The Bull Case For Alnylam Pharmaceuticals (ALNY) Could Change Following AMVUTTRA Uptake And Canada Reimbursement News

Alnylam Pharmaceuticals, Inc ALNY | 318.85 | -3.01% |

- In late February 2026, Alnylam Pharmaceuticals highlighted strong momentum for its RNAi franchise, including positive Phase 3 data and a favorable Canadian reimbursement recommendation for AMVUTTRA in transthyretin-mediated amyloid cardiomyopathy, alongside an upcoming presentation at the TD Cowen Health Care Conference in Boston.

- Together with upbeat analyst commentary on AMVUTTRA’s rollout and Alnylam’s growth profile, these updates have sharpened investor focus on the company’s rare disease leadership and expanding RNA-based pipeline.

- We’ll now consider how AMVUTTRA’s better-than-expected uptake and new reimbursement support reshape Alnylam’s investment narrative and risk balance.

The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you need to believe RNA interference can support a durable, profitable rare disease franchise anchored by AMVUTTRA, while the company broadens beyond transthyretin (TTR) amyloidosis. Right now, the key near term catalyst is continued AMVUTTRA launch performance and reimbursement wins; the biggest risk is heavy dependence on this single TTR franchise. The latest Canadian reimbursement progress and positive data support the catalyst but do not remove the concentration and pricing risks.

The most relevant update here is Canada’s positive reimbursement recommendation for AMVUTTRA in ATTR cardiomyopathy, backed by HELIOS B Phase 3 outcomes on mortality and cardiovascular events. This strengthens the case for international expansion as a meaningful driver of product revenue, alongside AMVUTTRA’s better than expected rollout so far. It may also influence how investors weigh the upside from new markets against ongoing concerns about future net price reductions and payer pressure over time.

Yet behind AMVUTTRA’s success, investors should also be aware of the risk that growing pricing pressure and net price erosion could eventually...

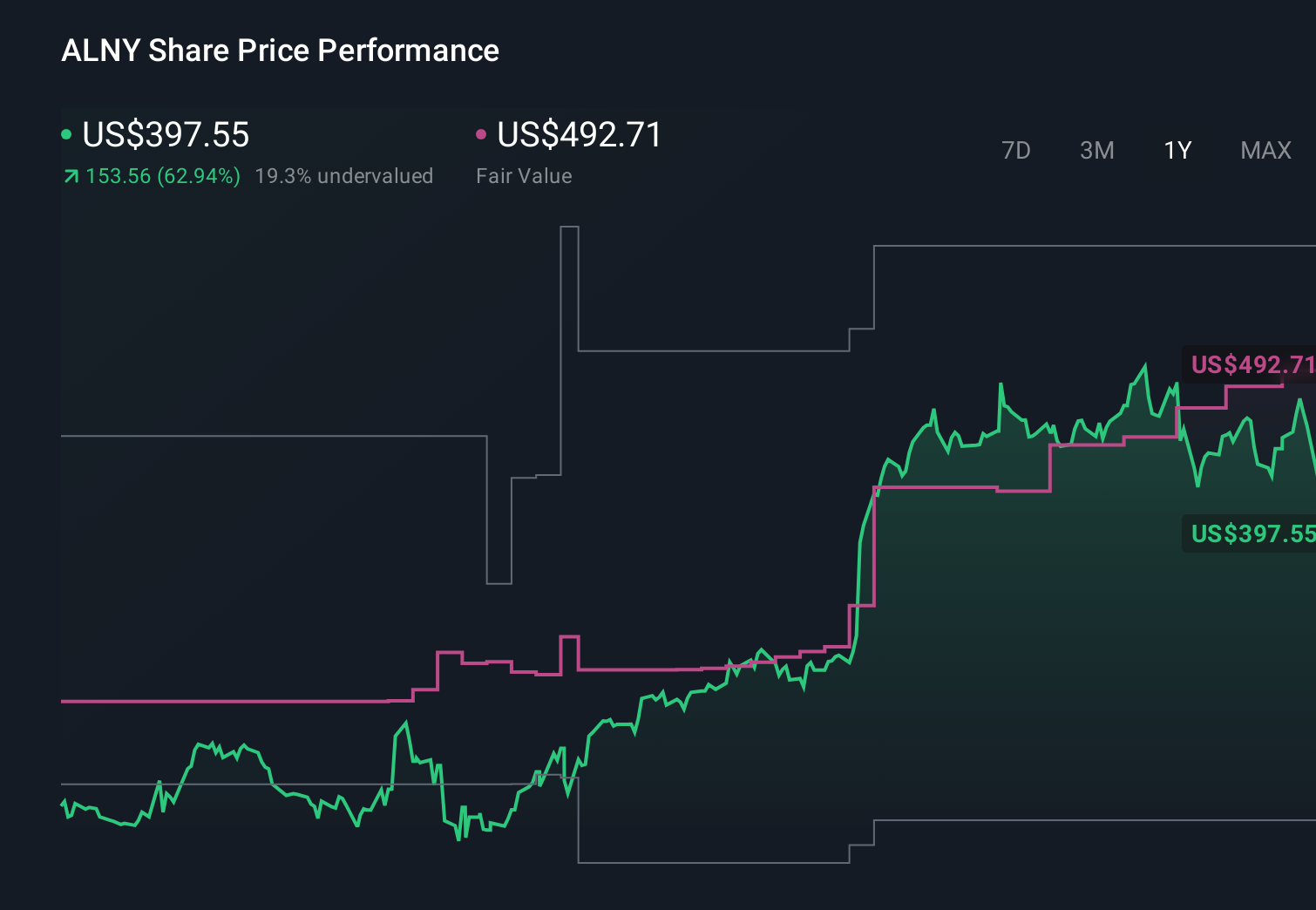

Alnylam Pharmaceuticals' narrative projects $7.0 billion revenue and $1.9 billion earnings by 2028.

Uncover how Alnylam Pharmaceuticals' forecasts yield a $491.92 fair value, a 51% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts took a far harsher view, assuming only about US$4.2 billion in 2028 revenue and roughly US$139 million in earnings, which sharply contrasts with the more upbeat story around AMVUTTRA’s rapid uptake and payer access; their caution highlights how differently you might weigh today’s launch wins against tomorrow’s pricing and TTR concentration risks, and it is a reminder to look at several competing narratives before deciding where you stand.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth as much as 92% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 84 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.