The Bull Case For CACI International (CACI) Could Change Following New VA Tech Deal And Army Contract Expansion

CACI International Inc Class A CACI | 0.00 |

- In early July 2026, CACI International Inc. reported a new six-year Department of Veterans Affairs technology contract worth up to US$308 million to modernize financial systems, alongside a more than US$140.5 million ceiling increase on a U.S. Army forensic exploitation contract and the return of Tom Kirkland as Executive Vice President of Electronic Warfare.

- Together, these contract wins and leadership changes highlight CACI’s role in modernizing critical federal technology infrastructure while deepening its capabilities in electronic warfare and mission-support services.

- With CACI securing a long-duration VA financial-systems modernization contract, we now assess how this development influences its existing investment narrative.

Find 45 companies with promising cash flow potential yet trading below their fair value.

CACI International Investment Narrative Recap

To own CACI, you need to believe that long term demand for complex, technology driven federal missions will keep supporting its backlog and earnings. The latest VA and Army awards modestly reinforce that backdrop, but they do not remove nearer term risks around federal budget timing, contract consolidation, and competition that could still make results lumpier than headline guidance suggests.

The six year, up to US$308 million VA iFAMS modernization contract looks most relevant, because it fits directly into CACI’s push toward higher value, software heavy modernization work. If this kind of ERP and systems transformation work scales across agencies, it could help offset pressure from pricing and talent costs, but it also increases CACI’s exposure to any slowdown or reprioritization in civilian IT modernization spending.

Yet despite these contract wins, investors should still be aware that...

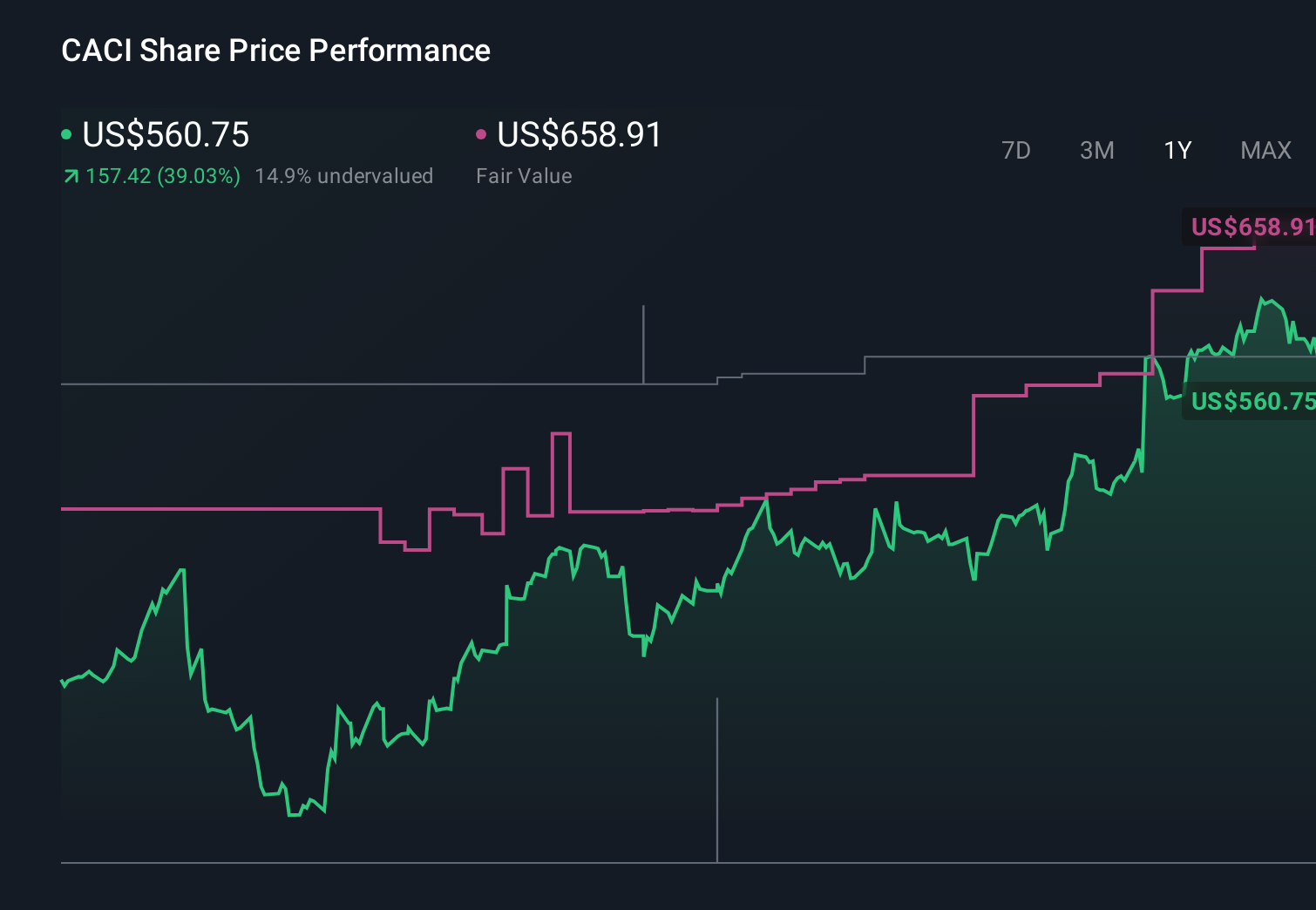

CACI International's narrative projects $12.0 billion revenue and $758.9 million earnings by 2029. This requires 9.3% yearly revenue growth and roughly a $222 million earnings increase from $536.9 million today.

Uncover how CACI International's forecasts yield a $676.71 fair value, a 39% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming only about 8.8% annual revenue growth to roughly US$11.8 billion and thinner margins, so if you worry that rising automation could undercut traditional service work, this more cautious view may resonate and the latest contract wins might or might not shift that picture.

Explore 3 other fair value estimates on CACI International - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.