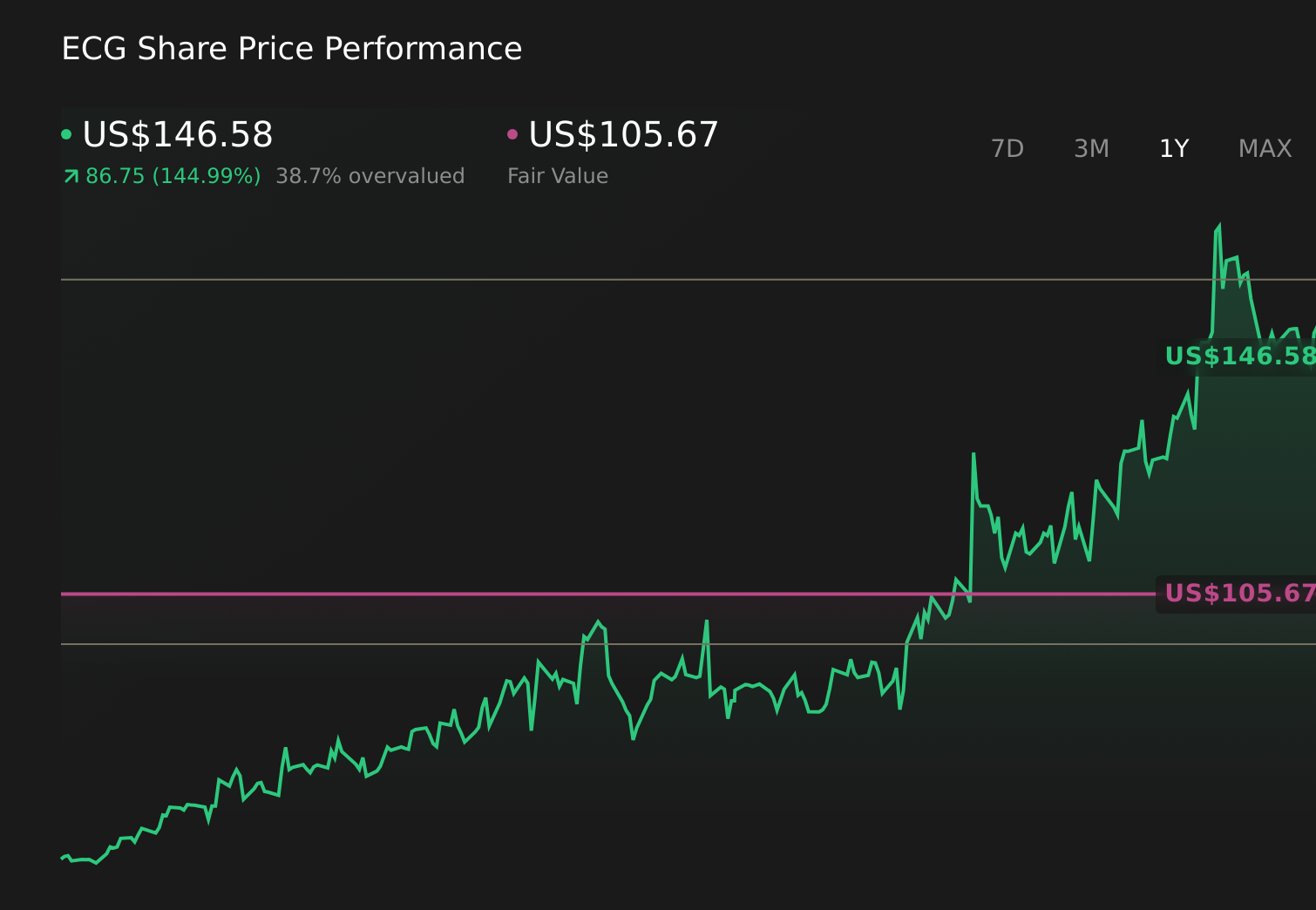

Uncover how Everus Construction Group's forecasts yield a $105.67 fair value, a 9% downside to its current price.

Exploring Other Perspectives

The lowest analyst estimates painted a more cautious picture, with revenue seen rising to about US$4.3 billion and earnings to roughly US$250 million, so you should weigh that more pessimistic view of acquisition and margin risks against the stronger 2025 results and the broader M&A ambitions described by management.

Explore 4 other fair value estimates on Everus Construction Group - why the stock might be worth 39% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Everus Construction Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Everus Construction Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Everus Construction Group's overall financial health at a glance.

No Opportunity In Everus Construction Group?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.