Textron (TXT) Valuation Check As Aerospace Results And New Aircraft Programs Draw Fresh Attention

Textron Inc. TXT | 88.05 | -0.97% |

Textron (TXT) is back in focus after strong aerospace and defense results, active analyst commentary, and fresh institutional repositioning, with interest further supported by new aircraft products entering service featuring advanced Garmin Autothrottle technology.

The recent aerospace and defense contract wins, product milestones and mixed analyst commentary are landing against a constructive backdrop, with a 90-day share price return of 13.5% and a 1-year total shareholder return of 19.16% suggesting momentum has been building rather than fading.

If Textron’s latest moves have caught your attention, it could be a good moment to scan other aerospace and defense stocks that are also tied to defense spending and aircraft programs.

With Textron trading near US$94.23, an intrinsic discount of about 31% and only a small gap to the average analyst price target, the key question is whether there is still a genuine entry window here or if the market is already pricing in future growth.

Most Popular Narrative: 1% Overvalued

At a last close of US$94.23 against a narrative fair value of about US$93.34, Textron is framed as slightly expensive, with that view built on detailed earnings, margin and discount rate assumptions.

The analysts have a consensus price target of $92.571 for Textron based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $107.0, and the most bearish reporting a price target of just $82.0.

If you are curious about the revenue path, margin lift and future P/E this story is built on, and how buybacks factor into the equation, read the full narrative.

Result: Fair Value of $93.34 (OVERVALUED)

However, there is still the risk that a weaker product mix and cost pressures, especially in Aviation and Industrial, could keep margins below what this narrative assumes.

Another View: Market Ratios Paint A Different Picture

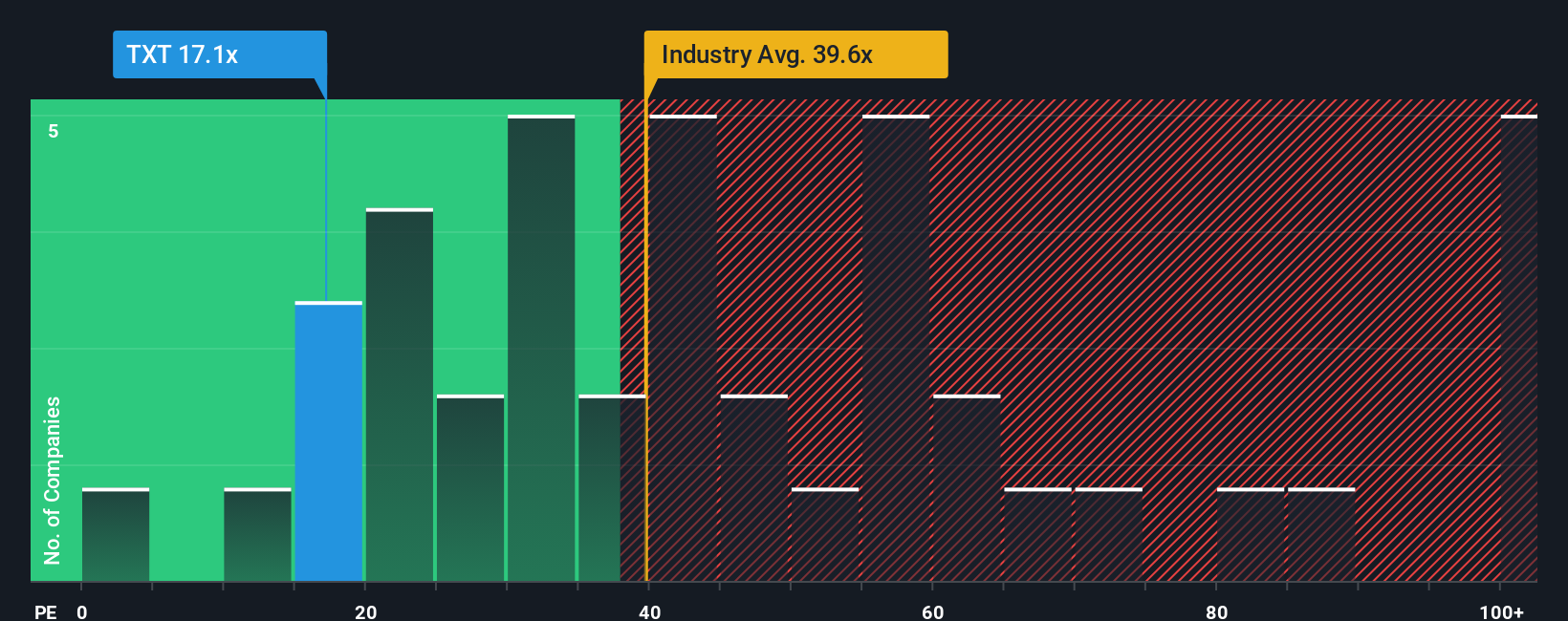

While the narrative model has Textron looking about 1% overvalued at a fair value near US$93.34, market ratios tell a softer story. The current P/E of 20.1x sits well below both the estimated fair ratio of 23.6x and the US Aerospace & Defense average of 42.6x. This points to a company priced more cautiously than many peers. That gap can cut both ways, raising the question of whether it reflects healthy skepticism or an opportunity if earnings hold up.

Build Your Own Textron Narrative

If you are not on board with this view or prefer to weigh the numbers yourself, you can shape a fresh Textron story in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Textron.

Looking for more investment ideas?

If Textron has sharpened your interest, do not stop here. Use the Simply Wall St Screener to spot other opportunities that could suit your style.

- Target income-focused opportunities by scanning these 12 dividend stocks with yields > 3% that may fit a yield focused approach without ignoring fundamentals.

- Catch potential growth stories early by checking out these 3526 penny stocks with strong financials that already show stronger financial underpinnings than many peers.

- Position yourself for long term themes by reviewing these 110 healthcare AI stocks that sit at the intersection of medicine and data driven decision making.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.