Stronger-Than-Expected Operating Income Could Be A Game Changer For ArcBest (ARCB)

ArcBest Corporation ARCB | 0.00 |

- In the recent past, ArcBest reported first-quarter revenue roughly matching market expectations while adjusted operating income exceeded estimates, supported by healthy demand for its shipping services.

- This performance highlights how growing e-commerce and global trade can bolster ground transportation operators like ArcBest even as they contend with economic cycles and fuel cost volatility.

- Now, we’ll explore how ArcBest’s stronger-than-expected adjusted operating income shapes its broader investment narrative and future business outlook.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

ArcBest Investment Narrative Recap

To own ArcBest, you need to believe that its mix of asset based trucking and asset light logistics can convert e commerce and trade demand into resilient earnings, even when freight conditions are choppy. The Q1 adjusted operating income beat modestly supports the near term catalyst around technology driven efficiency improvements, but it does not remove the key risk that soft freight markets, industry overcapacity, and higher labor costs could continue to weigh on margins.

The recent update on ArcBest’s long running share repurchase program is most relevant here, as it sits alongside Q1 results that showed pressure on reported earnings despite stronger adjusted operating income. For investors focused on catalysts, continued buybacks and a steady US$0.12 quarterly dividend may help signal confidence and support per share metrics, even as the company works through weaker net income and a still challenging freight backdrop.

Yet behind the solid quarter, investors should not overlook the ongoing risk that higher labor costs and soft freight demand may continue to affect...

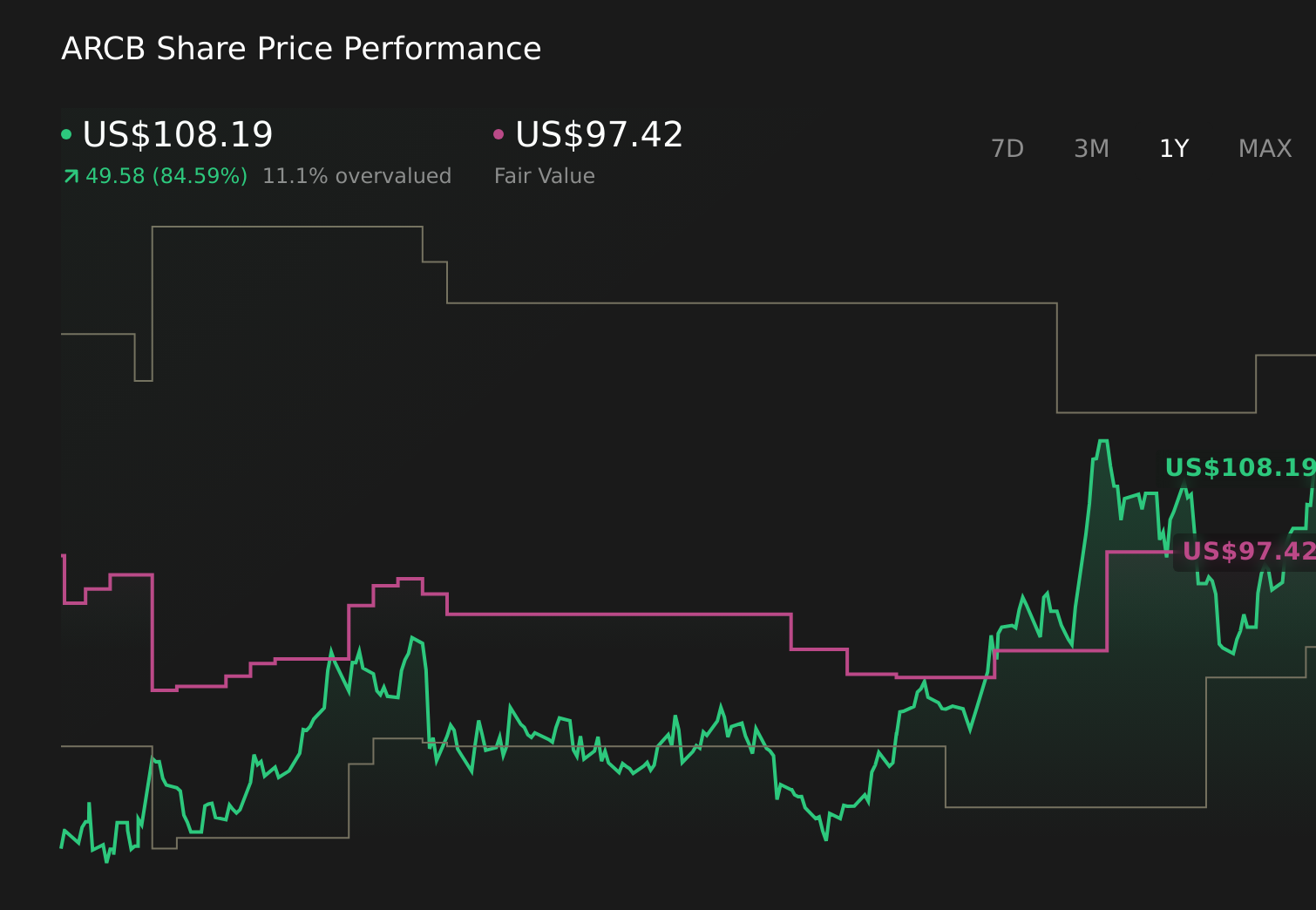

ArcBest’s narrative projects $4.5 billion revenue and $147.2 million earnings by 2028.

Uncover how ArcBest's forecasts yield a $97.42 fair value, a 22% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting ArcBest’s earnings to reach about US$213.7 million by 2029, and see AI driven automation as a step change, not just an efficiency tweak. In light of Q1’s adjusted operating income beat, and contrasting views on whether automation risks or opportunities dominate, this more upbeat narrative shows how far opinions can differ and why it is worth weighing several possible paths for ArcBest’s results.

Explore 3 other fair value estimates on ArcBest - why the stock might be worth as much as $97.42!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ArcBest research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ArcBest research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ArcBest's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.