The Bull Case For General Dynamics (GD) Could Change Following New Abrams Tank Upgrade Contract Extension - Learn Why

General Dynamics Corporation GD | 0.00 |

- General Dynamics recently received a US$43.50 million contract modification to enhance production of Abrams M1A2 System Enhancement Package Version Three tanks, with work expected to run through January 31, 2028.

- This extension reinforces the company’s role in U.S. armored vehicle modernization, supporting its defense manufacturing pipeline and long-term program visibility.

- We’ll now examine how this Abrams production boost fits into General Dynamics’ broader investment narrative built around record backlog and long-term defense programs.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

General Dynamics Investment Narrative Recap

To own General Dynamics, you typically need to believe in durable defense demand, the value of its record backlog, and disciplined execution across long cycle programs. The US$43.50 million Abrams contract modification modestly supports that backlog and near term visibility, but does not materially change the key short term catalyst, which remains consistent submarine and shipbuilding progress at Electric Boat and NASSCO. The largest current risk is still program or supply chain disruption in Marine Systems rather than incremental tank work.

The Abrams production boost sits alongside General Dynamics’ recent Q1 2026 results, where revenue and earnings both increased year over year, reinforcing the role of long term defense programs in driving the business. Together, the earnings trajectory and continued awards like Abrams help illustrate how backlog conversion and disciplined capital allocation, including dividends and selective buybacks, are central to the investment case while investors monitor execution risks in complex Marine and defense platforms.

However, investors should also be aware that growing commitments to legacy platforms could expose General Dynamics to technology and customer preference risk if...

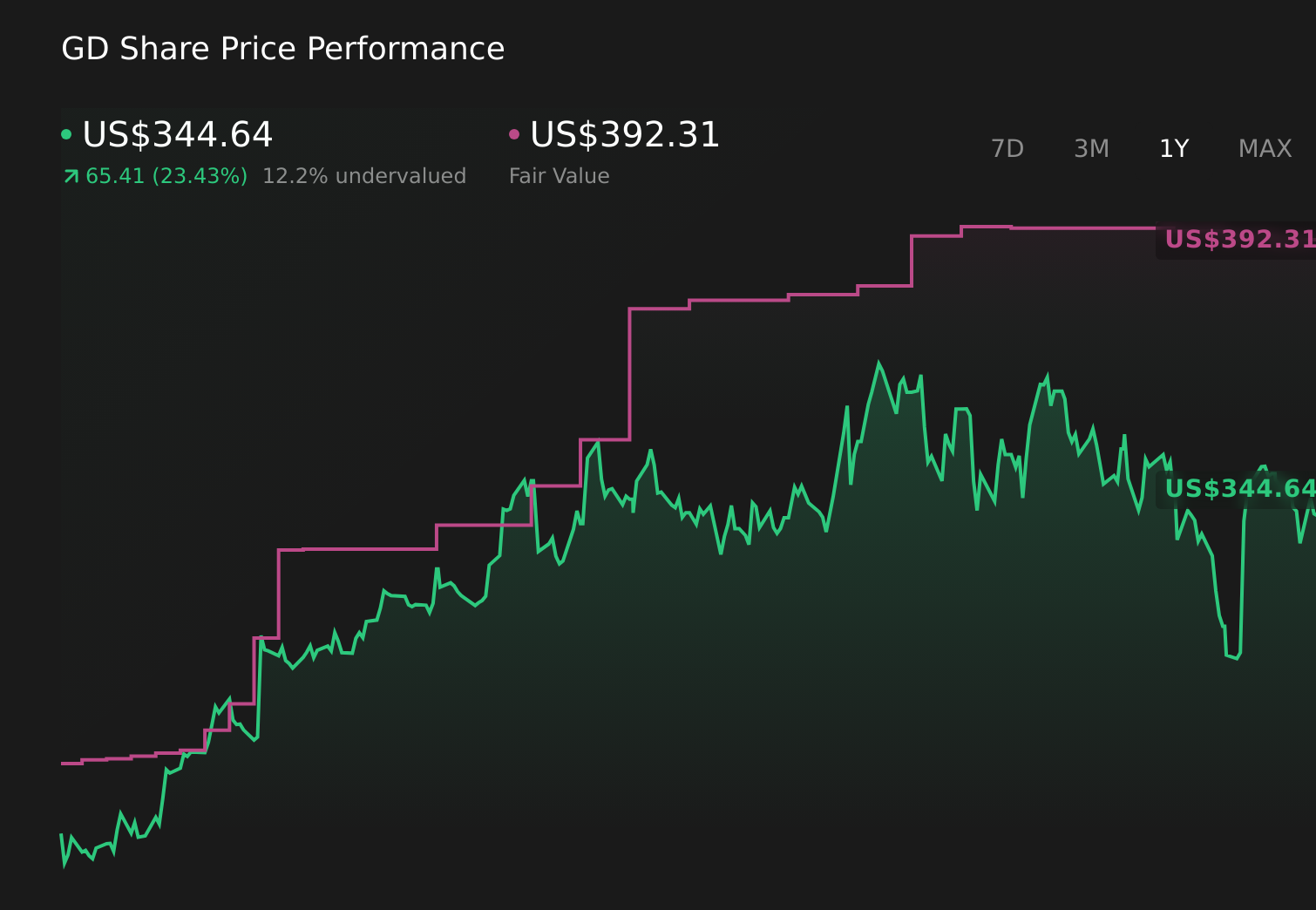

General Dynamics' narrative projects $60.7 billion revenue and $5.4 billion earnings by 2029. This requires 4.1% yearly revenue growth and a $1.1 billion earnings increase from $4.3 billion today.

Uncover how General Dynamics' forecasts yield a $392.22 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for General Dynamics cluster between US$392.22 and US$405.18, highlighting how differently individual investors can value the same cash flow outlook. Set against this, the reliance on multi year defense backlog as a core catalyst underscores why you may want to weigh several views on how resilient those programs really are before forming your own stance.

Explore 3 other fair value estimates on General Dynamics - why the stock might be worth as much as 16% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Dynamics research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free General Dynamics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Dynamics' overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.