Tapestry (TPR) Stock May Be Fairly Priced Despite Pricey Earnings

Tapestry TPR | 0.00 |

Tapestry stock is coming off a striking run over the past five years, yet its valuation checks now point to a company that no longer looks obviously cheap, with the intrinsic value estimate from a Discounted Cash Flow (DCF) model sitting close to the current share price while traditional multiples lean expensive.

- Tapestry has delivered a 311.2% return over 5 years, which means anyone holding through that period has already seen a very large amount of value recognized by the market.

- Future cash flow expectations and the durability of the brand portfolio can support the current valuation, but any pressure on margins or slower cash generation may quickly weigh on what investors are willing to pay.

- The company passes only 1 of 6 valuation checks, which suggests Tapestry leans expensive rather than a clear bargain when looking at the broader assessment of value.

The key consideration for investors is whether Tapestry's recent gains leave enough potential upside relative to its intrinsic value estimate to justify the current price.

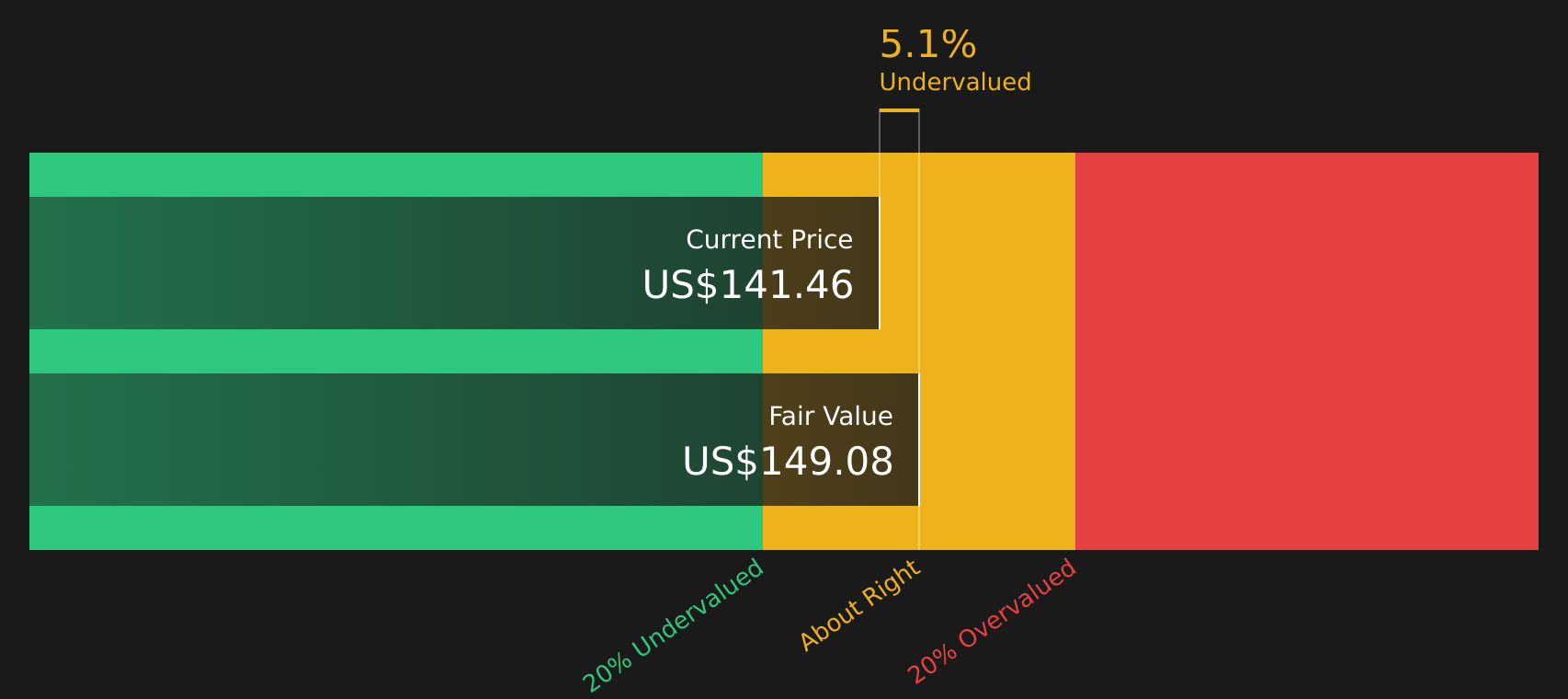

Is Tapestry Fairly Priced on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what Tapestry is worth based on the cash it is expected to generate for shareholders. For Tapestry, the model uses latest twelve month free cash flow of about $1.76b and assumes those cash flows continue growing rather than shrinking, then discounts them back to today using a 2 stage Free Cash Flow to Equity approach.

On this basis, the DCF points to an intrinsic value of about $149 per share. With the model indicating the stock is trading at roughly a 3.2% discount to that estimate, Tapestry appears only slightly cheap rather than a deep value situation. The small gap between the current share price and the DCF outcome suggests the market already prices in much of the projected cash generation, so any change in free cash flow expectations could quickly tilt this balance.

Overall, the Discounted Cash Flow view suggests Tapestry stock looks about fairly valued at current levels.

Tapestry is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Is Tapestry Getting Expensive on Earnings?

P/E is a useful lens for Tapestry because earnings power is central to how investors usually compare global luxury stocks. On this measure, Tapestry trades on a P/E of about 44.0x, which is well above the luxury industry average of around 21.7x and higher than the peer group average of roughly 24.2x.

The fair P/E ratio implied by its profile is about 27.6x. The current multiple therefore sits materially above what this framework suggests would be reasonable for Tapestry. That gap indicates investors are already paying a premium for the stock relative to both the sector and the modelled fair level, leaving limited room for disappointment if earnings do not support such a high valuation.

On the P/E measure, Tapestry stock currently screens as overvalued compared with both peers and its own fair multiple estimate.

The Tapestry Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Tapestry connect the valuation picture above with the specific expectations about Tapestry's future that would need to hold for the stock to be worth meaningfully more or less than it is today. These Narratives sit on the company’s Community page. Instead of stopping at a single ratio or model output, they unpack the path for growth, margins and earnings that number relies on so you can watch how reality lines up over time.

The community is split on Tapestry, with one side leaning into brand momentum and AI, and the other focused on tariffs, competition, and margin risk.

Bull case: 13% undervalued

"Ongoing investments in digital infrastructure, omnichannel capabilities, and data-driven customer engagement are expected to enable margin expansion and direct-to-consumer growth..."

Bear case: 29% overvalued

"Digital disruption is intensifying, with agile direct-to-consumer and social media-native competitors rapidly gaining market share, which could increasingly marginalize established brands like Coach and Kate Spade..."

Do you think there's more to the story for Tapestry? Head over to our Community to see what others are saying!

The Bottom Line

For Tapestry, the Discounted Cash Flow (DCF) view and the market multiples tell a different story. The intrinsic value estimate sits close to the current share price, while the elevated P/E suggests the stock is priced for strong earnings support and limited room for setbacks. The low broader value score highlights that, outside the DCF, most checks do not flag Tapestry as a clear bargain. What really decides it from here is whether the company can sustain the cash generation and margins implied in the DCF without investors reassessing the premium multiple they are currently paying.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.