The Bull Case For Frontline (FRO) Could Change Following Shifts In Ownership And Momentum Signals

Frontline Plc FRO | 0.00 |

- In recent weeks, Frontline Plc has seen a shift in its shareholder base, with institutional ownership easing to 29.60% while the stock’s technical indicators and moving averages shifted largely to buy signals within the Oil & Gas Related Equipment and Services industry.

- Despite this institutional pullback, Frontline now ranks first in its industry for price momentum and carries a moderate risk profile with very low beta, highlighting a mix of strong trading interest and relatively muted volatility.

- We will now examine how Frontline’s top-ranked price momentum and predominantly bullish technical signals interact with its existing investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Frontline Investment Narrative Recap

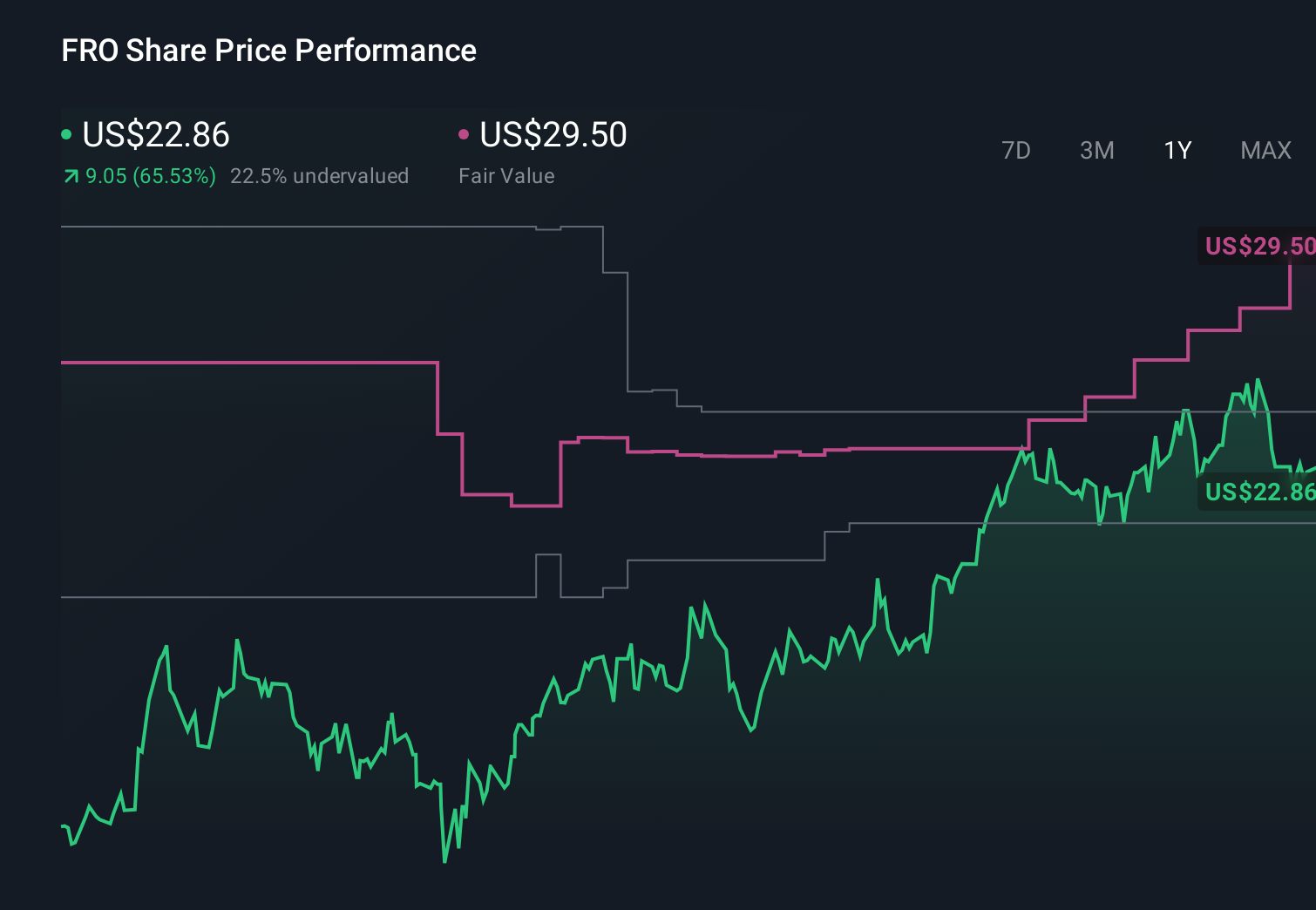

To own Frontline, you have to believe that tight tanker supply and active crude trade can keep supporting utilization and cash generation, even as the global energy transition and regulatory pressures loom in the background. The latest shift in institutional ownership and strong price momentum do not materially change the key near term swing factor, which is the strength and durability of tanker rates relative to Frontline’s spot exposure, nor the main risk of a downturn in seaborne oil volumes.

The most relevant recent development here is Frontline’s Q1 2026 results, with revenue of US$929.33 million and net income of US$559.12 million, followed by a higher US$1.55 per share dividend. This earnings step up and dividend move sit alongside the stock’s top ranked price momentum and bullish technical signals, reinforcing the idea that current trading strength is grounded in very recent cash generation, even as investors weigh how sustainable these conditions are against longer term demand and regulatory risks.

Yet behind the strong recent numbers, investors also need to consider how future regulatory costs and fleet renewal needs could affect Frontline’s ability to sustain...

Frontline’s narrative projects $1.6 billion revenue and $697.7 million earnings by 2029. This assumes revenues decline by 7.1% per year and earnings rise by about $318.6 million from $379.1 million today.

Uncover how Frontline's forecasts yield a $41.25 fair value, in line with its current price.

Exploring Other Perspectives

Compared with the baseline view, the most optimistic analysts were already assuming earnings of about US$792.1 million by 2029 and higher margins, so this recent price momentum and strong quarter could either reinforce their case or prompt revisions, underscoring how much your own view on tanker demand and regulatory risk can differ from theirs.

Explore 6 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Frontline research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Explore 31 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.