Terex (TEX) Stock Could Be 13% Undervalued After Strong Growth And Buy Signals

Terex Corporation TEX | 0.00 |

Terex stock reacts to strong fundamentals and technical momentum

Terex (TEX) has attracted investor attention after reports of significant year-over-year growth in revenue and net profit, alongside high operating efficiency and supportive technical signals that point to strong price momentum.

At a share price of $66.82, Terex has seen strong short term momentum, with a 30 day share price return of 16.61% feeding into a 1 year total shareholder return of 48.69%. This reflects building interest in the stock as recent operational and technical signals filter through.

If Terex’s move has you thinking more broadly about industrial and infrastructure themes, this could be a moment to scan other power grid related opportunities through the 34 power grid technology and infrastructure stocks

With Terex posting double digit annual growth in revenue and net income and trading at a discount to both analyst targets and some intrinsic estimates, the key question is whether the stock is still undervalued or if the market is already pricing in future growth.

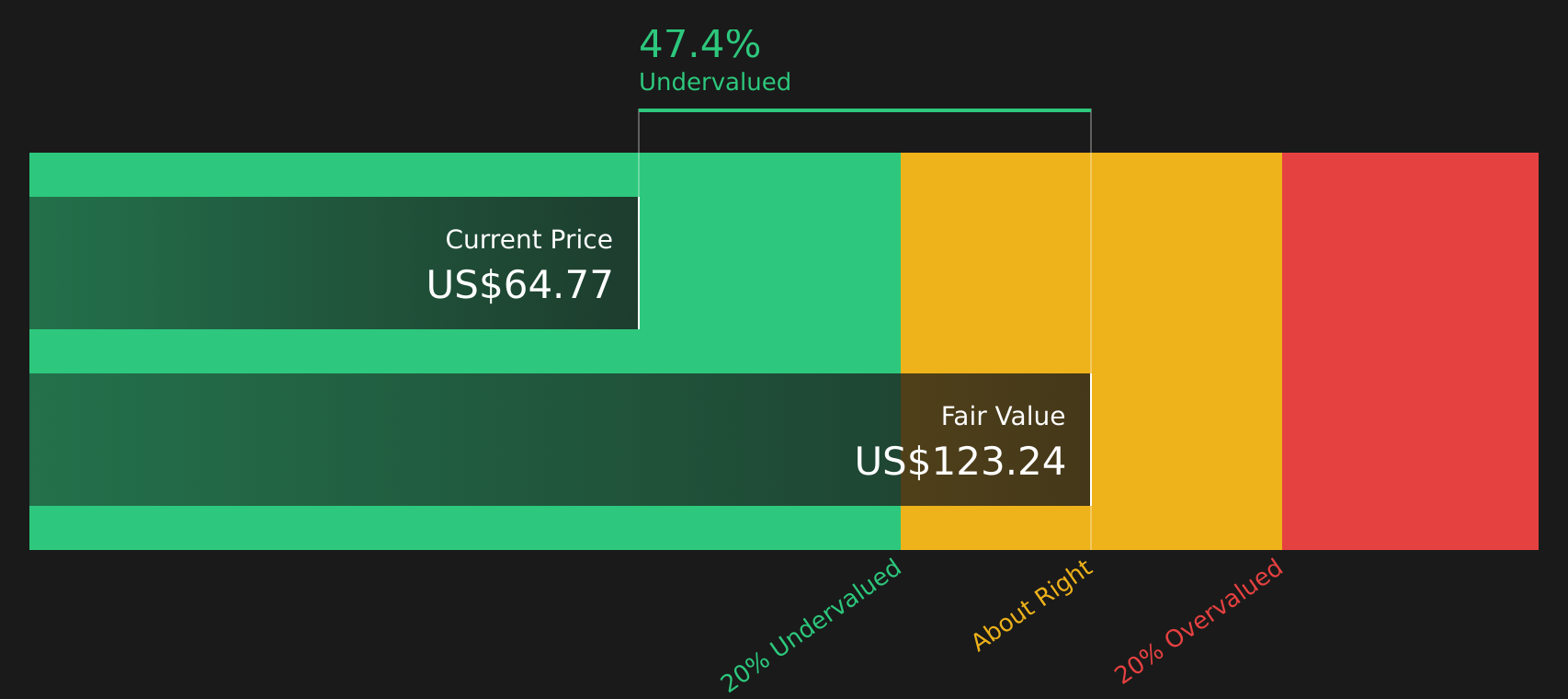

Most Popular Narrative: 13% Undervalued

On the most followed narrative, Terex’s fair value of $76.79 sits above the last close at $66.82. This frames the current move against a discounted cash flow and earnings outlook built on detailed analyst assumptions.

The company's acceleration of electrified and digital product offerings (Environmental Solutions growth, expansion of 3rd Eye telematics and SaaS subscriptions) is unlocking higher-margin, recurring revenues and enabling Terex to benefit from stricter sustainability and efficiency regulations, supporting margin expansion and differentiated pricing for next-generation equipment.

Curious what kind of revenue path, margin lift, and earnings profile would support that valuation gap for Terex, and how long that runway might last? The full narrative sets out a detailed financial roadmap built around those assumptions, including where analysts disagree most on the outcome.

Result: Fair Value of $76.79 (UNDERVALUED)

However, Terex’s story can change quickly if persistent high interest rates keep customers delaying equipment purchases, or if integration of the REV assets drags on margins.

Another view on Terex valuation

The DCF based fair value of $93.36 suggests Terex is about 28.4% below an estimate of its future cash flow value. This reinforces the idea that the stock screens as undervalued on this framework. With such a gap, the key question is which assumptions you trust most.

To see how that cash flow based view is built, and what would need to change for the valuation to move closer to the current price, Look into how the SWS DCF model arrives at its fair value.

Next Steps

With both appealing rewards and flagged risks in the Terex story, do you want to rely on others or test the numbers yourself, then weigh the balance and see how the 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Terex?

If Terex has sharpened your focus on where to put fresh capital, do not stop here. The right watchlist today can shape your next few years.

- Spot potential mispriced opportunities early by scanning the 45 high quality undervalued stocks that combine quality fundamentals with attractive valuations.

- Build a portfolio with staying power by reviewing the solid balance sheet and fundamentals stocks screener (48 results), focusing on companies with stronger financial footing.

- Get ahead of the crowd by hunting through the screener containing 19 high quality undiscovered gems that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.