Sysco Stock And Two Defensive Dividend Names For Rising Inflation

Sysco Corporation SYY | 0.00 |

With inflation pressures building after the Strait of Hormuz closure and interest rates pushing higher, many investors are taking a fresh look at dependable dividend stocks that may help keep portfolios grounded. The focus here is on companies with a history of paying and growing dividends, backed by solid balance sheets and measured payout ratios, rather than on speculative inflation trades. This article walks through three stocks from the Inflation-Resilient Dividend Stocks screener that appear positioned to respond in different ways to the current mix of higher prices, rising bond yields, and tighter financial conditions, and explains what that could mean for your long term allocation.

Metcash (ASX:MTS)

Overview: Metcash is a wholesale and distribution group that supplies food, liquor, and hardware products to independent supermarkets, convenience stores, hotels, and hardware retailers across Australia, operating well known retail brands such as IGA, Foodland, Mitre 10, Home Hardware, Total Tools, Cellarbrations, IGA Liquor, and the Bottle O.

Operations: Metcash generates about A$9.2b in Food revenue, A$5.4b in Liquor revenue, and A$2.8b in Hardware & Tools revenue, with all reported revenue of A$17.4b coming from Australia.

Market Cap: A$3.2b

Metcash provides exposure to essential groceries, liquor, and hardware at a time when inflation and higher rates are pressuring many other sectors. Its wholesale model can help pass through rising costs while keeping some independent retailers competitive. The shares currently screen as undervalued against cash flow estimates, have an established dividend, and are supported by a broad A$17.4b revenue base. However, earnings growth is modest, margins are thin at around 1.6%, and the dividend track record has not been perfectly consistent. With inflation reported as reaccelerating after the Strait of Hormuz closure, Metcash’s ability to handle price increases and funding risks is a key consideration for investors to examine more closely.

Metcash’s wholesale reach and broad A$17.4b revenue base hint at an underappreciated income engine, but the thin 1.6% margins and uneven dividend history matter, so unpack the 3 key rewards and 1 important warning sign

Otter Tail (OTTR)

Overview: Otter Tail Corporation is a diversified utility and manufacturing group that generates and sells electricity in the Upper Midwest while also producing metal components, thermoformed plastics, and PVC pipe for infrastructure, industrial, and consumer markets across the United States.

Operations: Otter Tail generates around US$582.9m of revenue from Electric, US$408.4m from Plastics, and US$322.4m from Manufacturing.

Market Cap: US$3.7b

Otter Tail stands out in a period of rising inflation and interest rates because its regulated electric utility and PVC pipe businesses can often adjust prices, while its manufacturing arm adds another source of cash flow and dividend support. At the same time, investors need to weigh regulatory and environmental pressures on coal and renewables, elevated debt and funding needs tied to a US$1.4b capital plan, and the cost of recent PVC litigation settlements. With earnings guidance reaffirmed, a dividend still on the table, and PVC resin pricing closely linked to the same energy shock that is lifting inflation, there is more to the Otter Tail story than a simple “defensive utility” label suggests.

Otter Tail’s income mix from regulated power, PVC and manufacturing is unusual, and the market may not be pricing that complexity. Read the 1 key reward and 3 important warning signs (1 is major!) for one insight that could change how you see the stock

Sysco (SYY)

Overview: Sysco is a global foodservice distributor that supplies restaurants, hospitals, schools, hotels, and other venues with everything from frozen and fresh food to kitchen equipment, paper goods, and cleaning supplies. It helps keep much of the food eaten away from home moving through the supply chain.

Operations: Sysco generates around US$58.2b from U.S. Foodservice Operations, US$15.8b from International Foodservice Operations, US$8.6b from SYGMA, and US$1.1b from Other activities.

Market Cap: US$39.9b

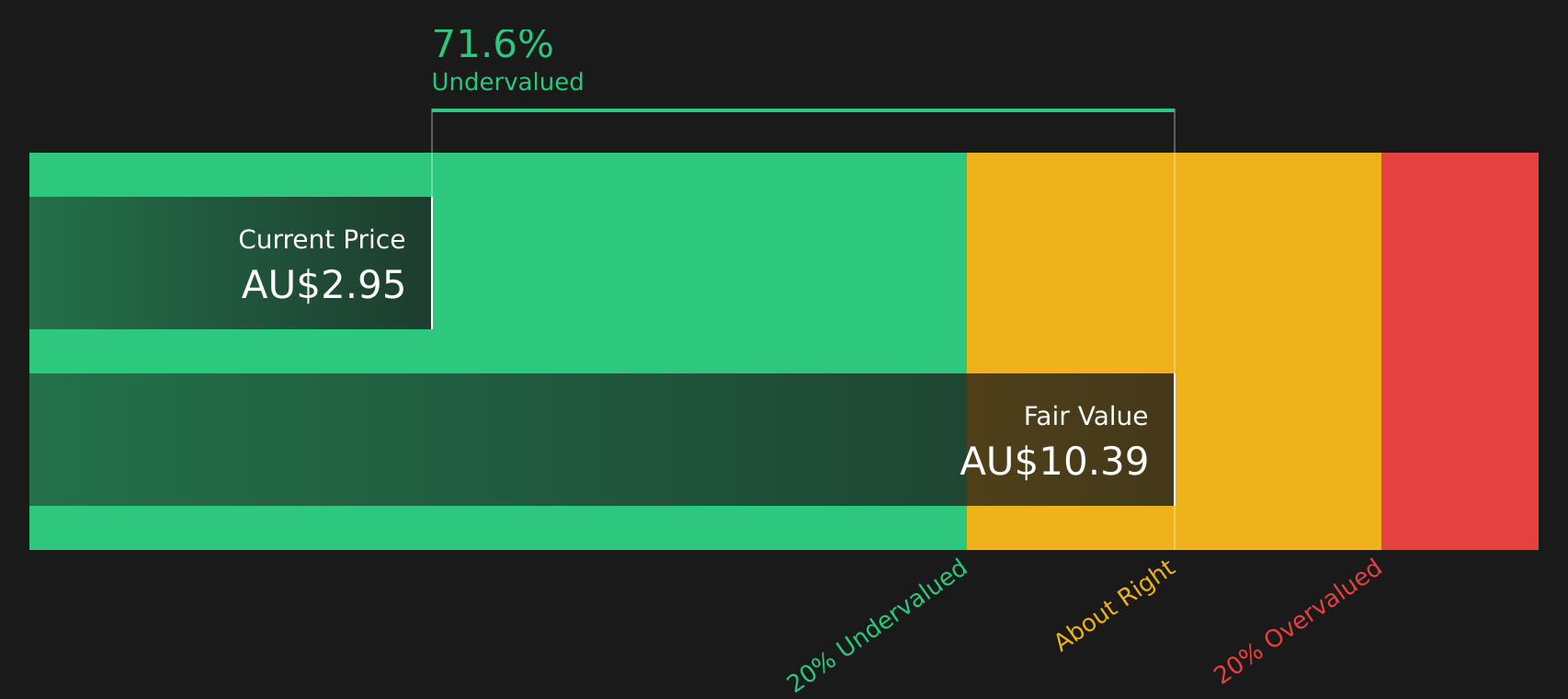

Sysco draws attention in an inflation spike because it sits between suppliers and thousands of foodservice customers, giving it pricing levers that can help keep a 2.63% dividend supported while costs for meat, poultry, and fuel are moving higher. The business has high reported ROE, a long record of dividend increases, and scale large enough to prepare for events like the 2026 World Cup. However, its recent net income and EPS have slipped, debt is heavy, and a larger credit facility and term loan increase funding exposure if rates stay high. With the stock trading well below some fair value estimates, the tension between Sysco’s income appeal and its leverage and margin pressures is exactly what investors will want to examine more closely.

Sysco’s scale, pricing power, and dividend history could be masking a very different story when compared with its leverage and funding needs, so review the 3 key rewards and 1 important major warning sign

The three dividend stocks covered so far are only a starting point, as the full Inflation-Resilient Dividend Stocks screener surfaces 21 more companies with equally compelling income stories that may fit different risk and sector preferences. Use Simply Wall St to identify, filter and analyze the specific catalysts and dividend narratives that matter to you so you can focus on the highest conviction opportunities for your portfolio.

Take Control of Your Investment Journey

If Metcash or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly

Fresh ideas move first, and by the time the crowd catches on the cleanest entry points can be gone. Scan curated stocks gaining quiet momentum under the radar for now and consider your options.

- Explore opportunities in resilient compounding by screening companies with reliable cash flows and sturdy finances using the 9 high quality undervalued stocks.

- Assess structural trends in power demand by reviewing infrastructure builders and grid specialists through the curated 35 power grid technology and infrastructure stocks.

- Review developments in robotics adoption by focusing on hand picked automation leaders via the 29 robotics and automation stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.