Stronger Q1 2026 Earnings and Higher Dividend Could Be A Game Changer For Williams (WMB)

Williams Companies, Inc. WMB | 0.00 |

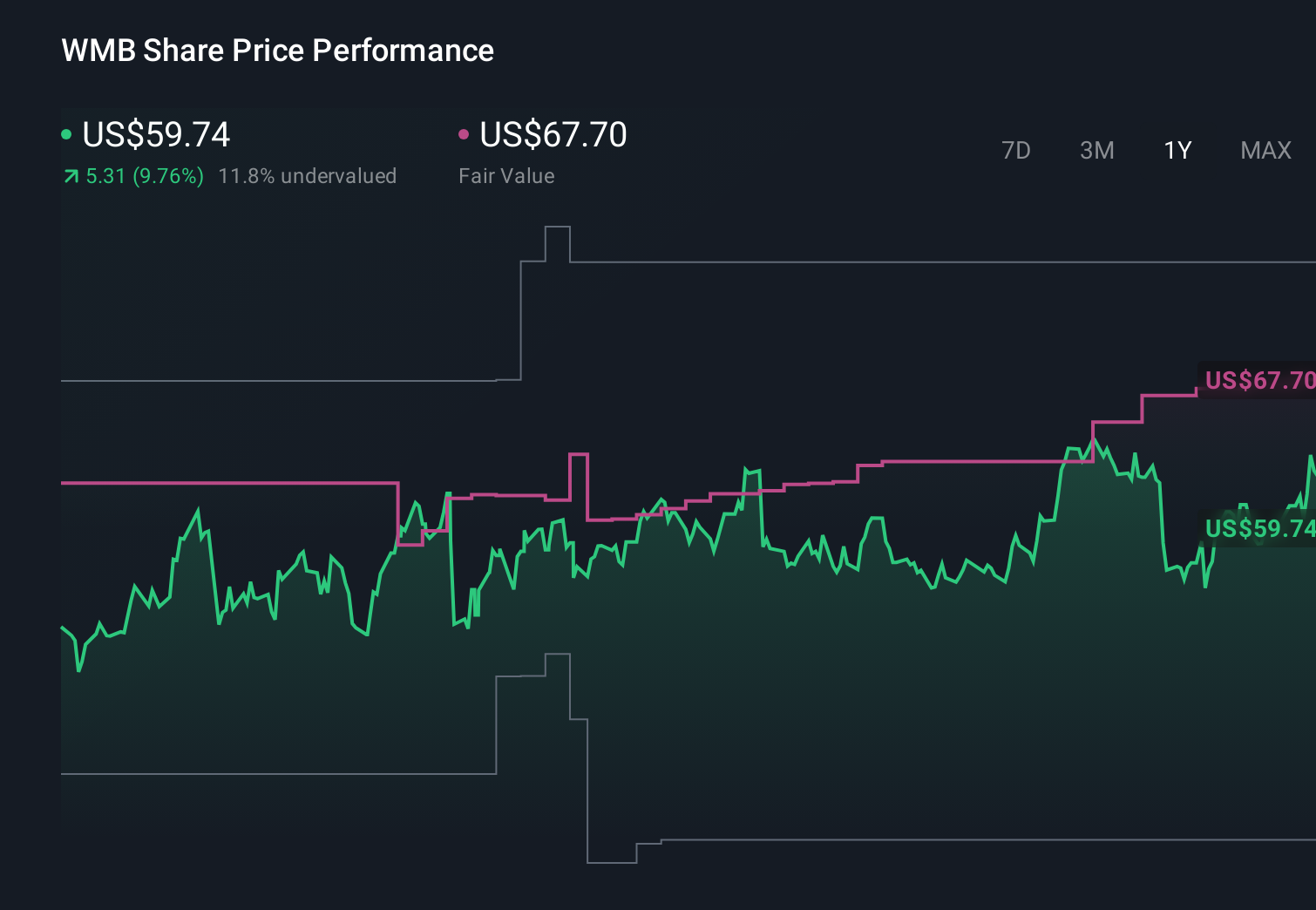

- The Williams Companies, Inc. has already reported first-quarter 2026 results, with revenue of US$3,030 million and net income of US$865 million, alongside basic earnings per share from continuing operations of US$0.71.

- Shortly after, the company approved a 5% increase in its regular quarterly dividend to US$0.525 per share, highlighting a focus on returning more cash to shareholders.

- Against this backdrop of higher earnings and a raised dividend, we’ll examine how the latest results might influence Williams Companies’ investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Williams Companies Investment Narrative Recap

To own Williams Companies, you need to believe that natural gas infrastructure will stay essential despite the energy transition, and that its pipeline network will remain well utilized. The latest quarter’s higher earnings and modest revenue change do not materially alter that big picture, but they may support confidence in the near term. The key short term catalyst remains execution on its large project backlog, while permitting delays and long cycle capital commitments still stand out as the biggest risks.

Among the recent announcements, the 5% dividend increase to US$0.525 per share is most relevant here, because it relies on Williams converting its contracted project backlog and existing assets into steady cash generation. For investors focused on catalysts, this dividend action sits alongside projects like NESE and Gulf Coast expansions, which are intended to underpin future earnings and potentially support the dividend over time if they are delivered as planned.

However, while earnings and dividends look solid today, investors should also be aware of the risk that long dated pipeline assets could eventually face...

Williams Companies’ narrative projects $16.3 billion revenue and $3.9 billion earnings by 2029. This requires 11.3% yearly revenue growth and a roughly $1.3 billion earnings increase from $2.6 billion today.

Uncover how Williams Companies' forecasts yield a $80.07 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already expecting slower progress, with revenue at about US$15.2 billion and earnings around US$3.1 billion by 2029, so you should weigh this more cautious view against the latest earnings surprise and consider how quickly project or policy risks could reshape both narratives.

Explore 4 other fair value estimates on Williams Companies - why the stock might be worth 13% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Williams Companies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Williams Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Williams Companies' overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.