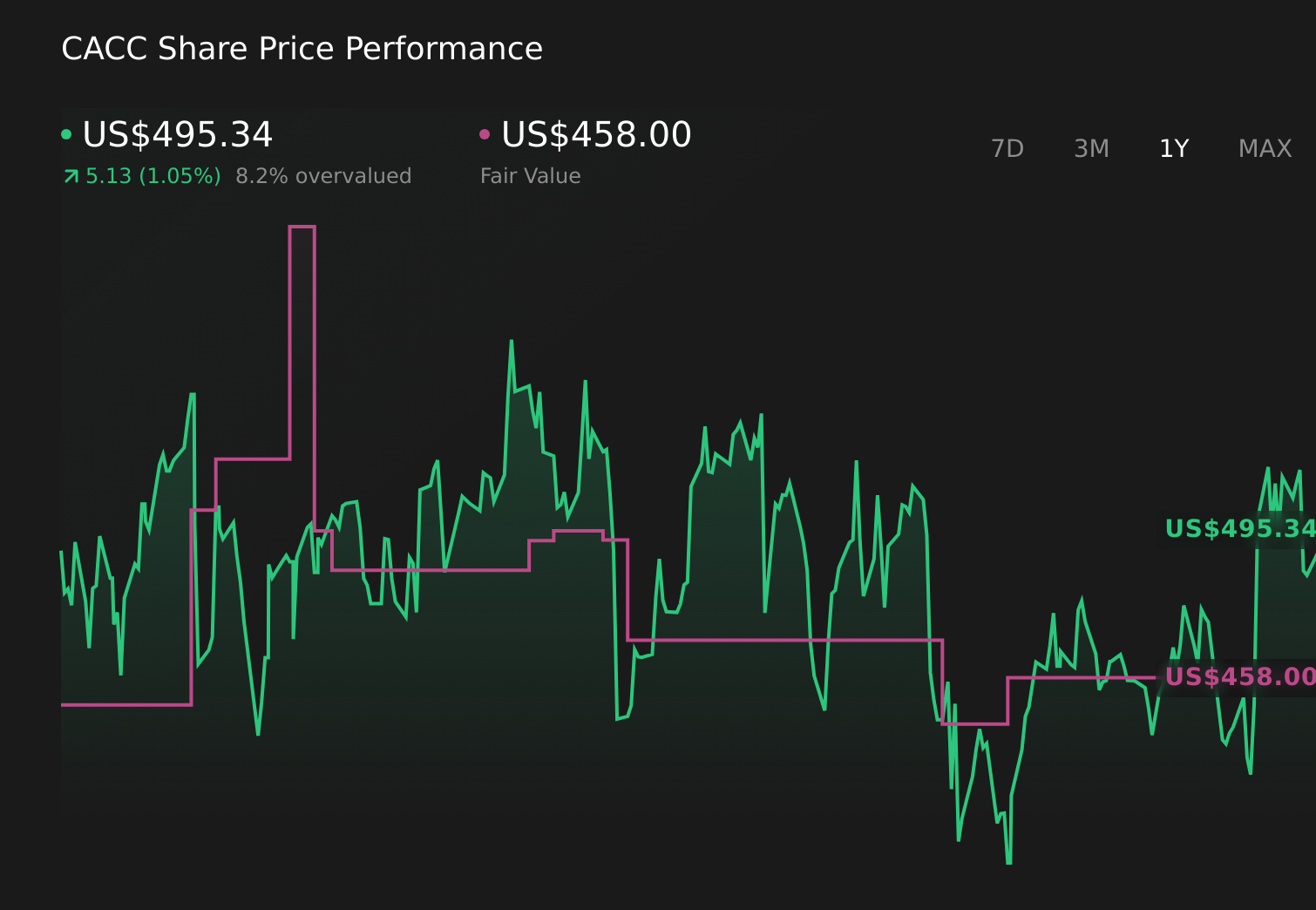

Stronger Profitability and Capital Returns Might Change The Case For Investing In Credit Acceptance (CACC)

Credit Acceptance Corporation CACC | 0.00 |

- In the first quarter of 2026, Credit Acceptance Corporation reported revenue of US$580.0 million and net income of US$135.8 million, alongside basic earnings per share from continuing operations of US$12.64, all higher than a year earlier.

- On the same day, the company completed a US$450.0 million asset-backed non-recourse financing and finished a buyback of 588,925 shares, signaling an emphasis on balance sheet efficiency and capital returns.

- We’ll now examine how Credit Acceptance’s stronger profitability, supported by cost controls and efficiency gains, may influence its previously outlined investment narrative.

Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

Credit Acceptance Investment Narrative Recap

To own Credit Acceptance, you need to be comfortable with a subprime auto lender whose story hinges on disciplined credit risk management and efficient capital use. The latest earnings beat, margin improvement and asset backed financing support that thesis in the near term, while persistent credit performance uncertainty in recent loan vintages still looks like the key risk to watch; the impact of this quarter’s results on that bigger issue is helpful, but not yet decisive.

The US$450.0 million non recourse asset backed financing is particularly relevant here, as it refreshes funding at an expected 5.2% average cost and is intended to retire higher cost debt, potentially reinforcing near term earnings resilience if collection trends hold. Combined with the completed repurchase of 588,925 shares for US$275.72 million, it underlines how balance sheet structure could amplify or constrain the earnings impact of any future shifts in loan performance.

However, behind the stronger quarter, investors should still be aware of how continued underperformance in the 2022 to 2024 loan vintages could...

Credit Acceptance's narrative projects $3.6 billion revenue and $700.7 million earnings by 2029. This requires 40.7% yearly revenue growth and an earnings increase of about $247 million from $453.4 million today.

Uncover how Credit Acceptance's forecasts yield a $536.67 fair value, in line with its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span a wide band, from about US$341.70 to US$536.67, underscoring how far apart views can be. As you weigh those against the recent earnings beat and improving margins, remember that concerns about weaker vintage performance and credit risk could still shape how sustainably the business can support its current profitability.

Explore 2 other fair value estimates on Credit Acceptance - why the stock might be worth 38% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Credit Acceptance research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Credit Acceptance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Credit Acceptance's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.